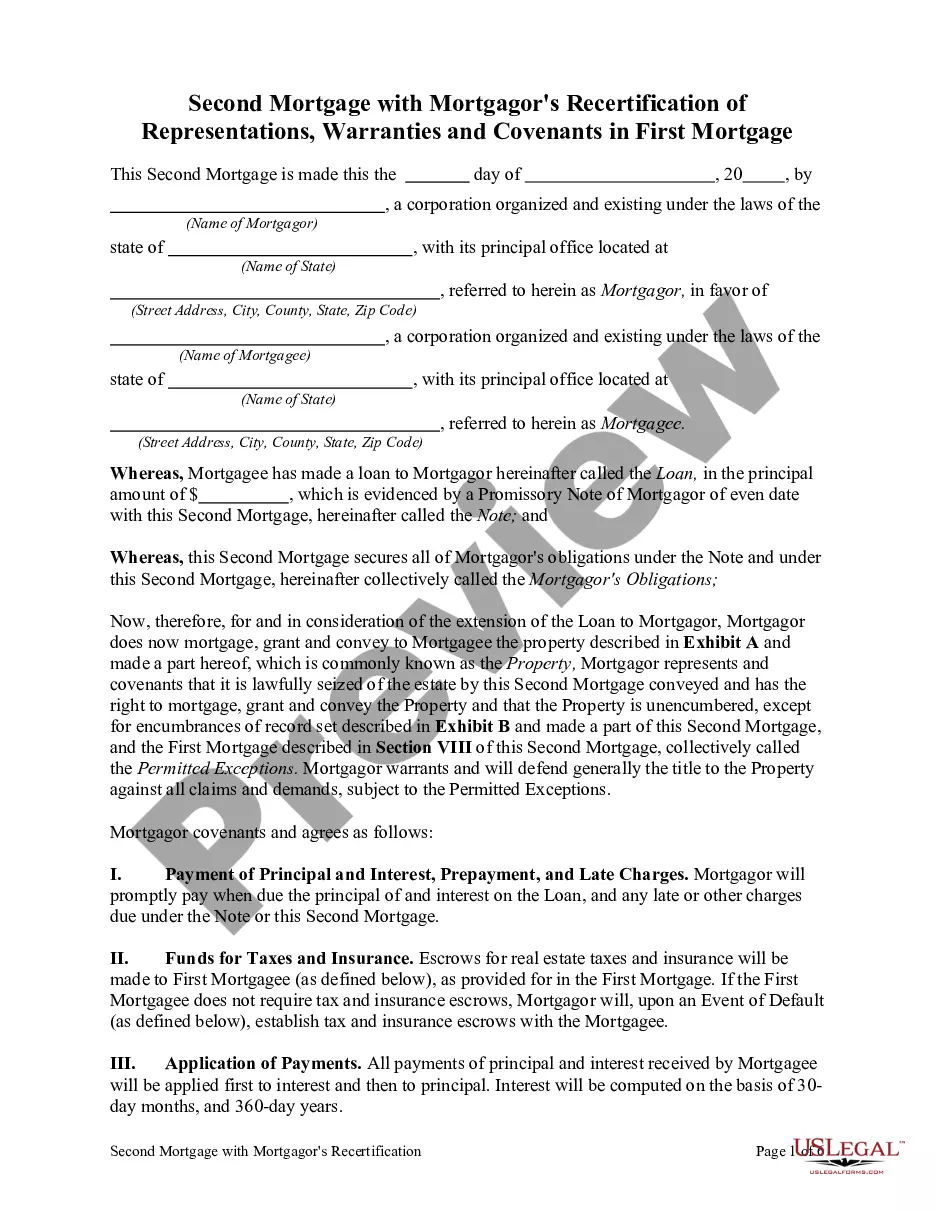

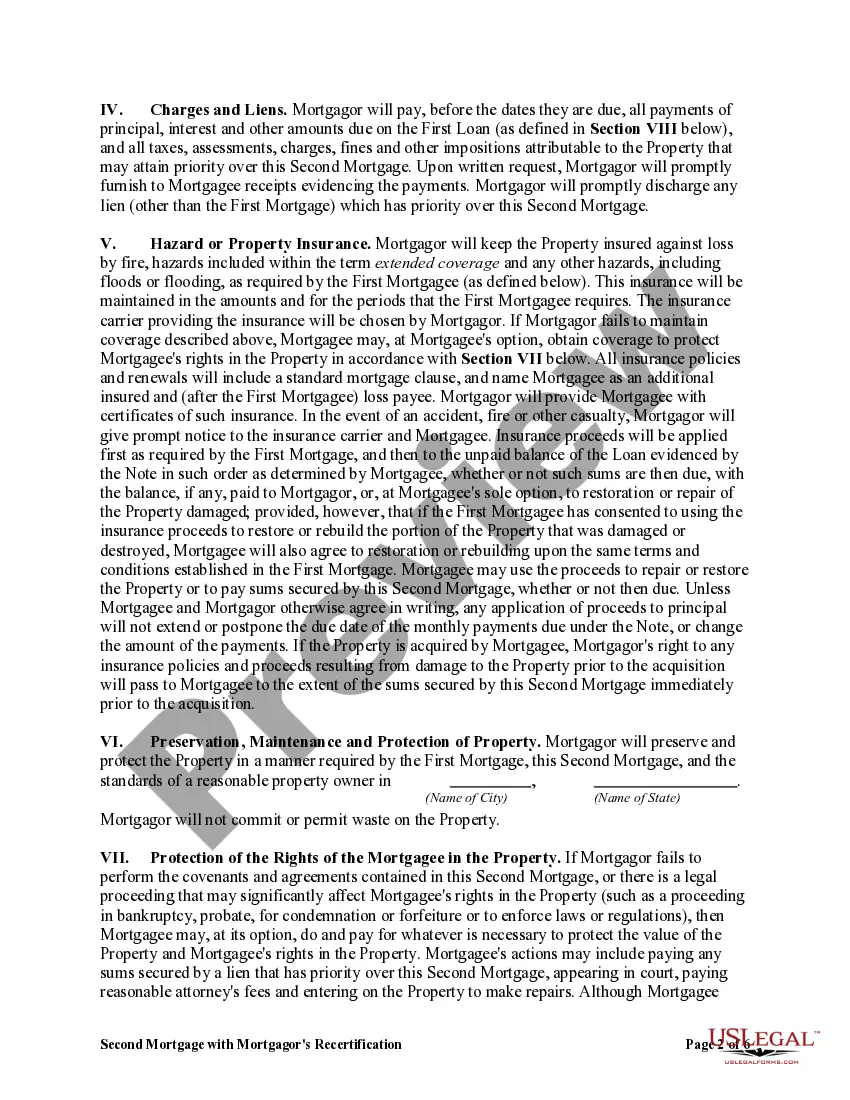

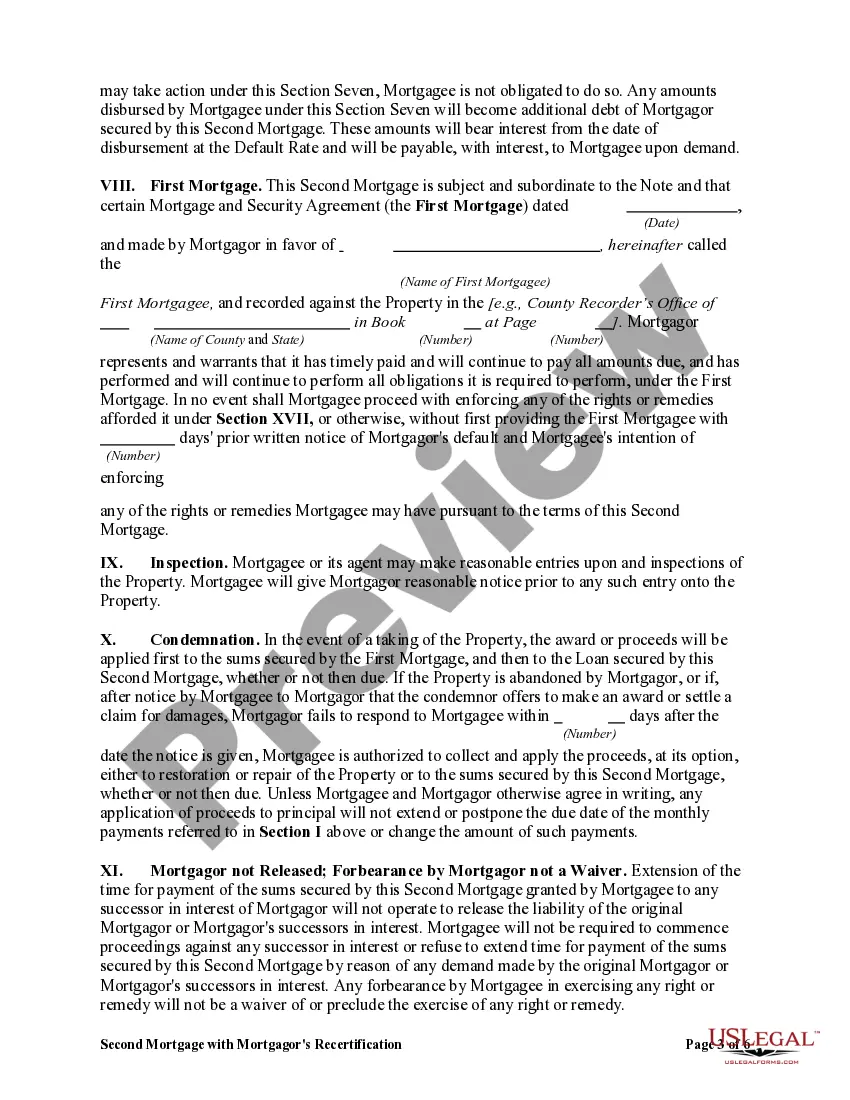

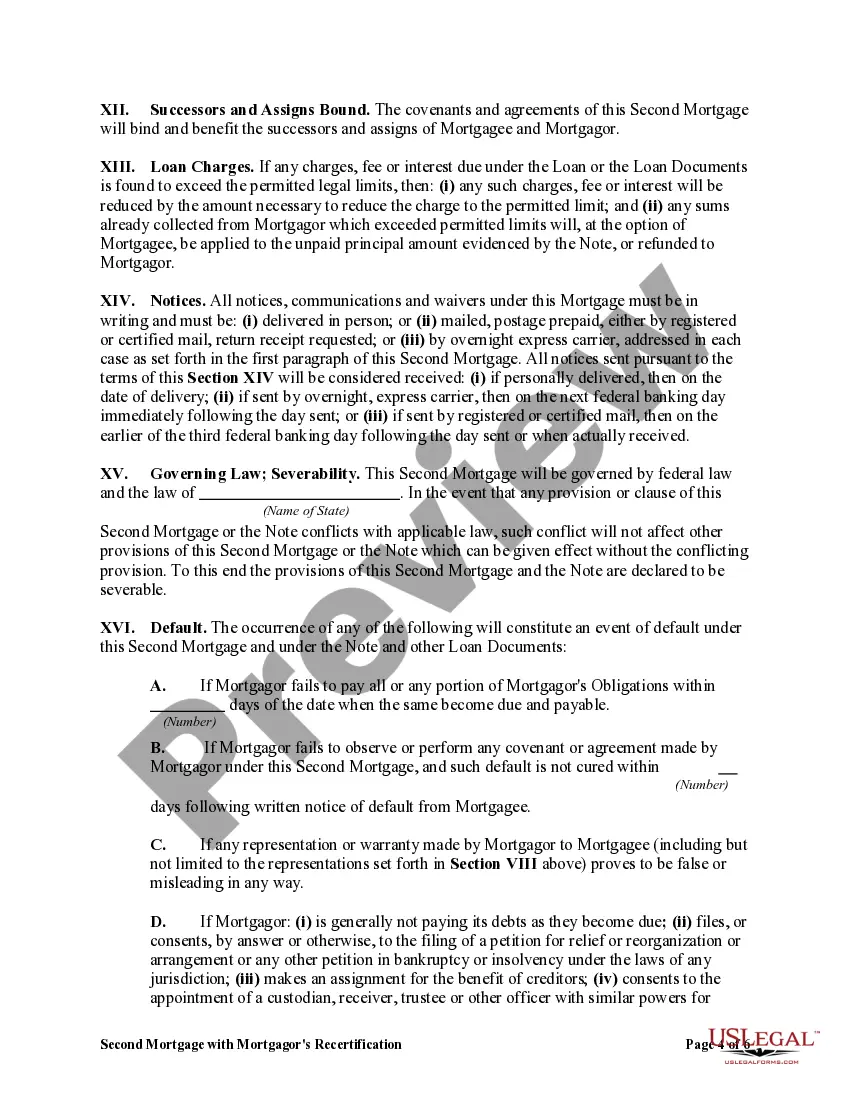

A Florida Second Mortgage with Mortgagor's Recertification of Representations, Warranties, and Covenants in First Mortgage is a legal document that outlines the terms and conditions of a second mortgage in the state of Florida. This mortgage is taken out by homeowners who already have an existing first mortgage on their property. Keywords: Florida, second mortgage, mortgagor's recertification, representations, warranties, covenants, first mortgage. Types of Florida Second Mortgages with Mortgagor's Recertification of Representations, Warranties, and Covenants in First Mortgage: 1. Fixed-Rate Second Mortgage: This type of second mortgage offers a fixed interest rate throughout the term of the loan. Borrowers can recertify their representations, warranties, and covenants in their existing first mortgage, giving lenders additional security. 2. Adjustable-Rate Second Mortgage: In contrast to a fixed-rate second mortgage, this type of mortgage has an adjustable interest rate that may fluctuate over time. The mortgagor will have to recertify their representations, warranties, and covenants in the first mortgage to accommodate any adjustments