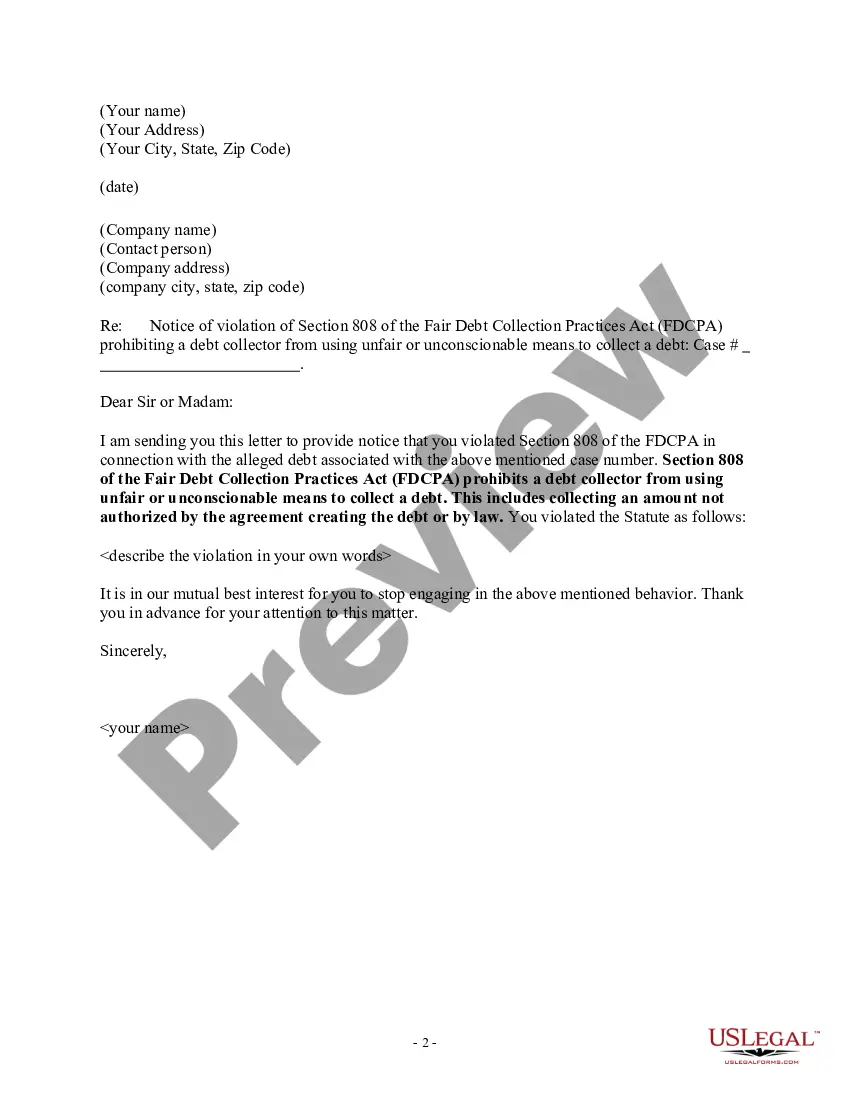

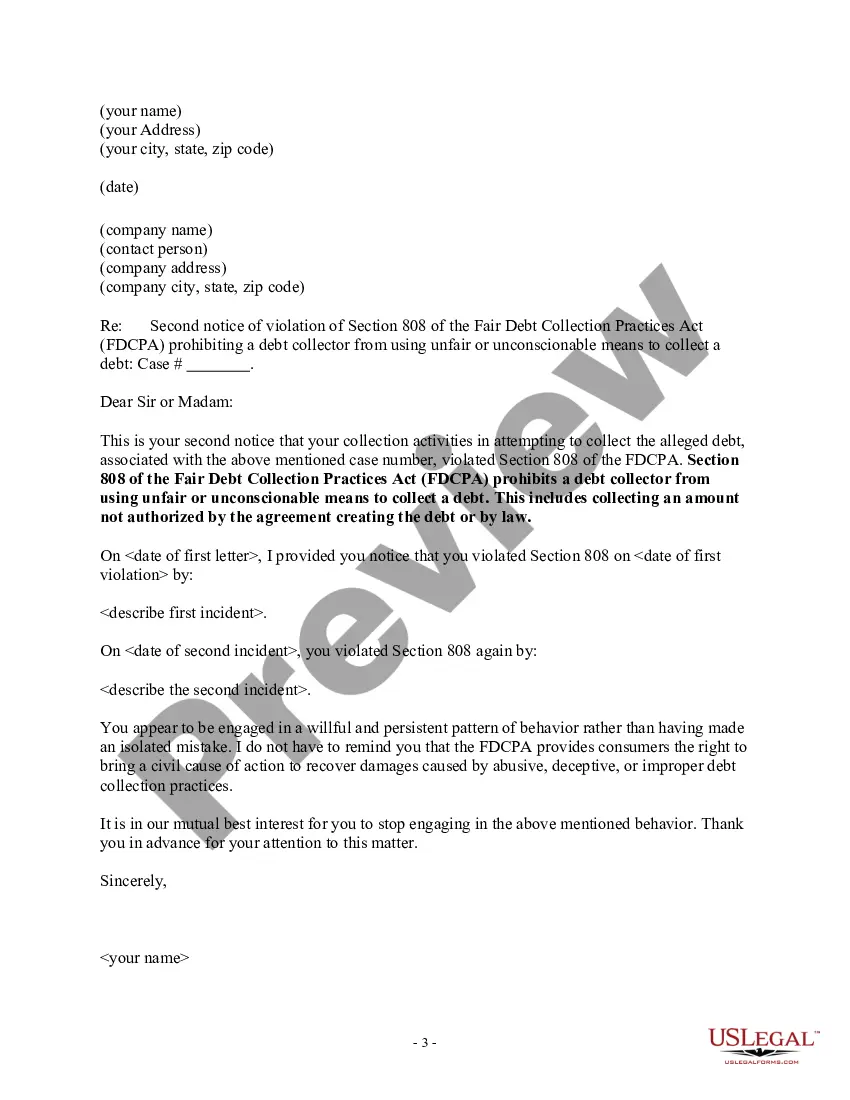

A debt collector may not use unfair or unconscionable means to collect a debt. This includes collecting an amount not authorized by the agreement creating the debt or by law.

Delaware Notice to Debt Collector - Collecting an Amount Not Authorized by Agreement or by Law

Category:

State:

Multi-State

Control #:

US-DCPA-42

Format:

Word;

Rich Text

Instant download

Description

Use this form to notify a debt collector they violated the Fair Debt Collection Practices Act (FDCPA). Receiving notice from a consumer makes it more likely a debt collector will comply with the FDCPA. If they don't comply after receiving notice, your notice letter may help prove that their actions were intentional.

Free preview

How to fill out Delaware Notice To Debt Collector - Collecting An Amount Not Authorized By Agreement Or By Law?

Are you presently within a situation in which you require papers for both company or person uses just about every day? There are tons of legal document web templates accessible on the Internet, but finding ones you can trust is not simple. US Legal Forms gives thousands of develop web templates, just like the Delaware Notice to Debt Collector - Collecting an Amount Not Authorized by Agreement or by Law, which can be composed to meet state and federal demands.

In case you are already familiar with US Legal Forms internet site and get your account, just log in. Next, you may acquire the Delaware Notice to Debt Collector - Collecting an Amount Not Authorized by Agreement or by Law web template.

Unless you provide an bank account and wish to begin using US Legal Forms, follow these steps:

- Obtain the develop you want and ensure it is to the proper metropolis/area.

- Use the Review option to check the form.

- Read the outline to ensure that you have chosen the correct develop.

- In case the develop is not what you are seeking, use the Look for area to get the develop that suits you and demands.

