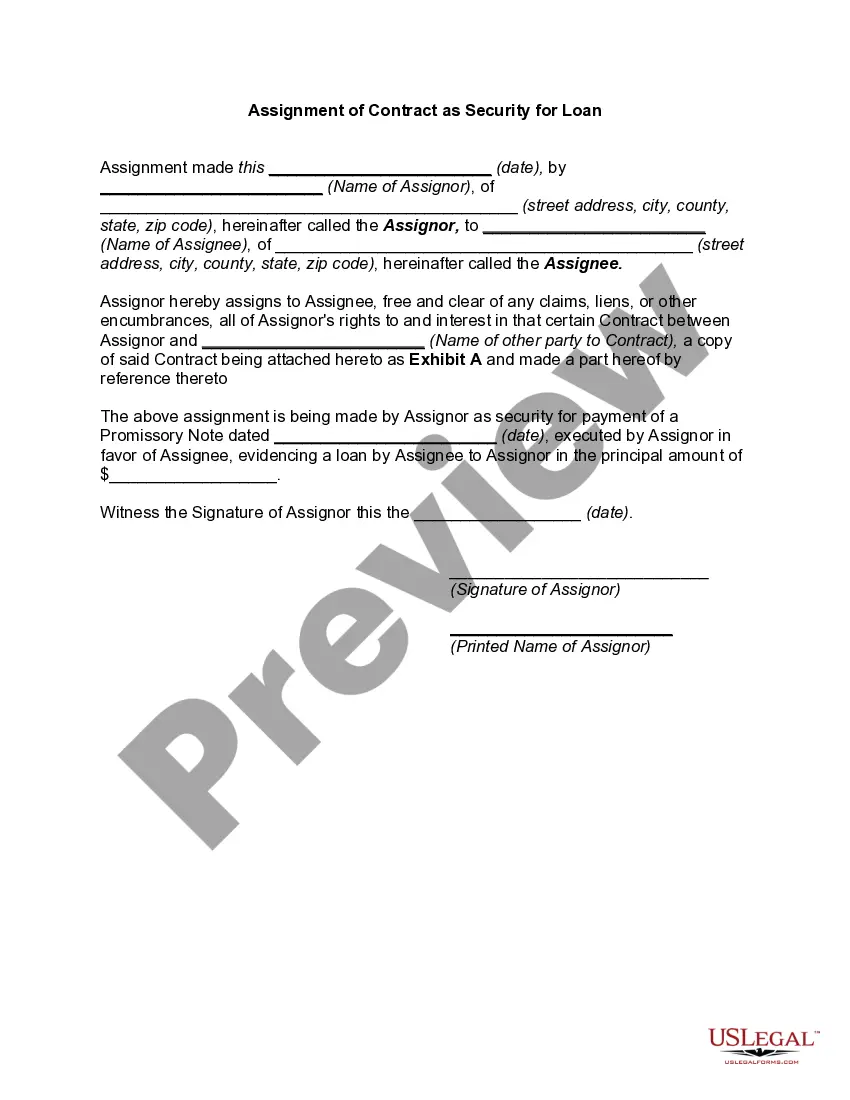

Delaware Assignment of Contract as Security for Loan: A Comprehensive Overview In Delaware, an Assignment of Contract as Security for Loan is a legal agreement entered into by a borrower (assignor) and a lender (assignee). This contractual arrangement allows the borrower to utilize an existing contract as collateral to secure a loan. By pledging their rights, interests, and benefits arising from the contract, the assignor provides an additional layer of security to the lender. Key Features: 1. Parties Involved: The agreement involves two primary parties. The assignor, often the original party to the contract, assigns their rights and obligations under the contract to the assignee (lender). 2. Purpose: The principal purpose of the Delaware Assignment of Contract as Security for Loan is to offer lenders additional assurance in case of default by the borrower. In the event of non-payment or breach of the loan agreement, the assignee can step in and enforce their rights as the assignor's legal successor. 3. Collateral: The assigned contract functions as collateral. This contract can encompass various agreements, such as lease contracts, purchase agreements, service contracts, or employment contracts. It could even include intellectual property licenses or royalty agreements. Collateralizing a contract allows the lender to possess a tangible asset, albeit in the form of legal rights and obligations. 4. Legal Documentation: To execute a Delaware Assignment of Contract as Security for Loan, a written agreement is essential. It outlines the assignment terms, including the rights transferred, representations, warranties, and the assignee's remedies in the case of default. Both parties must sign and notarize the agreement for legal validity. Types of Delaware Assignment of Contract as Security for Loan: 1. Absolute Assignment: The assignor transfers all rights, obligations, and benefits associated with the contract to the assignee. The lender gains complete control over the assigned contract, assuming all risks and rewards. 2. Conditional Assignment: In this type, the assignment is conditional upon the borrower's default or any other predetermined circumstances mentioned in the agreement. Until the condition is triggered, the assignor retains their rights under the contract. 3. Specific Assignment: This type involves assigning specific rights or a part of the original contract, rather than the entirety. The lender receives only certain aspects of the assigned contract, limiting their control and potential remedies in case of non-payment. 4. Floating Assignment: The assignment encompasses a pool of contracts, usually revolving around a particular business activity. Rather than assigning individual contracts, the assignor pledges a group of agreements as security for the loan. In Delaware, the Assignment of Contract as Security for Loan provides an effective mechanism for lenders to mitigate risk and secure repayment. It offers flexibility to assignors and lenders by allowing various types of assignments based on specific requirements.

Delaware Assignment of Contract as Security for Loan

Description

How to fill out Delaware Assignment Of Contract As Security For Loan?

You are able to invest time on-line attempting to find the lawful document format that suits the federal and state needs you will need. US Legal Forms gives thousands of lawful kinds which can be evaluated by specialists. It is simple to down load or print out the Delaware Assignment of Contract as Security for Loan from the assistance.

If you currently have a US Legal Forms accounts, you may log in and click the Obtain key. Next, you may comprehensive, modify, print out, or indicator the Delaware Assignment of Contract as Security for Loan. Each and every lawful document format you get is the one you have eternally. To get an additional version associated with a purchased form, go to the My Forms tab and click the corresponding key.

Should you use the US Legal Forms internet site the very first time, stick to the easy instructions under:

- First, ensure that you have chosen the proper document format for your region/city that you pick. See the form information to ensure you have picked the right form. If offered, take advantage of the Review key to appear with the document format also.

- If you wish to find an additional edition from the form, take advantage of the Search field to get the format that fits your needs and needs.

- Upon having discovered the format you want, just click Buy now to continue.

- Pick the costs program you want, type in your qualifications, and register for your account on US Legal Forms.

- Full the financial transaction. You can use your charge card or PayPal accounts to pay for the lawful form.

- Pick the format from the document and down load it for your device.

- Make modifications for your document if necessary. You are able to comprehensive, modify and indicator and print out Delaware Assignment of Contract as Security for Loan.

Obtain and print out thousands of document themes utilizing the US Legal Forms Internet site, that provides the biggest variety of lawful kinds. Use specialist and status-distinct themes to tackle your company or personal requires.