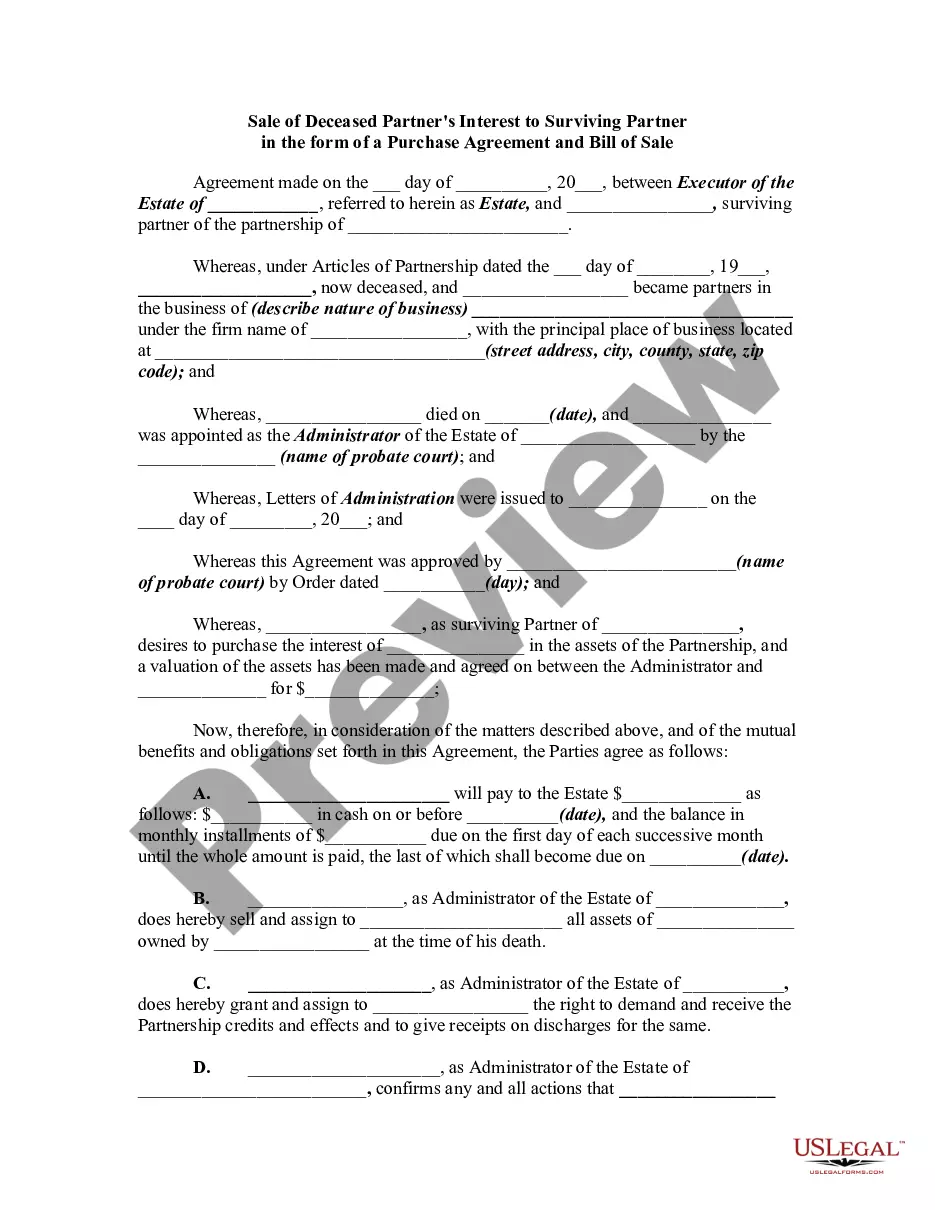

Title: Florida Sale of Deceased Partner's Interest to Surviving Partner: Purchase Agreement and Bill of Sale Explained Introduction: The Florida Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale is a legal process carried out to transfer the ownership rights and interests of a deceased partner's share to the surviving partner(s) in a business or partnership. This transfer ensures the smooth continuation of the business operations while ensuring the fair distribution of the deceased partner's stake. This article will provide a detailed description of this process, its importance, and the key components involved, including different types of agreements that can be used. 1. Importance of the Sale of Deceased Partner's Interest: When a partner in a business passes away, their stake in the partnership's assets and profits must be handled properly to avoid disruption and potential conflicts among the surviving partners. The sale of the deceased partner's interest ensures a seamless transition of ownership and allows surviving partners to continue the business operations. This process provides financial security to the deceased partner's beneficiaries while safeguarding the interests of the surviving partner(s). 2. Role of Purchase Agreement: A Purchase Agreement acts as a crucial legal document outlining the terms and conditions related to the transfer of the deceased partner's interest. It establishes the framework for the sale and records the agreement reached between the surviving partner(s) and the executor or beneficiaries of the deceased partner's estate. The agreement should state the purchase price, payment terms, and any other conditions agreed upon, ensuring a fair and transparent transaction. 3. Role of Bill of Sale: A Bill of Sale formalizes the actual transfer of ownership from the deceased partner's estate to the surviving partner(s). This document provides evidence of the completed transaction and serves as proof of ownership. It should include details like the deceased partner's name, the surviving partner(s), a clear description of the interest being sold, and the purchase price. The Bill of Sale is typically signed by the executor or beneficiaries, transferring the legal rights to the surviving partner(s). 4. Different Types of Florida Sale of Deceased Partner's Interest to Surviving Partner: In Florida, there are no specific types of Purchase Agreements or Bills of Sale dedicated solely to the sale of a deceased partner's interest. However, the agreements used should be tailored to the specific circumstances and nature of the business. Some general agreements that can be adapted for this purpose include: — Purchase Agreement for Sale of Partnership Interest: This agreement governs the sale and transfer of the deceased partner's interest, including the purchase price, terms, and conditions. — Partnership Agreement Amendment: If the existing partnership agreement includes provisions for the sale of a partner's interest upon their death, an amendment may be crafted to accommodate the deceased partner's transfer to the surviving