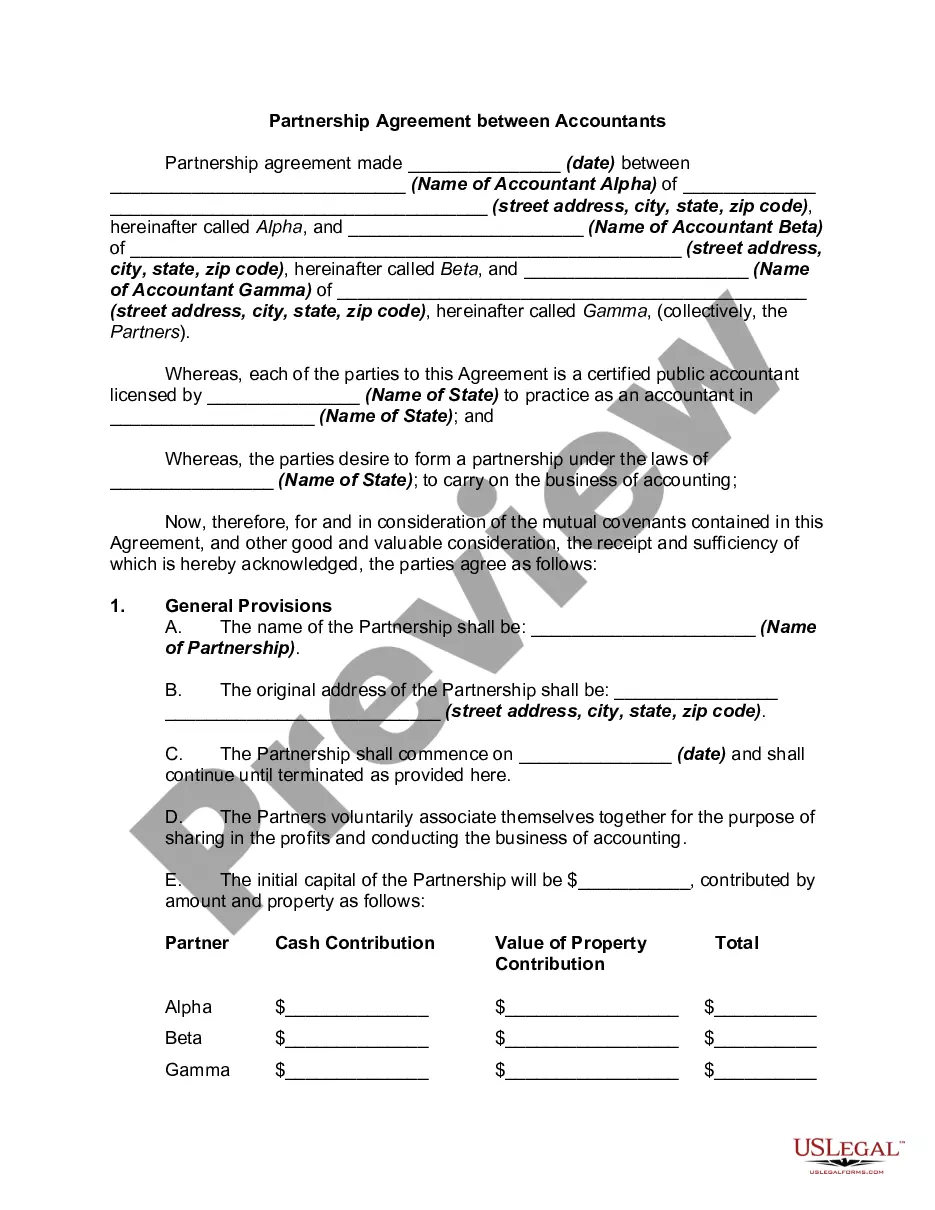

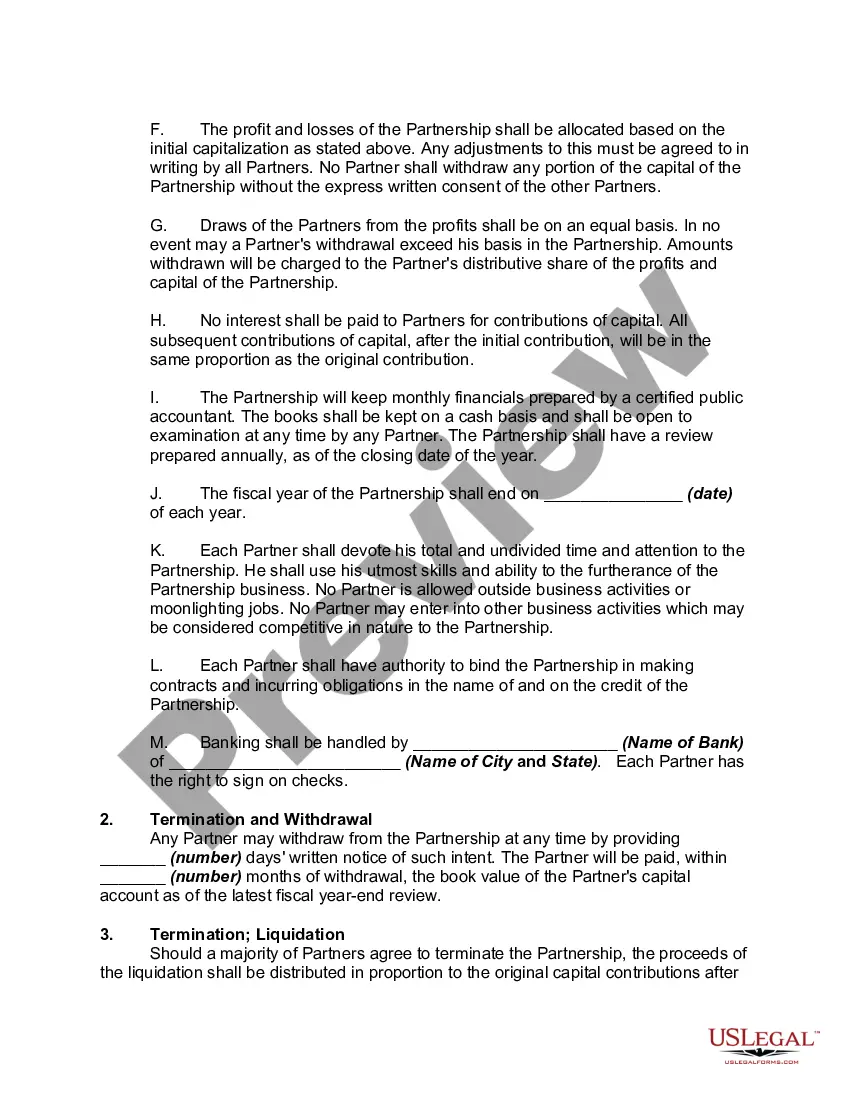

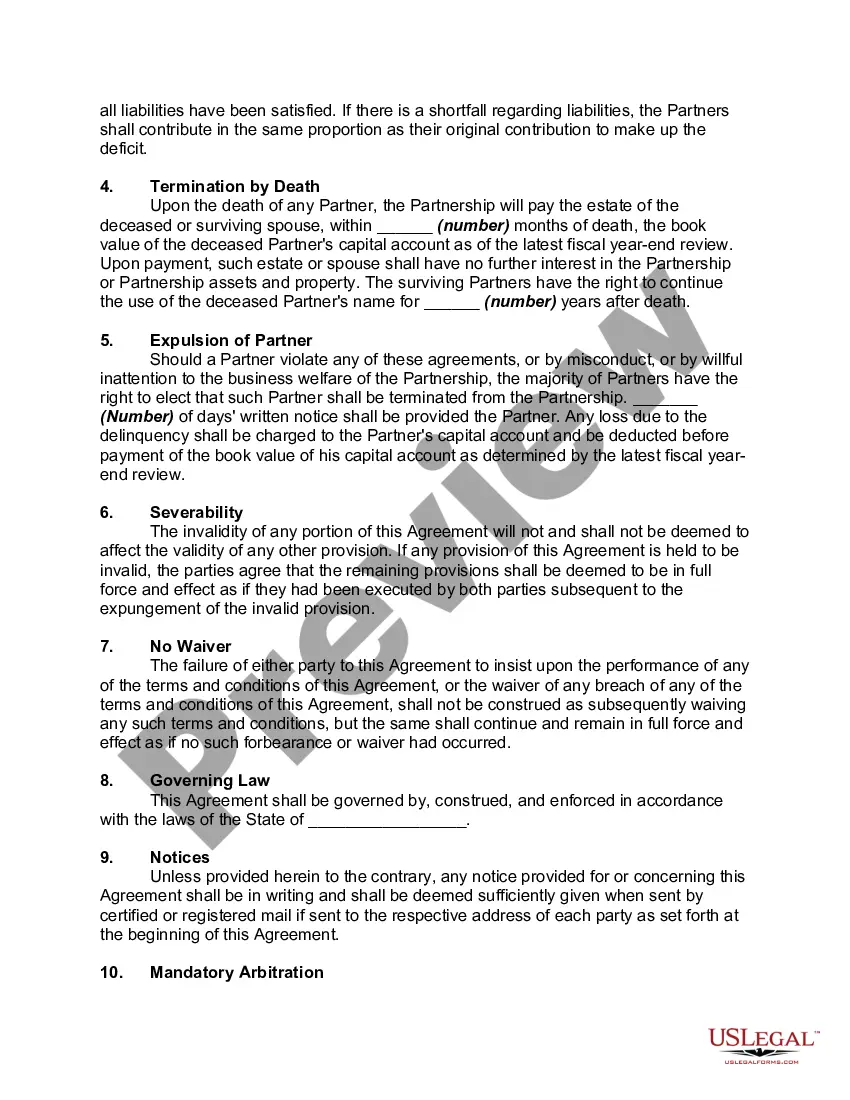

Partnership agreements are written documents that explicitly detail the relationship between the business partners and their individual obligations and contributions to the partnership. Since partnership agreements should cover all possible business situations that could arise during the partnership's life, the documents are often complex; legal counsel in drafting and reviewing the finished contract is generally recommended. If a partnership does not have a partnership agreement in place when it dissolves, the guidelines of the Uniform Partnership Act and various state laws will determine how the assets and debts of the partnership are distributed.

