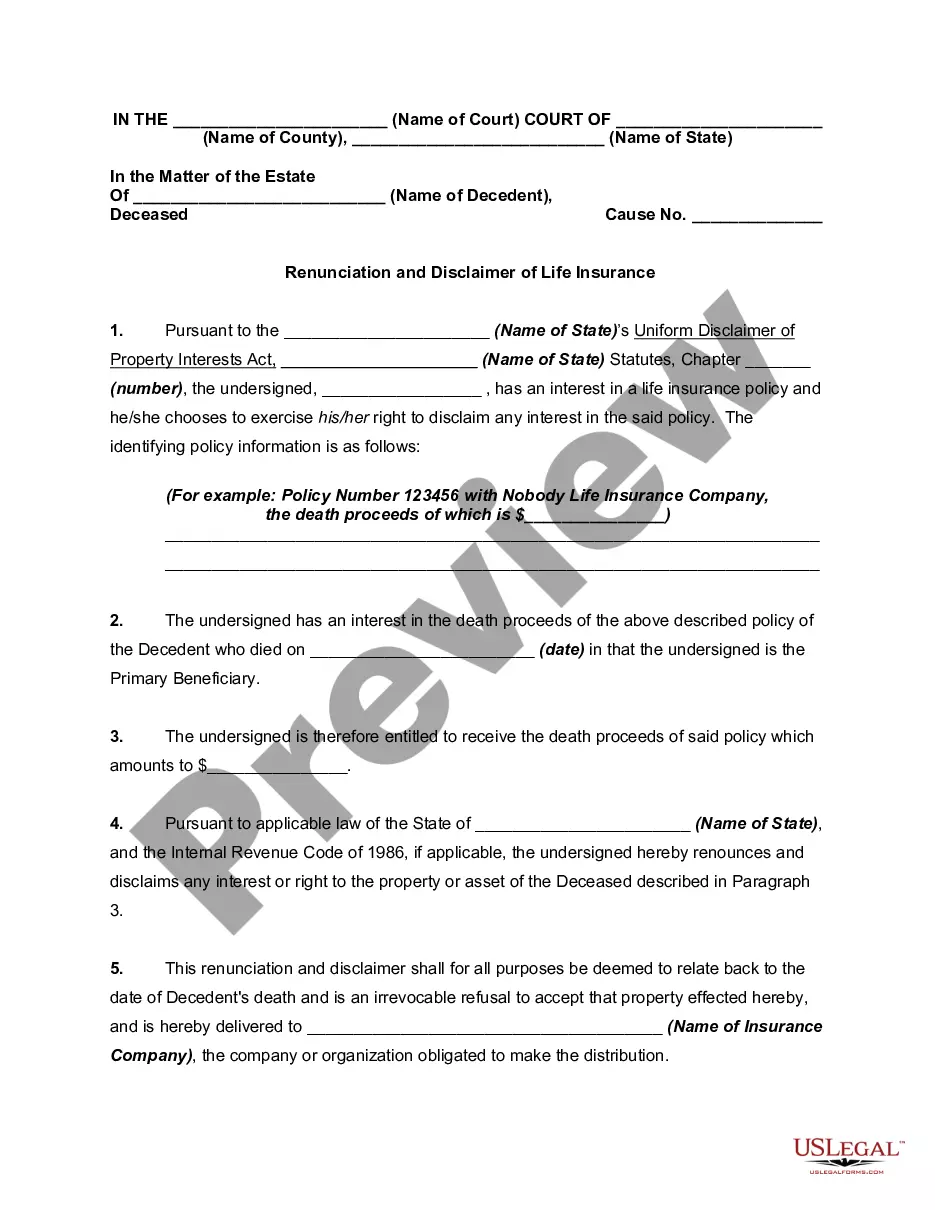

Disclaimers are used by those who receive property as heirs or legatees in an estate, or by beneficiaries of a non-testamentary transfer of property at death; for example, the beneficiaries of a life insurance policy. A disclaimer is simply a declaration by the person entitled to property that the interest in that property is disclaimed or renounced. A disclaimer allows the disclaiming heir or beneficiary to disclaim an interest in such a fashion that the right to the property that is disclaimed is treated as if it never existed.

The Uniform Disclaimers of Property Interests Act (which has been adopted by a number of states) provides the authority to make disclaimers, what interests may be disclaimed, the time when disclaimers are effective, and the effect on the distribution of the disclaimed property interests.

