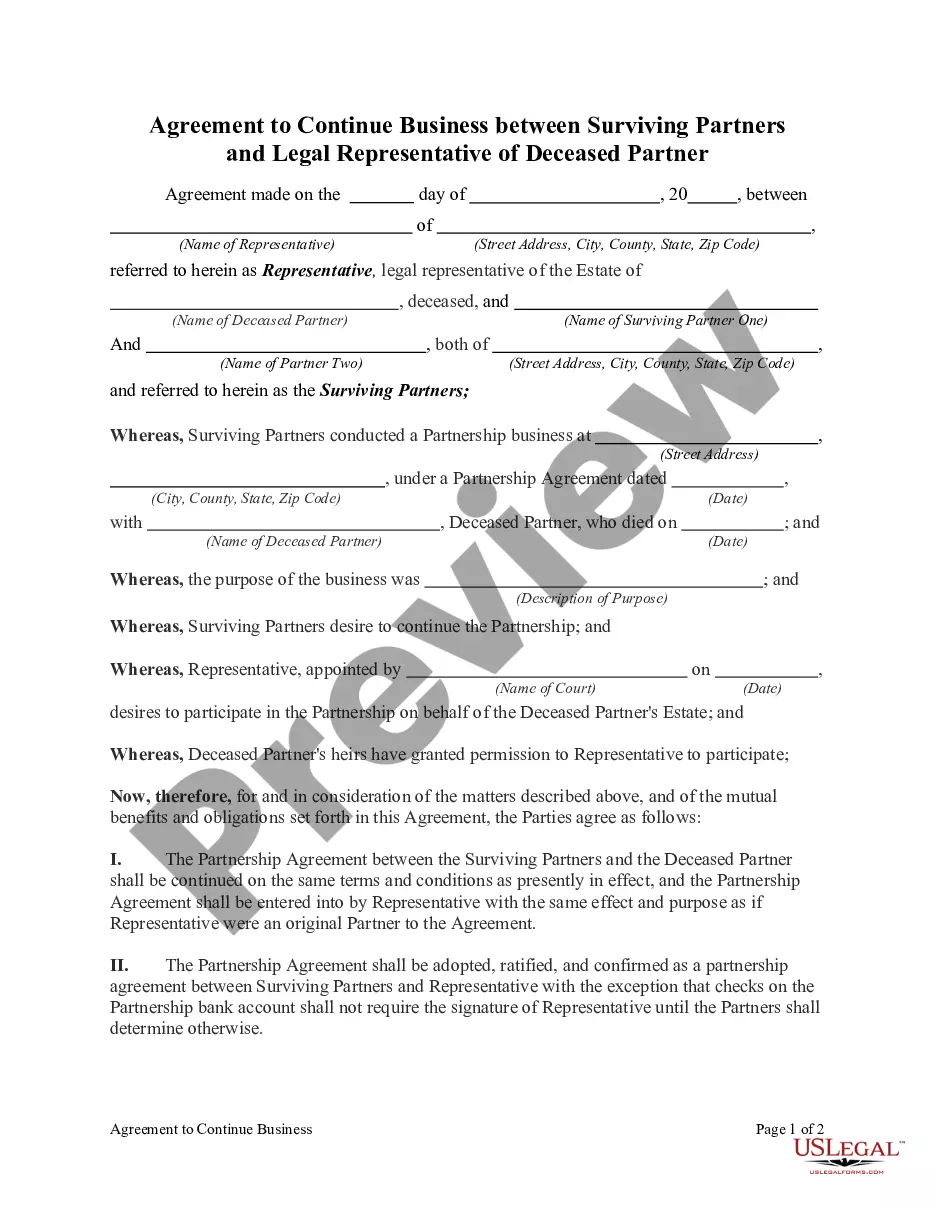

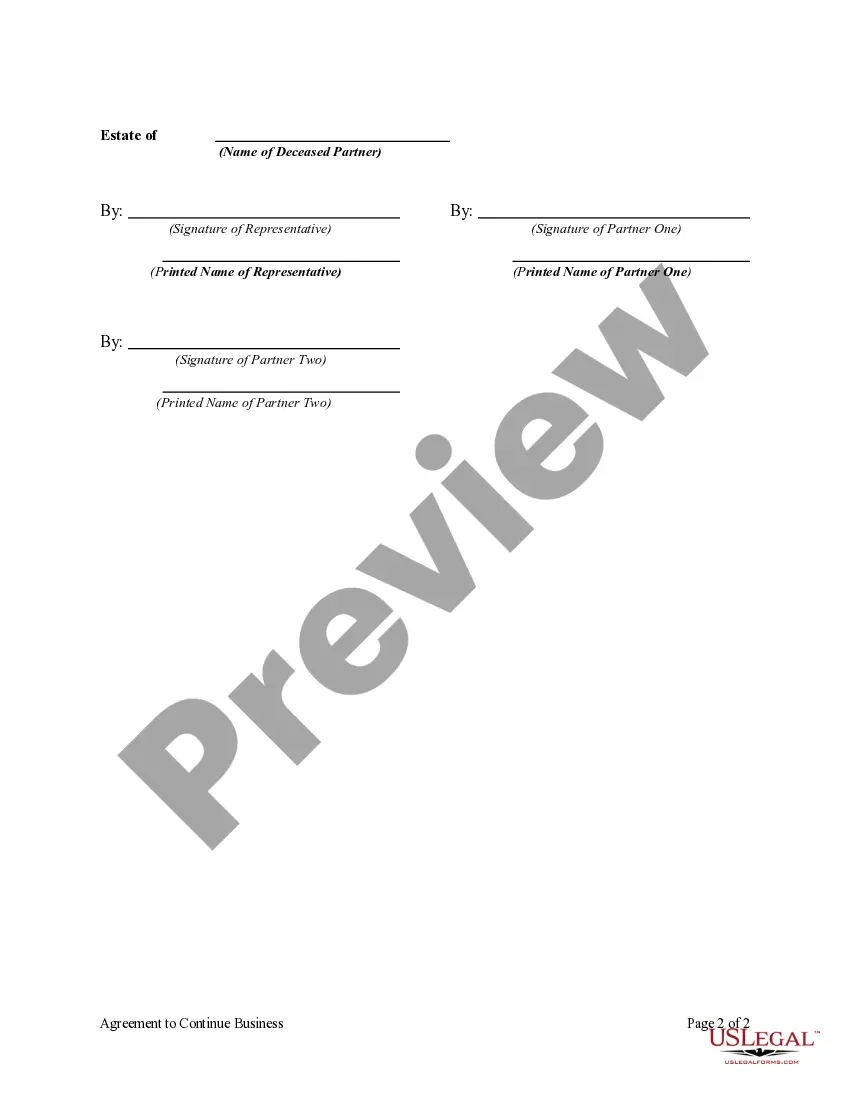

Florida Agreement to Continue Business Between Surviving Partners and Legal Representative of Deceased Partner is a legal document that outlines the terms and conditions for the continuation of a business relationship after the unfortunate demise of a partner. This agreement is crucial for ensuring smooth operations and preserving the partnership's value. It is designed to protect the interests of both the surviving partners and the legal representative of the deceased partner. Keywords: Florida Agreement to Continue Business, Surviving Partners, Legal Representative, Deceased Partner, Partnership, Terms and Conditions, Smooth Operations, Protect Interests, Preserving Value. There are two main types of Florida Agreement to Continue Business Between Surviving Partners and Legal Representative of Deceased Partner. 1. General Partnership Agreement: This type of agreement is used when the business is structured as a general partnership, where each partner has equal responsibilities and shares both profits and liabilities equally. When one partner passes away, the surviving partners must come to an agreement with the legal representative of the deceased partner to continue operating the business. 2. Limited Partnership Agreement: In a limited partnership, there are two types of partners — general partners, who manage the business and have unlimited liability, and limited partners, who contribute capital but have no involvement in the management. When a limited partner dies, the surviving general partners must reach an agreement with the legal representative to continue the business. Both types of agreements ensure that the surviving partners and the legal representative of the deceased partner have a clear understanding of their roles, responsibilities, and rights in the continued operation of the business. The agreement covers various aspects such as the distribution of profits and losses, decision-making authority, financial contributions, buyout provisions, and dispute resolution mechanisms. By formalizing the continuation of the business and clarifying the rights and obligations of the involved parties, the Florida Agreement to Continue Business Between Surviving Partners and Legal Representative of Deceased Partner offers peace of mind and legal protection to all parties involved. It serves as a vital tool for maintaining the stability and sustainability of the partnership, while safeguarding the interests of both the surviving partners and the legal representative of the deceased partner. In conclusion, the Florida Agreement to Continue Business Between Surviving Partners and Legal Representative of Deceased Partner is a crucial legal document that sets out the terms and conditions for the continuation of a business after the death of a partner. It ensures the smooth operation of the partnership and protects the interests of both the surviving partners and the legal representative.