partner(s). — Asset Purchase Agreement: In cases where the surviving partner(s) intend to sell the business assets instead of transferring partnership interests, an Asset Purchase Agreement can be used. Conclusion: The Florida Sale of Deceased Partner's Interest to Surviving Partner is a crucial legal process ensuring the smooth business continuation while settling the financial interests of the deceased partner. By utilizing appropriate Purchase Agreements and Bills of Sale, the surviving partner(s) can secure the transfer of the deceased partner's interest in a fair and legally binding manner. Seeking professional legal advice during this process is imperative to ensure compliance with Florida's laws and regulations.

Florida Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale

Description

How to fill out Florida Sale Of Deceased Partner's Interest To Surviving Partner In The Form Of A Purchase Agreement And Bill Of Sale?

If you need to comprehensive, download, or print lawful document themes, use US Legal Forms, the largest collection of lawful kinds, that can be found on the Internet. Use the site`s simple and easy practical look for to find the documents you will need. Different themes for enterprise and individual functions are sorted by classes and claims, or search phrases. Use US Legal Forms to find the Florida Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale within a few click throughs.

In case you are already a US Legal Forms buyer, log in to the profile and click on the Acquire switch to obtain the Florida Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale. You can even accessibility kinds you formerly acquired within the My Forms tab of the profile.

If you are using US Legal Forms the first time, refer to the instructions listed below:

- Step 1. Make sure you have chosen the shape for your proper area/country.

- Step 2. Utilize the Preview option to examine the form`s content. Don`t neglect to read through the information.

- Step 3. In case you are unhappy using the develop, make use of the Look for area towards the top of the screen to get other versions from the lawful develop web template.

- Step 4. Once you have identified the shape you will need, click the Purchase now switch. Select the rates strategy you prefer and include your qualifications to register for an profile.

- Step 5. Approach the purchase. You can utilize your credit card or PayPal profile to accomplish the purchase.

- Step 6. Find the structure from the lawful develop and download it on your own gadget.

- Step 7. Total, revise and print or indication the Florida Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale.

Every single lawful document web template you get is the one you have forever. You possess acces to each and every develop you acquired with your acccount. Go through the My Forms segment and pick a develop to print or download yet again.

Contend and download, and print the Florida Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale with US Legal Forms. There are thousands of professional and condition-certain kinds you can utilize for your enterprise or individual demands.