Florida Loan Guaranty Agreement

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Loan Guaranty Agreement?

Have you been in a placement in which you need files for either business or person functions just about every day? There are a lot of lawful document templates available on the Internet, but discovering kinds you can depend on isn`t effortless. US Legal Forms offers thousands of develop templates, like the Florida Loan Guaranty Agreement, which can be published to satisfy state and federal specifications.

When you are presently familiar with US Legal Forms website and also have a merchant account, basically log in. Afterward, you can acquire the Florida Loan Guaranty Agreement template.

Unless you come with an bank account and would like to begin using US Legal Forms, follow these steps:

- Get the develop you want and make sure it is for your appropriate metropolis/area.

- Use the Preview option to examine the shape.

- Read the explanation to actually have chosen the correct develop.

- In case the develop isn`t what you`re searching for, use the Search field to get the develop that fits your needs and specifications.

- Once you find the appropriate develop, simply click Acquire now.

- Pick the costs prepare you need, fill in the required info to produce your account, and pay for the order using your PayPal or credit card.

- Select a practical data file formatting and acquire your version.

Discover each of the document templates you possess bought in the My Forms menu. You can aquire a further version of Florida Loan Guaranty Agreement anytime, if needed. Just go through the required develop to acquire or printing the document template.

Use US Legal Forms, the most substantial collection of lawful varieties, to save lots of time as well as stay away from errors. The service offers expertly manufactured lawful document templates which can be used for a variety of functions. Generate a merchant account on US Legal Forms and start making your way of life a little easier.

Form popularity

FAQ

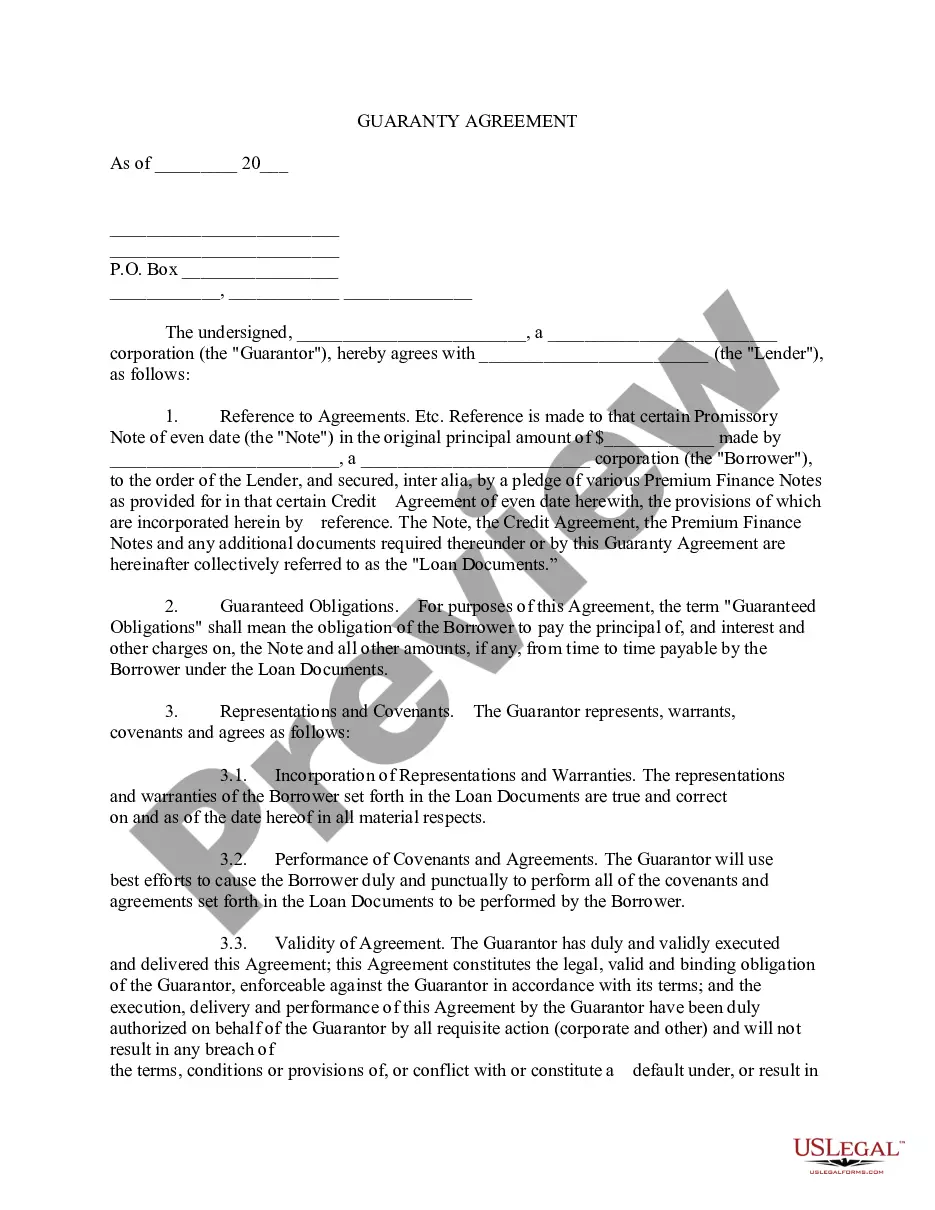

A loan guarantee is a legally binding commitment to pay a debt in the event the borrower defaults. This most often occurs between family members, where the borrower can't obtain a loan because of a lack of income or down payment, or due to a poor credit rating.

Under Florida law, the guarantor can be held liable only when a court determines the guaranty is lawful and the alleged debt is actually owed. In other words, a guarantor may not escape liability if the absolute guarantee is lawful and the party owing the underlying debt is liable under that debt.

Under Florida law, the guarantor can be held liable only when a court determines the guaranty is lawful and the alleged debt is actually owed. In other words, a guarantor may not escape liability if the absolute guarantee is lawful and the party owing the underlying debt is liable under that debt.

In a finance or lending context, a guarantor would be forced to answer for the debt or default of the debtor to the creditor, if a debtor does not fulfill an obligation on their part to repay their debt.

And, like in any breach of contract case, a plaintiff in a case claiming the breach of a guaranty must prove: (1) the existence of the contract (i.e., the guaranty); (2) a breach of the contract (i.e., a failure of the guarantor to pay); and (3) damages resulting from the breach (i.e., the amount remaining due).

A guaranty is a legal commitment by one party (the guarantor) to take responsibility for another party's (the debtor) financial obligation if that debtor fails to meet their obligations. If the debtor defaults on their payments, the guarantor becomes responsible for fulfilling those financial obligations.