Florida Renunciation and Disclaimer of Interest in Life Insurance Proceeds is a legal document that allows an individual to refuse their right to receive the proceeds from a life insurance policy. This document is often used when the intended beneficiary chooses not to accept or should not receive the benefits due to various reasons. One type of Florida Renunciation and Disclaimer of Interest in Life Insurance Proceeds is the Renunciation of Interest. This occurs when a beneficiary decides to give up their claim to the life insurance proceeds. They formally reject any rights to the policy, and this relinquishment often occurs after the policyholder's death. Another type is the Disclaimer of Interest. This disclaimer is similar to renunciation but is typically used when the beneficiary wants to refuse the life insurance proceeds before the policyholder's death. The disclaimer ensures that the intended beneficiary does not become the recipient of the death benefits under any circumstance. By filing the Florida Renunciation and Disclaimer of Interest in Life Insurance Proceeds, the beneficiary legally notifies the insurance company that they are declining their rights to the policy's benefits. This legal document ensures that the benefits will be distributed to alternate beneficiaries or follow the predetermined order set within the policy, such as the contingent beneficiaries. It is important to note that renunciation or disclaimer must be made in writing, signed by the beneficiary, and submitted to the insurance company within a certain period, usually specified by state law or the policy terms. Without fulfilling these requirements, the renunciation or disclaimer may not be valid. Reasons for someone to utilize the Florida Renunciation and Disclaimer of Interest in Life Insurance Proceeds can vary. For instance, a beneficiary might choose to renounce their interest to ensure the benefits pass to specific individuals, perhaps in cases of divorce or financial planning reasons. Moreover, a disclaimer may be used when an intended beneficiary wants to avoid any potential tax consequences or to prevent the funds from being considered part of their estate. In conclusion, the Florida Renunciation and Disclaimer of Interest in Life Insurance Proceeds is an essential legal document that permits beneficiaries to decline their rights to receive life insurance proceeds. Both renunciation and disclaimer options offer different timing and circumstances for the beneficiary to refuse the benefits. Understanding these options and properly executing the necessary paperwork is crucial to ensure the smooth and accurate distribution of life insurance proceeds.Florida Renunciation and Disclaimer of Interest in Life Insurance Proceeds is a legal document that allows an individual to refuse their right to receive the proceeds from a life insurance policy. This document is often used when the intended beneficiary chooses not to accept or should not receive the benefits due to various reasons. One type of Florida Renunciation and Disclaimer of Interest in Life Insurance Proceeds is the Renunciation of Interest. This occurs when a beneficiary decides to give up their claim to the life insurance proceeds. They formally reject any rights to the policy, and this relinquishment often occurs after the policyholder's death. Another type is the Disclaimer of Interest. This disclaimer is similar to renunciation but is typically used when the beneficiary wants to refuse the life insurance proceeds before the policyholder's death. The disclaimer ensures that the intended beneficiary does not become the recipient of the death benefits under any circumstance. By filing the Florida Renunciation and Disclaimer of Interest in Life Insurance Proceeds, the beneficiary legally notifies the insurance company that they are declining their rights to the policy's benefits. This legal document ensures that the benefits will be distributed to alternate beneficiaries or follow the predetermined order set within the policy, such as the contingent beneficiaries. It is important to note that renunciation or disclaimer must be made in writing, signed by the beneficiary, and submitted to the insurance company within a certain period, usually specified by state law or the policy terms. Without fulfilling these requirements, the renunciation or disclaimer may not be valid. Reasons for someone to utilize the Florida Renunciation and Disclaimer of Interest in Life Insurance Proceeds can vary. For instance, a beneficiary might choose to renounce their interest to ensure the benefits pass to specific individuals, perhaps in cases of divorce or financial planning reasons. Moreover, a disclaimer may be used when an intended beneficiary wants to avoid any potential tax consequences or to prevent the funds from being considered part of their estate. In conclusion, the Florida Renunciation and Disclaimer of Interest in Life Insurance Proceeds is an essential legal document that permits beneficiaries to decline their rights to receive life insurance proceeds. Both renunciation and disclaimer options offer different timing and circumstances for the beneficiary to refuse the benefits. Understanding these options and properly executing the necessary paperwork is crucial to ensure the smooth and accurate distribution of life insurance proceeds.