in the interest rate. 3. Home Equity Line of Credit (HELOT): A HELOT acts as a revolving line of credit, allowing homeowners to borrow against the equity in their property. This type of second mortgage offers flexibility for homeowners who need access to funds for various purposes such as home renovations or educational expenses. Recertification of representations, warranties, and covenants in the first mortgage may be required before establishing a HELOT. 4. Balloon Payment Second Mortgage: This type of second mortgage allows borrowers to make lower monthly payments for an agreed-upon term, but with a substantial final payment (balloon payment) due at the end of the loan term. Mortgagors will typically need to recertify their representations, warranties, and covenants in the first mortgage to secure this type of loan. 5. Reverse Mortgage: Reverse mortgages are available to homeowners aged 62 and older and enable them to convert a portion of their home equity into cash. Lenders may require mortgagors to recertify their representations, warranties, and covenants in the first mortgage to ensure the property meets certain criteria and qualifications for a reverse mortgage. Regardless of the type of second mortgage, the purpose of the mortgagor's recertification of representations, warranties, and covenants in the first mortgage is to reaffirm the accuracy and truthfulness of the original mortgage agreement and to provide additional protection for the lender. It ensures that the borrower is still in compliance with the terms and conditions set forth in the initial mortgage and that there have been no changes or events that may affect the lender's rights or the borrower's obligations.

Florida Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage

Description

How to fill out Florida Second Mortgage With Mortgagor's Recertification Of Representations, Warranties And Covenants In First Mortgage?

Finding the right legal document format can be a have a problem. Obviously, there are tons of templates available on the net, but how do you obtain the legal develop you require? Make use of the US Legal Forms web site. The support provides thousands of templates, including the Florida Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage, which you can use for business and private requires. All the varieties are checked out by specialists and meet up with federal and state needs.

Should you be already listed, log in in your bank account and then click the Down load key to get the Florida Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage. Utilize your bank account to search through the legal varieties you might have purchased earlier. Check out the My Forms tab of your respective bank account and acquire an additional version of the document you require.

Should you be a fresh end user of US Legal Forms, allow me to share simple recommendations that you should stick to:

- Initial, ensure you have selected the appropriate develop for your metropolis/region. You are able to look through the shape while using Review key and browse the shape explanation to guarantee it is the best for you.

- If the develop will not meet up with your needs, use the Seach industry to obtain the correct develop.

- Once you are certain that the shape is acceptable, select the Get now key to get the develop.

- Select the rates prepare you want and type in the necessary information and facts. Create your bank account and purchase the transaction making use of your PayPal bank account or Visa or Mastercard.

- Select the submit formatting and down load the legal document format in your gadget.

- Full, revise and produce and signal the acquired Florida Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage.

US Legal Forms will be the biggest catalogue of legal varieties in which you can find various document templates. Make use of the company to down load appropriately-manufactured paperwork that stick to state needs.