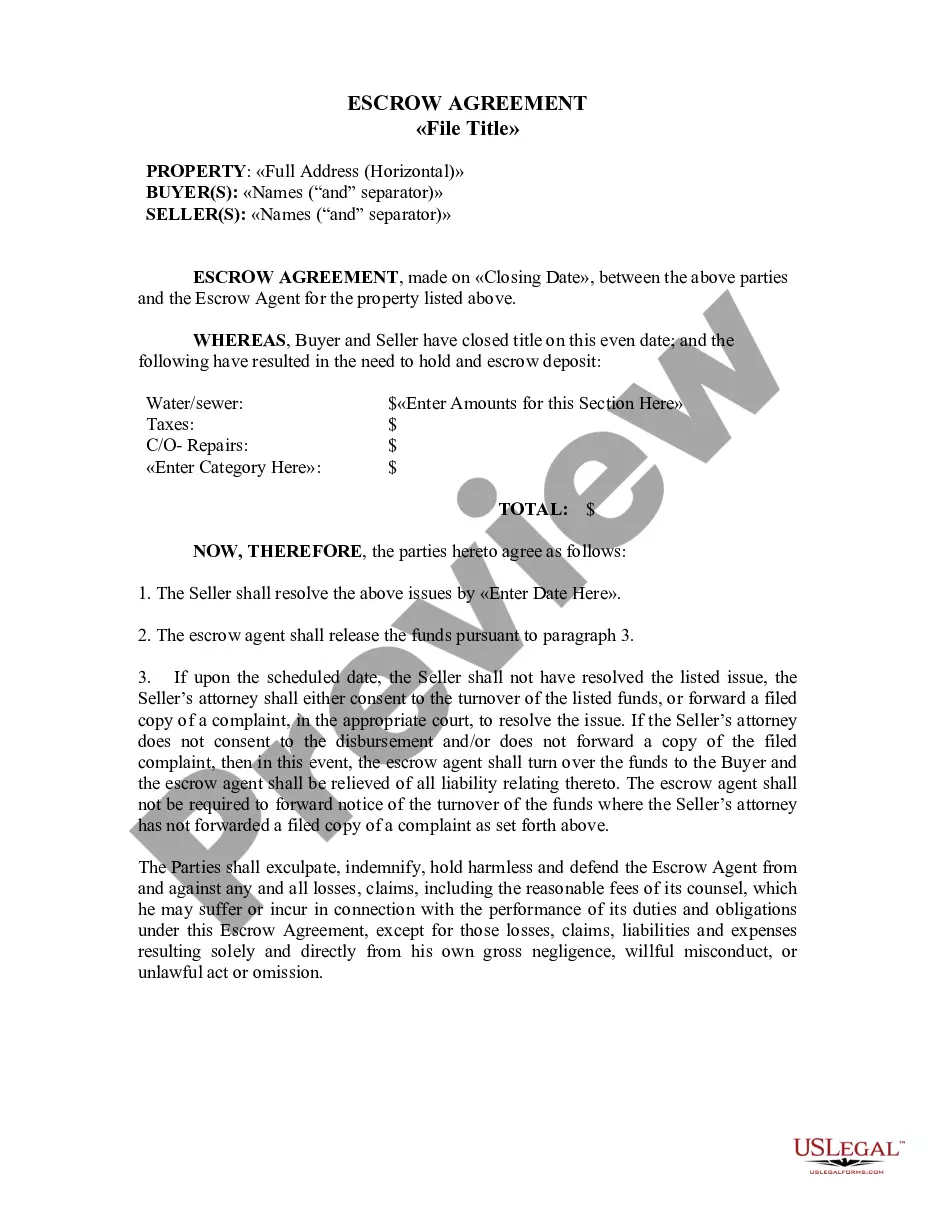

Escrow refers to a type of account in which the money, a mortgage or deed of trust, an existing promissory note secured by the real property, escrow "instructions" from both parties, an accounting of the funds and other documents necessary to complete the transaction by a date, is held by a third party, called an "escrow agent", until the conditions of an agreement are met. When the funding is complete and the deed is clear, the escrow agent will then record the deed to the buyer and deliver funds to the seller. The escrow agent or officer is an independent holder and agent for both parties who receives a fee for their services.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.