A Florida Partnership Agreement Between Accountants is a legally binding contract that outlines the terms and conditions of a partnership between two or more accountants in the state of Florida. It defines the rights, responsibilities, and obligations of each partner, as well as the distribution of profits and losses within the partnership. In Florida, there are several types of partnership agreements that accountants can enter into, such as: 1. General Partnership Agreement: This is the most common type of partnership agreement where partners share equal rights and responsibilities, as well as profits and losses. The partnership is not a separate legal entity from the partners involved. 2. Limited Partnership Agreement: In this type of agreement, there are two types of partners involved — general partners and limited partners. General partners have unlimited liability and manage the day-to-day operations, while limited partners contribute capital but have limited liability and are not involved in the management of the partnership. 3. Limited Liability Partnership Agreement: This agreement provides limited liability protection to partners, meaning their personal assets are protected from business liabilities. All partners can actively participate in running the partnership while enjoying limited personal liability. 4. Limited Liability Limited Partnership Agreement: This is a hybrid form of partnership that combines elements of both the limited partnership and limited liability partnership. It offers limited liability protection to all partners while allowing them to actively manage the business. Regardless of the type of partnership agreement, it is essential to include the following provisions: — Partnership Name and Purpose: Clearly state the name of the partnership and outline its purpose or business activities. — Partner Contributions: Specify the amount and nature of capital contributions made by each partner to the partnership. — Profit and Loss Sharing: Detail how profits and losses will be allocated among the partners, usually in proportion to their capital contributions or as agreed upon. — Management and Decision-Making: Determine how decision-making powers will be shared among partners and whether certain partners will have managing authority. — Partner Withdrawal or Dissolution: Outline the process for partners to withdraw from the partnership or dissolve it completely, including provisions for buyouts and the distribution of assets. — Dispute Resolution: Include a mechanism for resolving disputes or disagreements between partners, such as through arbitration or mediation. — Non-Compete and Non-Disclosure Clauses: Protect the partnership's trade secrets and client base by including non-compete and non-disclosure clauses. In conclusion, a Florida Partnership Agreement Between Accountants is a vital document that legally establishes the rights and obligations of partners in a business venture. Whether it is a general partnership agreement, limited partnership agreement, limited liability partnership agreement, or limited liability limited partnership agreement, accountants should carefully craft the terms to ensure a mutually beneficial and legally secure partnership.A Florida Partnership Agreement Between Accountants is a legally binding contract that outlines the terms and conditions of a partnership between two or more accountants in the state of Florida. It defines the rights, responsibilities, and obligations of each partner, as well as the distribution of profits and losses within the partnership. In Florida, there are several types of partnership agreements that accountants can enter into, such as: 1. General Partnership Agreement: This is the most common type of partnership agreement where partners share equal rights and responsibilities, as well as profits and losses. The partnership is not a separate legal entity from the partners involved. 2. Limited Partnership Agreement: In this type of agreement, there are two types of partners involved — general partners and limited partners. General partners have unlimited liability and manage the day-to-day operations, while limited partners contribute capital but have limited liability and are not involved in the management of the partnership. 3. Limited Liability Partnership Agreement: This agreement provides limited liability protection to partners, meaning their personal assets are protected from business liabilities. All partners can actively participate in running the partnership while enjoying limited personal liability. 4. Limited Liability Limited Partnership Agreement: This is a hybrid form of partnership that combines elements of both the limited partnership and limited liability partnership. It offers limited liability protection to all partners while allowing them to actively manage the business. Regardless of the type of partnership agreement, it is essential to include the following provisions: — Partnership Name and Purpose: Clearly state the name of the partnership and outline its purpose or business activities. — Partner Contributions: Specify the amount and nature of capital contributions made by each partner to the partnership. — Profit and Loss Sharing: Detail how profits and losses will be allocated among the partners, usually in proportion to their capital contributions or as agreed upon. — Management and Decision-Making: Determine how decision-making powers will be shared among partners and whether certain partners will have managing authority. — Partner Withdrawal or Dissolution: Outline the process for partners to withdraw from the partnership or dissolve it completely, including provisions for buyouts and the distribution of assets. — Dispute Resolution: Include a mechanism for resolving disputes or disagreements between partners, such as through arbitration or mediation. — Non-Compete and Non-Disclosure Clauses: Protect the partnership's trade secrets and client base by including non-compete and non-disclosure clauses. In conclusion, a Florida Partnership Agreement Between Accountants is a vital document that legally establishes the rights and obligations of partners in a business venture. Whether it is a general partnership agreement, limited partnership agreement, limited liability partnership agreement, or limited liability limited partnership agreement, accountants should carefully craft the terms to ensure a mutually beneficial and legally secure partnership.