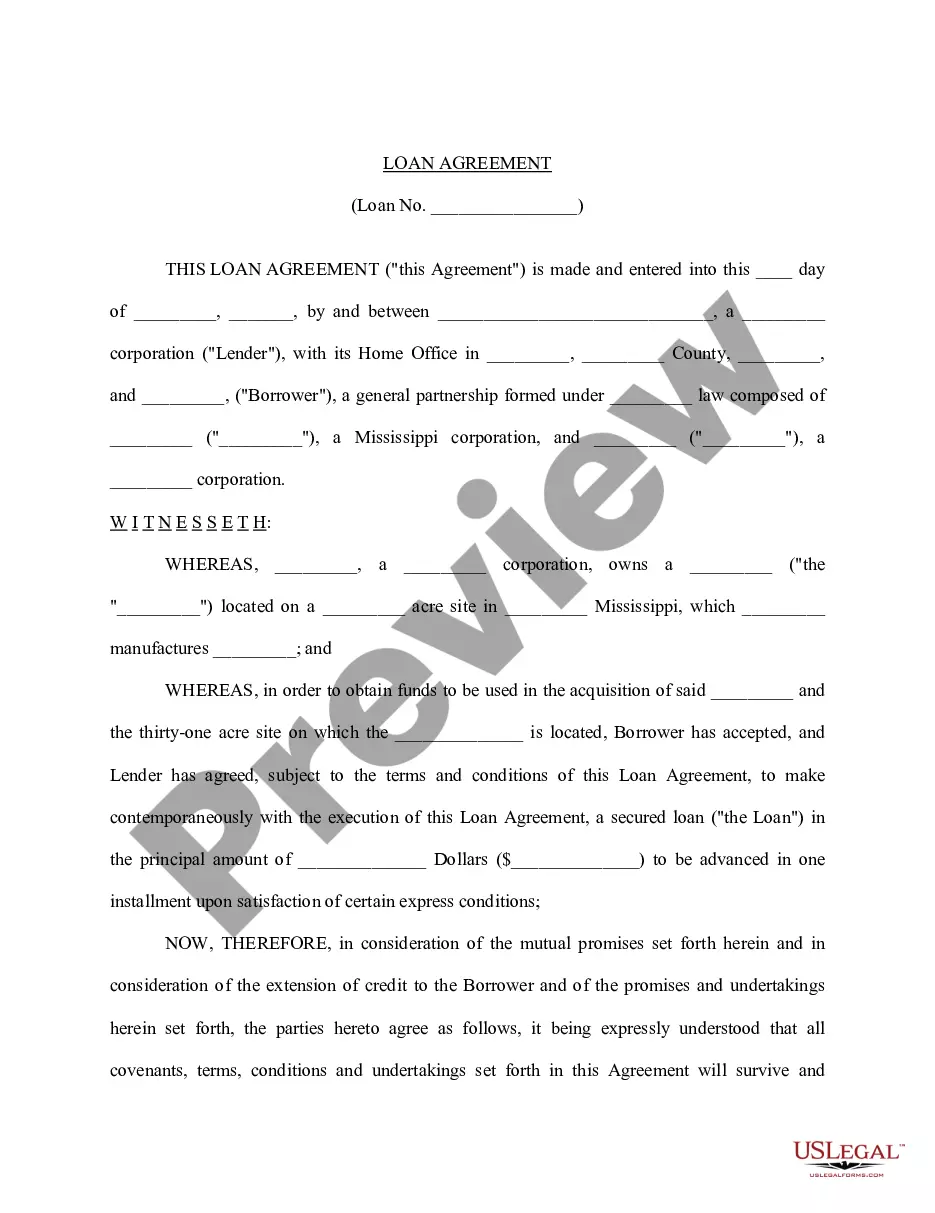

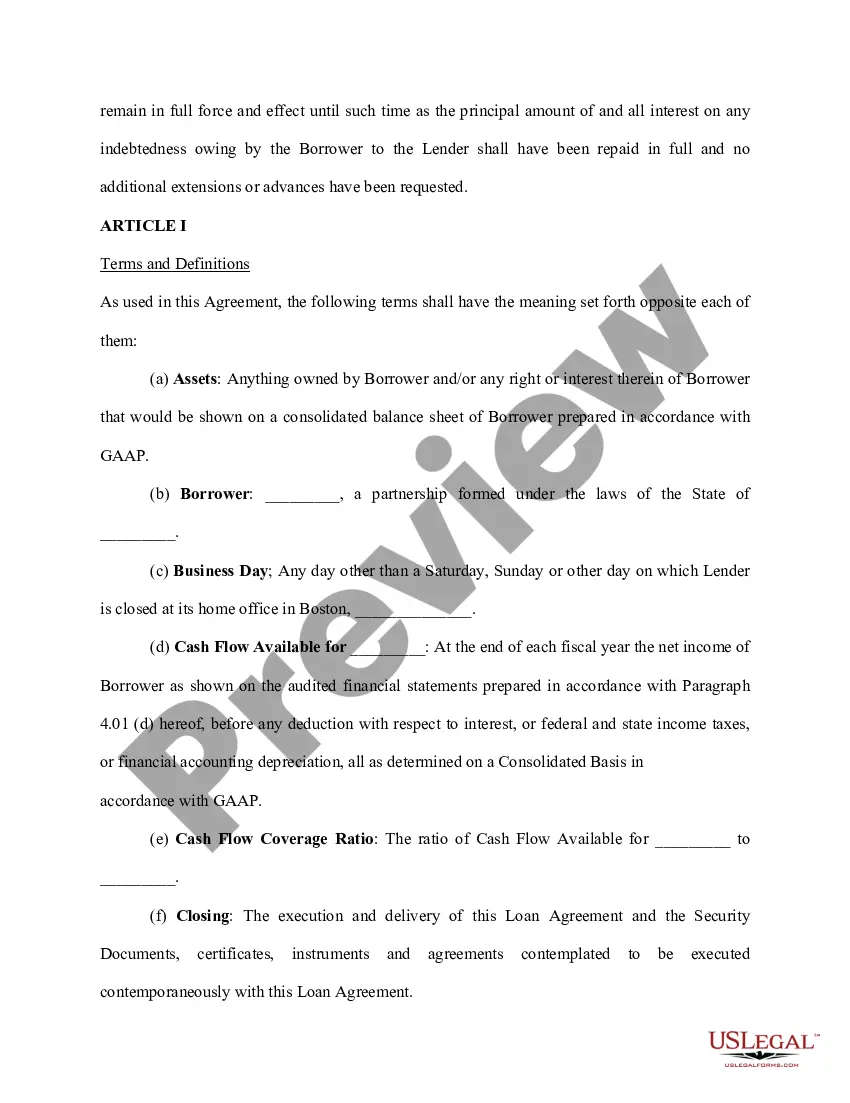

