Delaware Uniform Residential Loan Application

Description

How to fill out Uniform Residential Loan Application?

You can spend hrs on the Internet trying to find the legitimate papers web template that meets the state and federal requirements you require. US Legal Forms provides a large number of legitimate varieties that are reviewed by pros. It is simple to obtain or printing the Delaware Uniform Residential Loan Application from my assistance.

If you already possess a US Legal Forms bank account, you may log in and click on the Download option. After that, you may comprehensive, edit, printing, or indicator the Delaware Uniform Residential Loan Application. Every legitimate papers web template you buy is yours for a long time. To have one more version associated with a bought type, visit the My Forms tab and click on the corresponding option.

If you are using the US Legal Forms site initially, keep to the basic guidelines under:

- First, be sure that you have chosen the correct papers web template for your region/town of your liking. Browse the type outline to make sure you have chosen the proper type. If readily available, use the Review option to search with the papers web template too.

- In order to get one more edition of your type, use the Search field to find the web template that suits you and requirements.

- When you have identified the web template you want, click on Buy now to carry on.

- Choose the costs plan you want, enter your credentials, and register for a free account on US Legal Forms.

- Total the purchase. You may use your charge card or PayPal bank account to purchase the legitimate type.

- Choose the formatting of your papers and obtain it to the system.

- Make modifications to the papers if required. You can comprehensive, edit and indicator and printing Delaware Uniform Residential Loan Application.

Download and printing a large number of papers layouts making use of the US Legal Forms web site, that offers the largest collection of legitimate varieties. Use professional and state-certain layouts to handle your business or person requirements.

Form popularity

FAQ

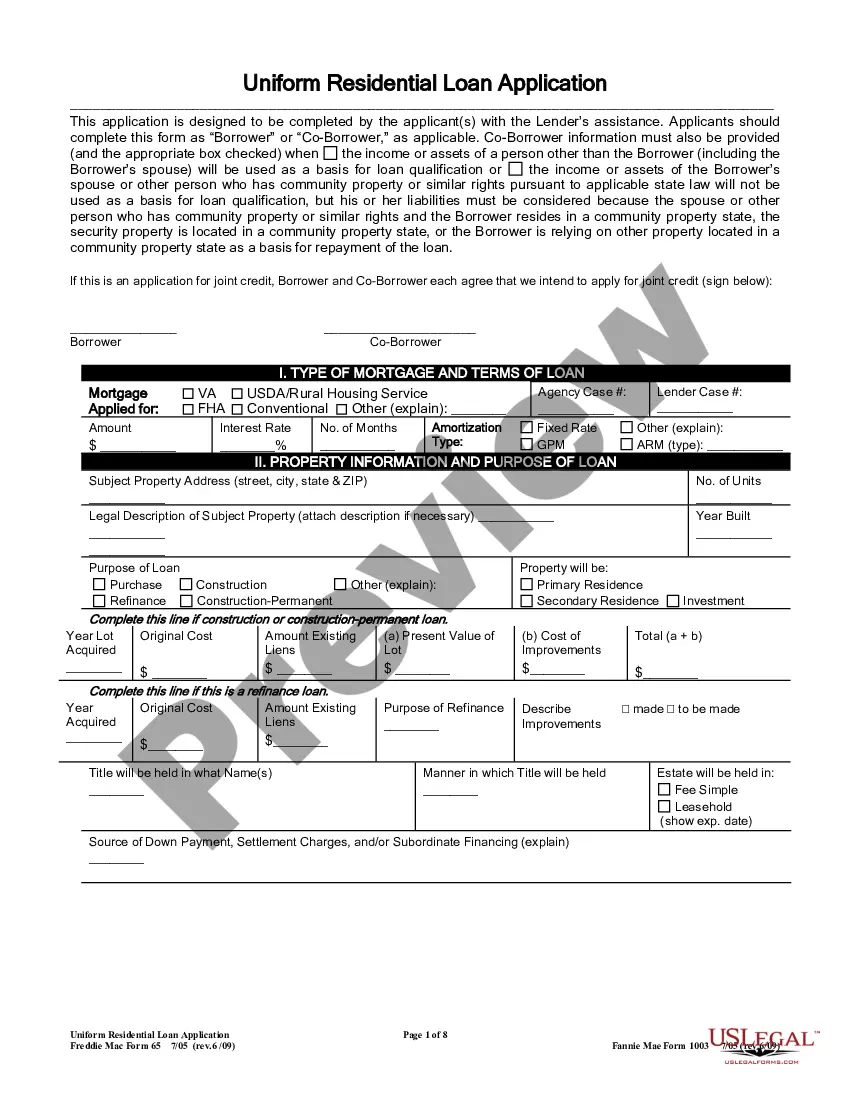

The uniform residential loan application is a form designed by Fannie Mae and Freddie Mac, government-sponsored enterprises (GSE) that support the mortgage market. The form was created to collect the information lenders need to assess your creditworthiness for a mortgage loan.

The iLAD is a ?superset? of loan application data based on MISMO v3. 4 that includes all the data in the ULAD Mapping Document and the GSE AUS Specifications. iLAD also includes additional origination data points requested by the industry that may be needed for exchange of loan information.

The URLA consists of two main forms, the Borrower Information Form and the Lender Information Form, which together make up the complete loan application. However, depending on certain situations, additional forms may be required. These are the Additional Borrower form, Unmarried Addendum, and Continuation Sheet.

The uniform residential loan application is a form designed by Fannie Mae and Freddie Mac, government-sponsored enterprises (GSE) that support the mortgage market. The form was created to collect the information lenders need to assess your creditworthiness for a mortgage loan.

Effective May 1, Desktop Underwriter® (DU®) and Desktop Originator® (DO®) will only accept new loans submitted using the redesigned Uniform Residential Loan Application (URLA)/Form 1003 and the updated DU MISMO 3.4 file format.

A loan application must be documented on the Uniform Residential Loan Application (Form 1003). A complete, signed, and dated version of the final Form 1003 must always be included in the loan file. The final Form 1003 must reflect the income, assets, debts, and final loan terms used in the underwriting process.

ULAD Map. Provides the association between the form fields on the URLA and the MISMO v3.4 data points. Every field in the URLA is included in the ULAD Mapping Document. Some URLA fields may require more than one MISMO data point.

The Uniform Loan Delivery Dataset (ULDD), part of the Uniform Mortgage Data Program (UMDP), is the common set of data elements required by Fannie Mae and Freddie Mac for single-family loan deliveries.