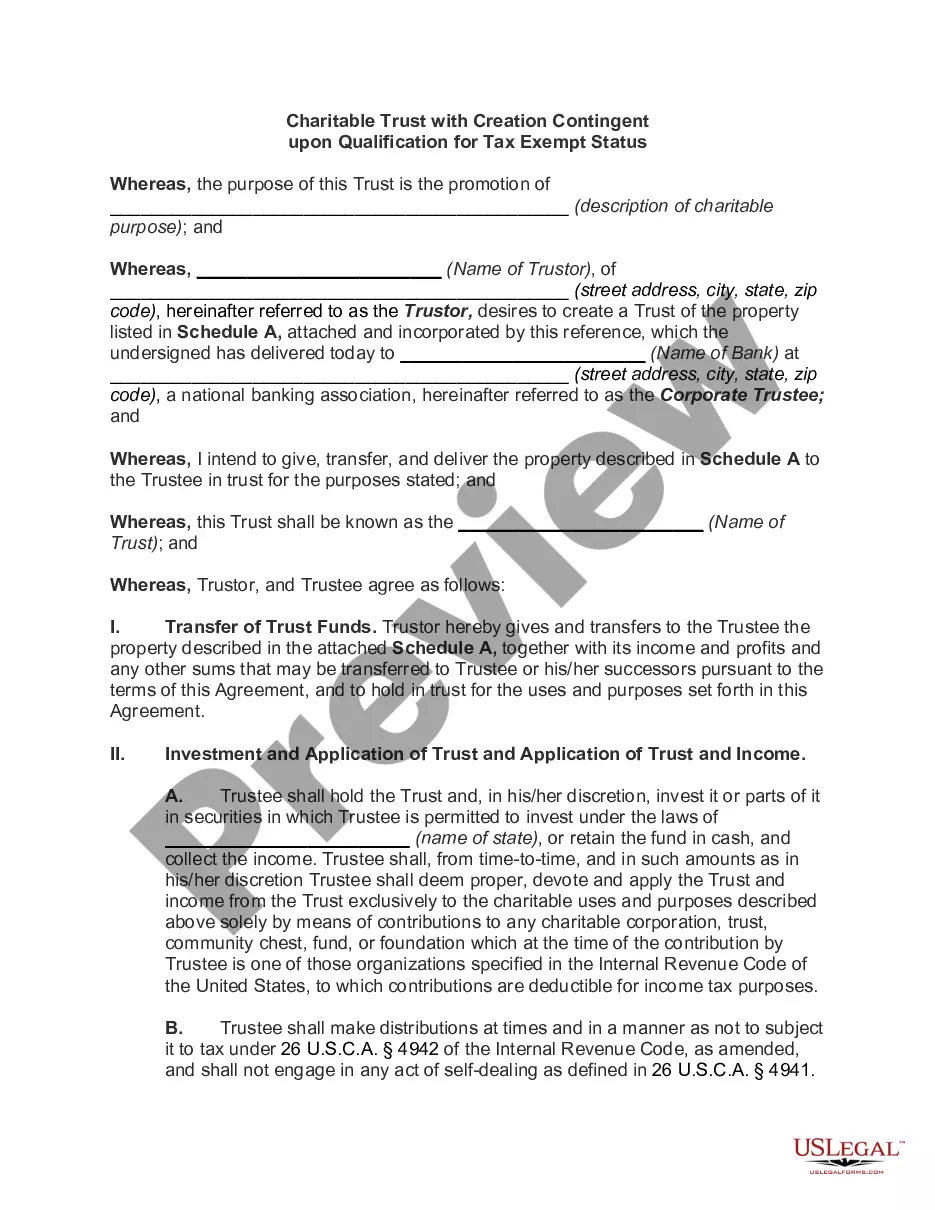

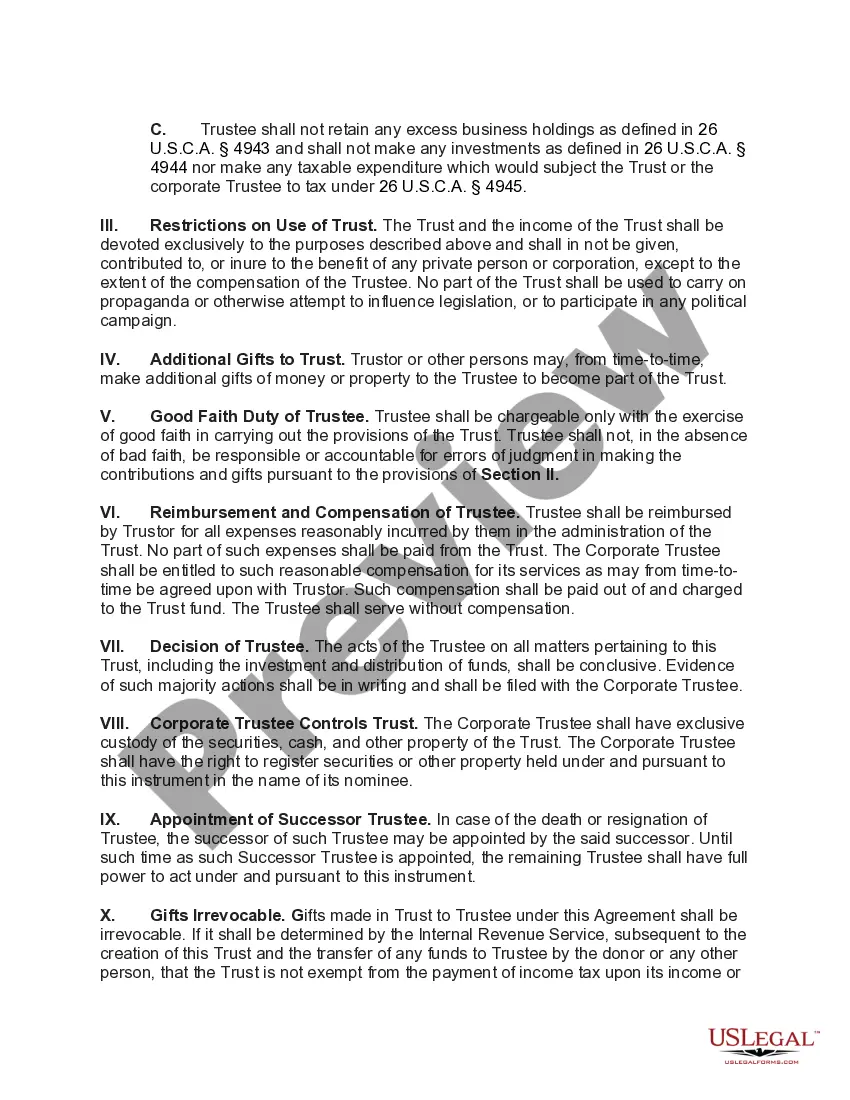

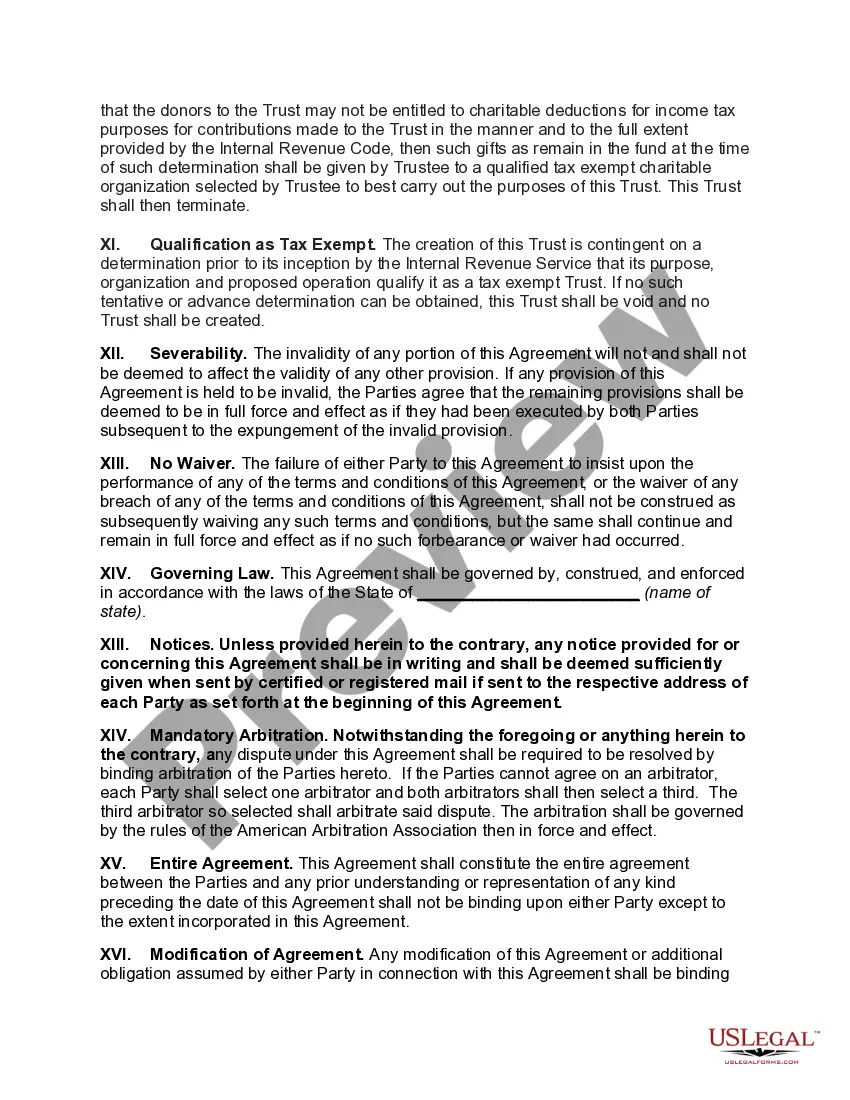

Delaware Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status is a legal entity established under the laws of Delaware that aims to support charitable causes while also seeking tax-exempt status from the Internal Revenue Service (IRS). This type of trust structure allows individuals or organizations to create a charitable trust, while ensuring that it qualifies for tax benefits and exemptions provided to recognized charitable entities. In order to establish a Delaware Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status, the trust's creator must comply with the requirements set forth by both the Delaware Statutory Trust Act and the IRS regulations for tax-exempt organizations. This includes filing the necessary paperwork to register the trust in Delaware and applying to the IRS for tax-exempt recognition. The primary goal of a Delaware Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status is to further philanthropic objectives by providing financial support to charitable causes, such as educational institutions, healthcare organizations, or social welfare programs. By qualifying for tax-exempt status, the trust can benefit from various tax advantages, including exemption from income taxes on its assets and the ability for donors to claim tax deductions for their contributions. There are different types of Delaware Charitable Trusts with Creation Contingent upon Qualification for Tax Exempt Status, each tailored to the specific charitable goals and purposes of the trust's creator. Some common types include: 1. Public Charitable Trusts: These trusts are established to benefit the public and have a broader charitable purpose. They typically support organizations that provide public benefit, such as education, healthcare, poverty alleviation, or environmental conservation. 