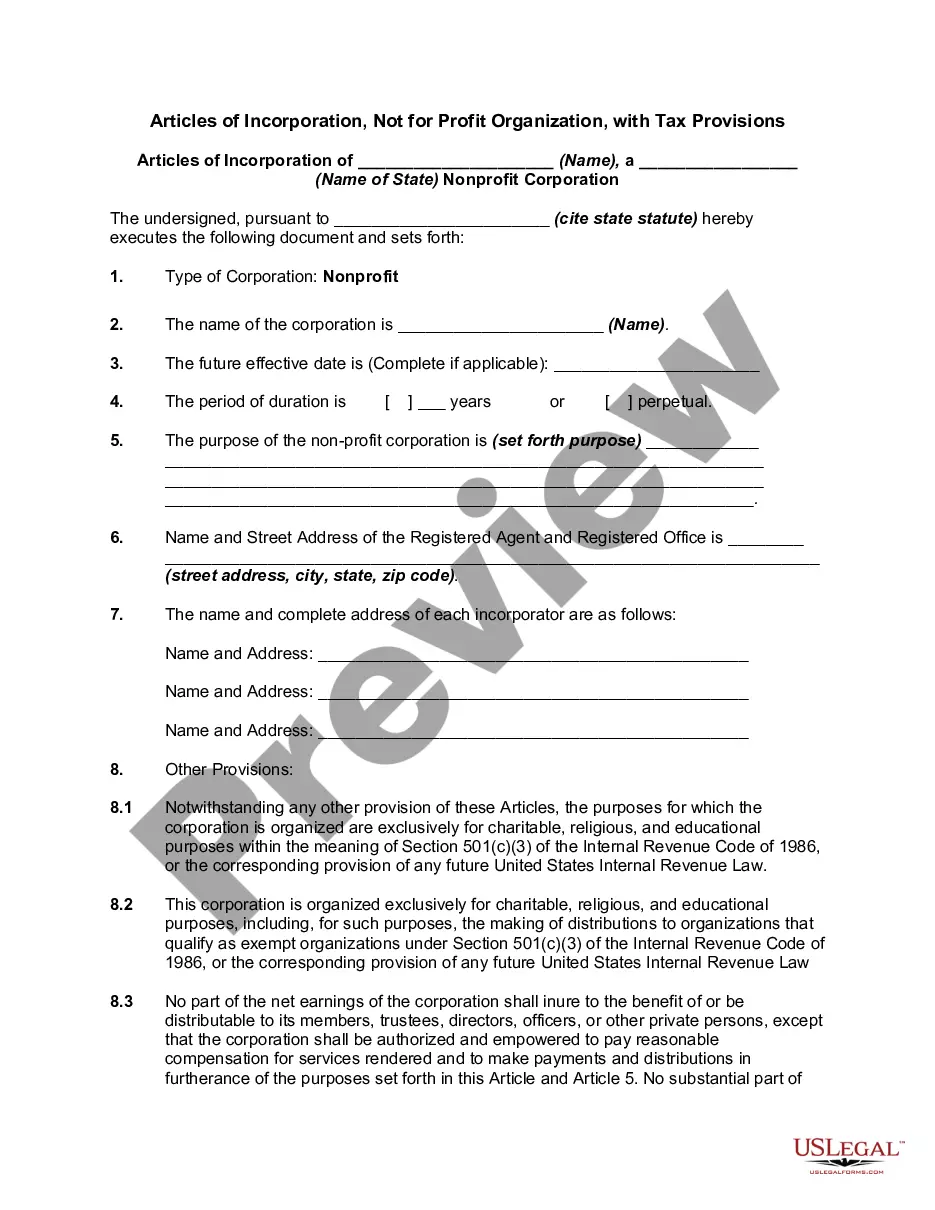

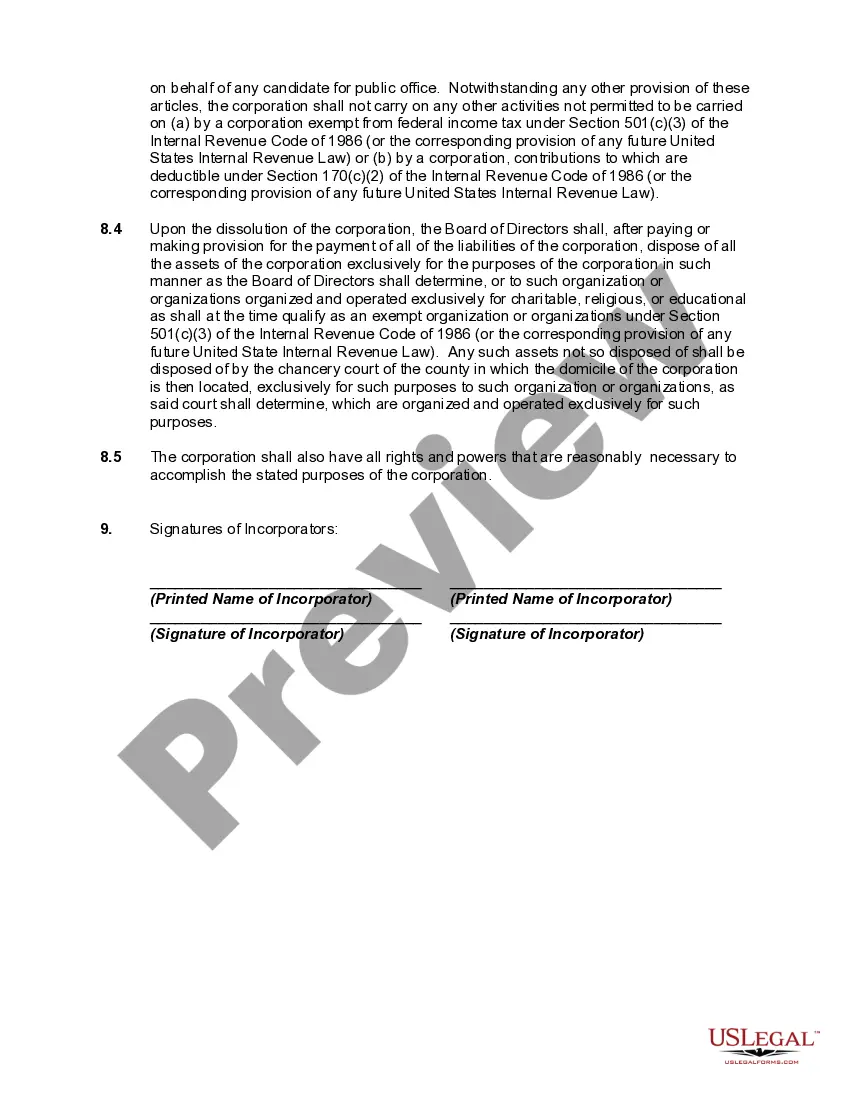

The proper form and necessary content of articles or certificates of incorporation for a nonprofit corporation depend largely on the requirements of the state nonprofit corporation act in the state of incorporation. Typically nonprofit corporations have no capital stock and therefore have members, not stockholders. Because federal tax-exempt status will be sought for most nonprofit corporations, the articles or certificate of incorporation must be carefully drafted to include specific language designed to ensure qualification for tax-exempt status.

Florida Articles of Incorporation, Not-for-Profit Organization, with Tax Provisions, serve as the foundational legal document required to establish a nonprofit entity in the state of Florida. These documents outline various essential aspects of the organization, including its purpose, structure, governance, and tax-related provisions. Nonprofit organizations that aim to achieve tax-exempt status must adhere to specific guidelines provided in the Florida Statutes and Internal Revenue Service (IRS) regulations. The two main types of Florida Articles of Incorporation for Not-for-Profit Organizations with Tax Provisions are: 1. Articles of Incorporation for a Florida Not-for-Profit Corporation: This type of Articles of Incorporation is relevant for organizations seeking to establish themselves as a nonprofit corporation in Florida. It outlines essential information, such as the organization's name, its purpose, and the registered agent's details. Additionally, it should include provisions ensuring compliance with federal and state tax laws to qualify for tax-exempt status. These provisions establish that the corporation will operate exclusively in accordance with section 501(c)(3) of the Internal Revenue Code (IRC). 2. Articles of Incorporation for a Florida Religious, Charitable, Educational, Scientific, or Literary Organization: This specific type of Articles of Incorporation caters to organizations that intend to operate exclusively for religious, charitable, educational, scientific, or literary purposes. The format is similar to the general Articles of Incorporation, with additional sections addressing the organization's religious nature or primary purpose, provisions to ensure compliance with tax-exempt status requirements, and how any assets should be distributed upon dissolution. These provisions aim to meet the criteria outlined in section 501(c)(3) of the IRC. Keywords: Florida Articles of Incorporation, Not-for-Profit Organization, Tax Provisions, nonprofit corporation, tax-exempt status, Florida Statutes, Internal Revenue Service, IRS regulations, nonprofit organization, registered agent, 501(c)(3), religious organization, charitable organization, educational organization, scientific organization, literary organization, dissolution, assets.