Florida Agreement to Continue Business Between Surviving Partners and Legal Representative of Deceased Partner

Description

How to fill out Florida Agreement To Continue Business Between Surviving Partners And Legal Representative Of Deceased Partner?

Discovering the right legitimate papers template can be a struggle. Of course, there are plenty of templates available online, but how do you obtain the legitimate develop you require? Take advantage of the US Legal Forms website. The services provides thousands of templates, such as the Florida Agreement to Continue Business Between Surviving Partners and Legal Representative of Deceased Partner, which can be used for business and personal needs. Every one of the varieties are examined by experts and meet up with state and federal demands.

When you are currently listed, log in in your accounts and then click the Down load option to find the Florida Agreement to Continue Business Between Surviving Partners and Legal Representative of Deceased Partner. Utilize your accounts to look with the legitimate varieties you may have ordered earlier. Visit the My Forms tab of your own accounts and obtain an additional version in the papers you require.

When you are a new user of US Legal Forms, allow me to share easy recommendations that you should stick to:

- First, make certain you have chosen the proper develop for your personal city/area. You may look through the shape while using Preview option and browse the shape outline to guarantee it is the best for you.

- In the event the develop does not meet up with your requirements, take advantage of the Seach industry to find the correct develop.

- Once you are positive that the shape is suitable, click on the Get now option to find the develop.

- Opt for the pricing plan you desire and enter the necessary information and facts. Build your accounts and buy your order with your PayPal accounts or credit card.

- Select the data file file format and down load the legitimate papers template in your product.

- Full, change and print and indicator the acquired Florida Agreement to Continue Business Between Surviving Partners and Legal Representative of Deceased Partner.

US Legal Forms is the greatest local library of legitimate varieties where you can find various papers templates. Take advantage of the service to down load expertly-manufactured paperwork that stick to condition demands.