2. Private Charitable Trusts: Private charitable trusts are established to benefit specific individuals, families, or groups. They focus on personal or family charitable objectives and may support causes that are important to the trust's creator. 3. Charitable Remainder Trusts: These trusts allow the donor to receive income during their lifetime while ensuring that the remaining assets are distributed to charitable organizations upon their death. Charitable remainder trusts provide flexibility and tax advantages for donors while supporting charitable causes in the long term. 4. Charitable Lead Trusts: Charitable lead trusts work in the opposite manner of charitable remainder trusts. In this case, the income from the trust is directed to charitable organizations for a defined period, after which the remaining assets are passed on to non-charitable beneficiaries, such as family members or other individuals. It's important for individuals or organizations interested in establishing a Delaware Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status to consult with legal and tax professionals who are knowledgeable in trusts, Delaware law, and IRS regulations. This ensures compliance with all applicable rules and maximizes the benefits of incorporating charitable giving with tax exemptions under Delaware's trust laws.

Delaware Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status

Description

How to fill out Delaware Charitable Trust With Creation Contingent Upon Qualification For Tax Exempt Status?

Discovering the right legitimate file design might be a have a problem. Needless to say, there are a lot of web templates available on the net, but how do you obtain the legitimate type you need? Use the US Legal Forms internet site. The assistance gives a huge number of web templates, like the Delaware Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status, which you can use for enterprise and personal requires. All of the kinds are inspected by specialists and satisfy state and federal demands.

In case you are previously authorized, log in to your bank account and then click the Down load key to find the Delaware Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status. Make use of bank account to appear with the legitimate kinds you have acquired earlier. Go to the My Forms tab of the bank account and have an additional copy from the file you need.

In case you are a whole new user of US Legal Forms, here are easy guidelines for you to comply with:

- First, make sure you have selected the appropriate type for the town/area. You are able to check out the shape while using Preview key and study the shape information to ensure this is basically the right one for you.

- If the type is not going to satisfy your requirements, take advantage of the Seach area to discover the appropriate type.

- When you are certain the shape is acceptable, go through the Get now key to find the type.

- Select the pricing prepare you want and type in the needed details. Create your bank account and pay for the order making use of your PayPal bank account or Visa or Mastercard.

- Select the submit formatting and down load the legitimate file design to your product.

- Full, modify and produce and sign the received Delaware Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status.

US Legal Forms may be the most significant collection of legitimate kinds for which you will find numerous file web templates. Use the service to down load appropriately-created documents that comply with condition demands.