- Whenever you get the proper develop, just click Purchase now.

- Opt for the pricing plan you would like, complete the desired details to make your account, and buy your order utilizing your PayPal or charge card.

- Decide on a convenient file format and acquire your duplicate.

Discover every one of the document web templates you have purchased in the My Forms food selection. You may get a extra duplicate of Delaware Notice to Debt Collector - Collecting an Amount Not Authorized by Agreement or by Law whenever, if required. Just select the needed develop to acquire or printing the document web template.

Use US Legal Forms, one of the most comprehensive variety of legal kinds, to conserve time and steer clear of errors. The assistance gives professionally manufactured legal document web templates that can be used for a selection of uses. Make your account on US Legal Forms and begin producing your daily life easier.

Form popularity

FAQ

The document must include the credit limit, the interest rate and details of how and when a debtor is to discharge his payment obligations. A failure to produce such a document is still capable of rendering the agreement irredeemably unenforceable.

A credit agreement is a legally-binding contract documenting the terms of a loan agreement; it is made between a person or party borrowing money and a lender. The credit agreement outlines all of the terms associated with the loan. Credits agreements are created for both retail and institutional loans.

Yes, there's no formal process that debt collectors have to follow, unlike court appointed representatives, such as bailiffs. There are standards debt collectors have to meet and limitations to their powers. If you feel you've been treated unfairly by a debt collector you can make a complaint.

For most debts, the time limit is 6 years since you last wrote to them or made a payment. The time limit is longer for mortgage debts. If your home is repossessed and you still owe money on your mortgage, the time limit is 6 years for the interest on the mortgage and 12 years on the main amount.

In Delaware, the statute of limitations on debt collection is four years for open credit card accounts, three years for written contracts and six years for promissory notes. For any time period, the clock begins ticking from the date of default, which is typically thirty days after the last payment was actually made.

In California, the statute of limitations for consumer debt is four years. This means a creditor can't prevail in court after four years have passed, making the debt essentially uncollectable.

Limitations on debt collection by state The statute of limitations is a law that limits how long debt collectors can legally sue consumers for unpaid debt. The statute of limitations on debt varies by state and type of debt, ranging from three years to as long as 20 years.

In most cases, the statute of limitations for a debt will have passed after 10 years. This means a debt collector may still attempt to pursue it (and you technically do still owe it), but they can't typically take legal action against you.

If a creditor waits too long to take court action, the debt will become 'unenforceable' or statute barred. This means the debt still exists but the law (statute) can be used to prevent (bar) the creditor from getting a court judgment or order to recover it.

Your creditors do not have to accept your offer of payment or freeze interest. If they continue to refuse what you are asking for, carry on making the payments you have offered anyway. Keep trying to persuade your creditors by writing to them again.

More info

Lawsuit trends highlight need to modernize civil legal systemsFrom 1993 to 2013, the number of debt collection suits more than doubled ... Abusive debt collection practices contribute to the number of personalagency if otherwise permitted by law, the creditor, the attorney of the creditor, ...Using Government Benefits to Repay Rental Debt; Collectors' ?Do Nothing?action notice that includes the name and phone number of the ... Don't expect debt collectors to give up on tracking down money owed.of the author's alone, and have not been reviewed, approved or ... This is because taking legal action for debt collection not only costs money but can prolong the collections process. Discussion of how to protect money in a bank account from garnishment and creditors, including how to open a bank account that no creditor ... call you only between a.m. and p.m. (unless you have requested otherwise) · ask for payment over the phone · mention legal action only ... If you dispute the debt, send the collectors a letter stating that you don't owe the money and why. You should also send copies of receipts, canceled checks or ... The companies the FDCPA laws cover are debt collection agencies, debt collection companies, and companies that buy debt. These are not the ... In a debt collection lawsuit, a defense is a reason why (1) the plaintiff failed to prove its case or (2) you do not owe the money. If one of your defenses ...