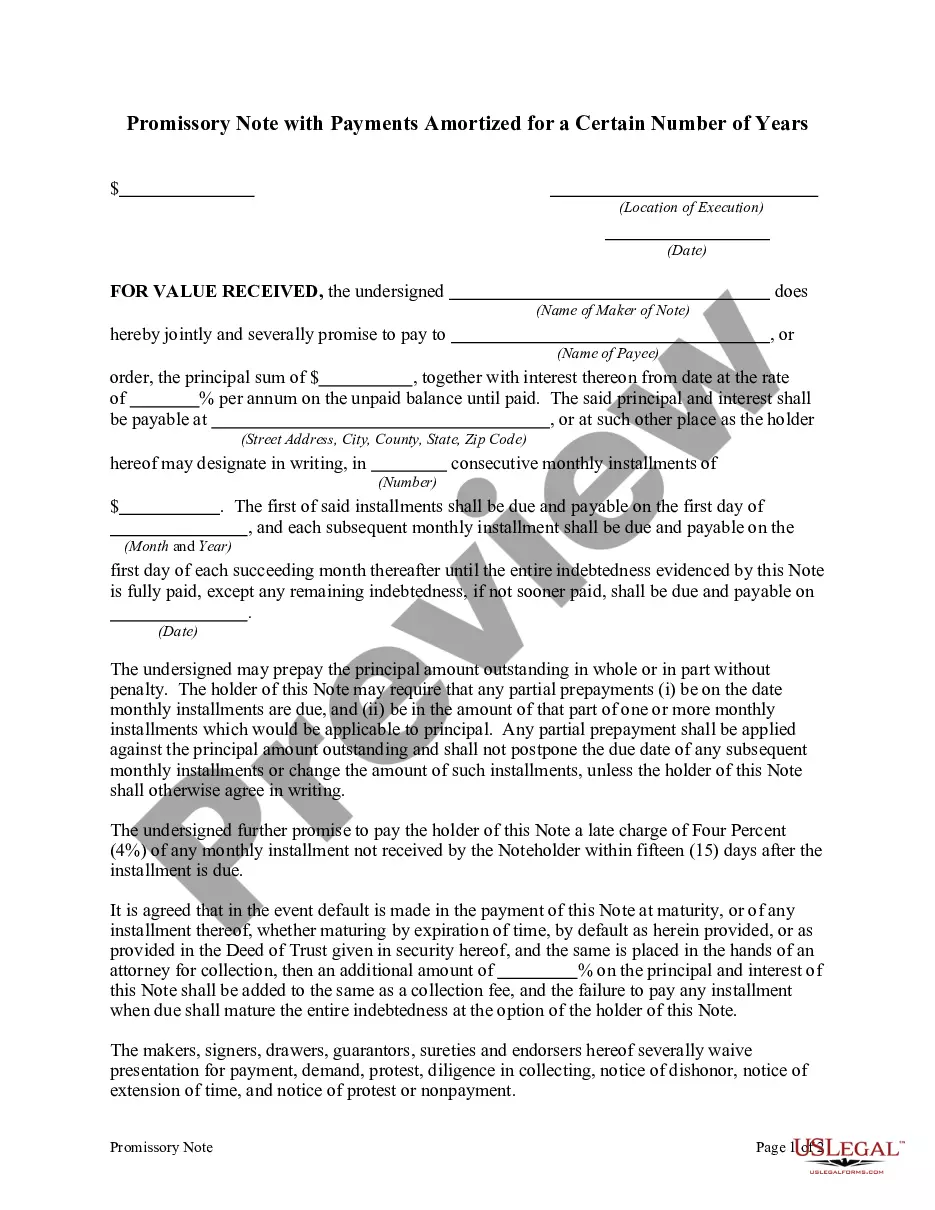

A Florida Promissory Note with Payments Amortized for a Certain Number of Years is a legally binding document outlining the terms and conditions between a borrower and a lender for a loan to be repaid in regular installments over a specified period. This type of promissory note includes specific provisions for amortization, meaning that the payments are structured to gradually reduce the outstanding principal amount over time. Florida's law recognizes different types of promissory notes with payments amortized for a certain number of years, including: 1. Fixed-Rate Promissory Note: This type of promissory note in Florida has a predetermined interest rate that remains constant throughout the loan term. The borrower makes equal monthly payments that include both principal and interest, ensuring a consistent payment schedule over the specified period. 2. Adjustable-Rate Promissory Note: In contrast to fixed-rate promissory notes, an adjustable-rate promissory note allows for the interest rate to change periodically based on a specified index or market conditions. This means the borrower's monthly payments may fluctuate, typically resulting in adjustments at set intervals, such as annually or every few years. 3. Balloon Promissory Note: A balloon promissory note is structured to have regular payments for a certain number of years, typically allowing smaller monthly payments initially. However, at the end of the specified term, there is a large final payment (balloon payment) that the borrower must make to fully repay the loan. Balloon notes are often used in situations where a borrower expects to have the means to make a lump sum payment in the future. 4. Graduated Payment Promissory Note: This type of promissory note starts with lower monthly payments that increase over time, usually at predetermined intervals. It may suit borrowers who anticipate their income or financial capabilities to rise in the future but require more manageable initial payments. When drafting a Florida Promissory Note with Payments Amortized for a Certain Number of Years, it is crucial to include essential details such as the loan amount, interest rate, payment frequency, repayment term, and any applicable late fees or penalties. Both the borrower and lender must sign the promissory note to make it legally binding. It is advisable to consult with a qualified legal professional to ensure compliance with Florida's specific regulations and requirements for promissory notes.

Florida Promissory Note with Payments Amortized for a Certain Number of Years

Description

How to fill out Florida Promissory Note With Payments Amortized For A Certain Number Of Years?

You can spend hrs on the Internet searching for the lawful document format that fits the federal and state specifications you will need. US Legal Forms supplies thousands of lawful types that happen to be evaluated by professionals. It is possible to acquire or printing the Florida Promissory Note with Payments Amortized for a Certain Number of Years from your assistance.

If you already have a US Legal Forms profile, it is possible to log in and then click the Obtain key. After that, it is possible to full, modify, printing, or indication the Florida Promissory Note with Payments Amortized for a Certain Number of Years. Each lawful document format you purchase is your own property eternally. To get yet another copy associated with a obtained type, proceed to the My Forms tab and then click the related key.

If you work with the US Legal Forms internet site the very first time, adhere to the easy instructions below:

- Initial, ensure that you have selected the correct document format for the county/town of your choosing. See the type description to ensure you have chosen the correct type. If accessible, use the Preview key to check throughout the document format as well.

- If you want to find yet another version in the type, use the Search field to obtain the format that fits your needs and specifications.

- Upon having identified the format you want, just click Get now to carry on.

- Select the prices strategy you want, type your qualifications, and sign up for a free account on US Legal Forms.

- Total the transaction. You may use your bank card or PayPal profile to purchase the lawful type.

- Select the structure in the document and acquire it to the product.

- Make changes to the document if required. You can full, modify and indication and printing Florida Promissory Note with Payments Amortized for a Certain Number of Years.

Obtain and printing thousands of document themes using the US Legal Forms website, that offers the biggest collection of lawful types. Use expert and express-particular themes to tackle your organization or personal requirements.