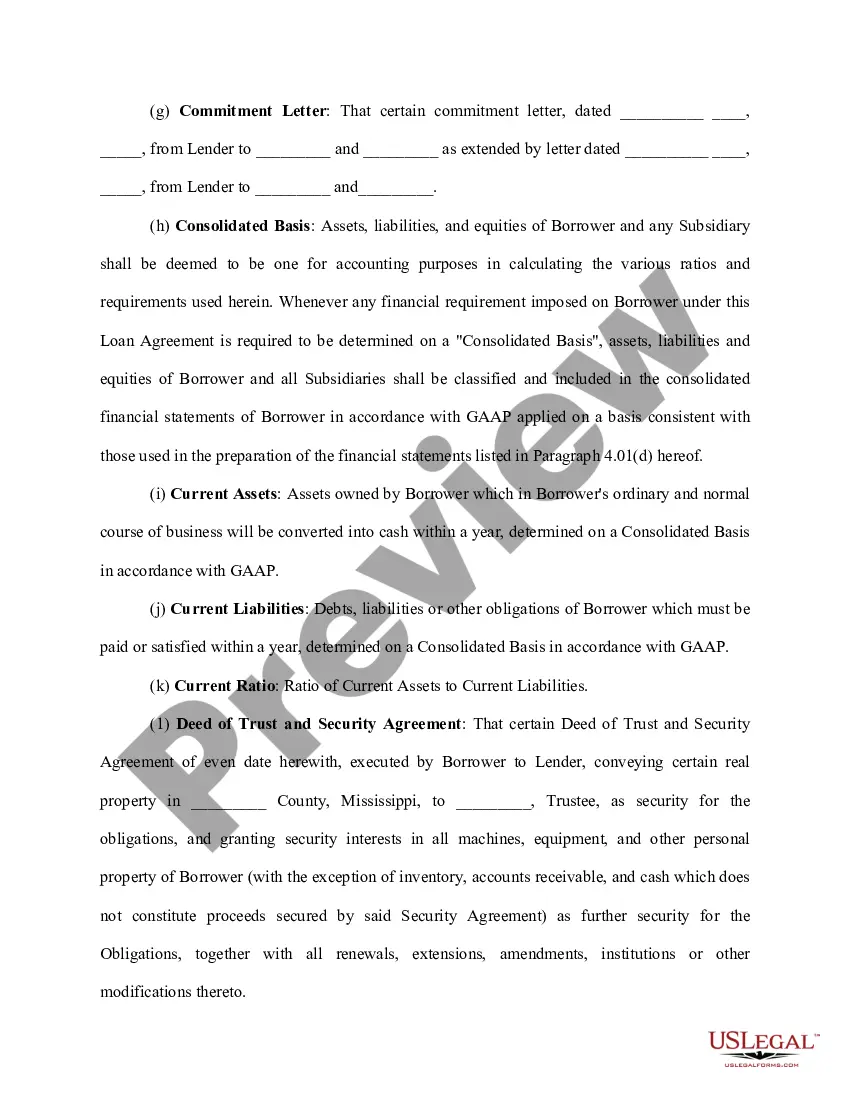

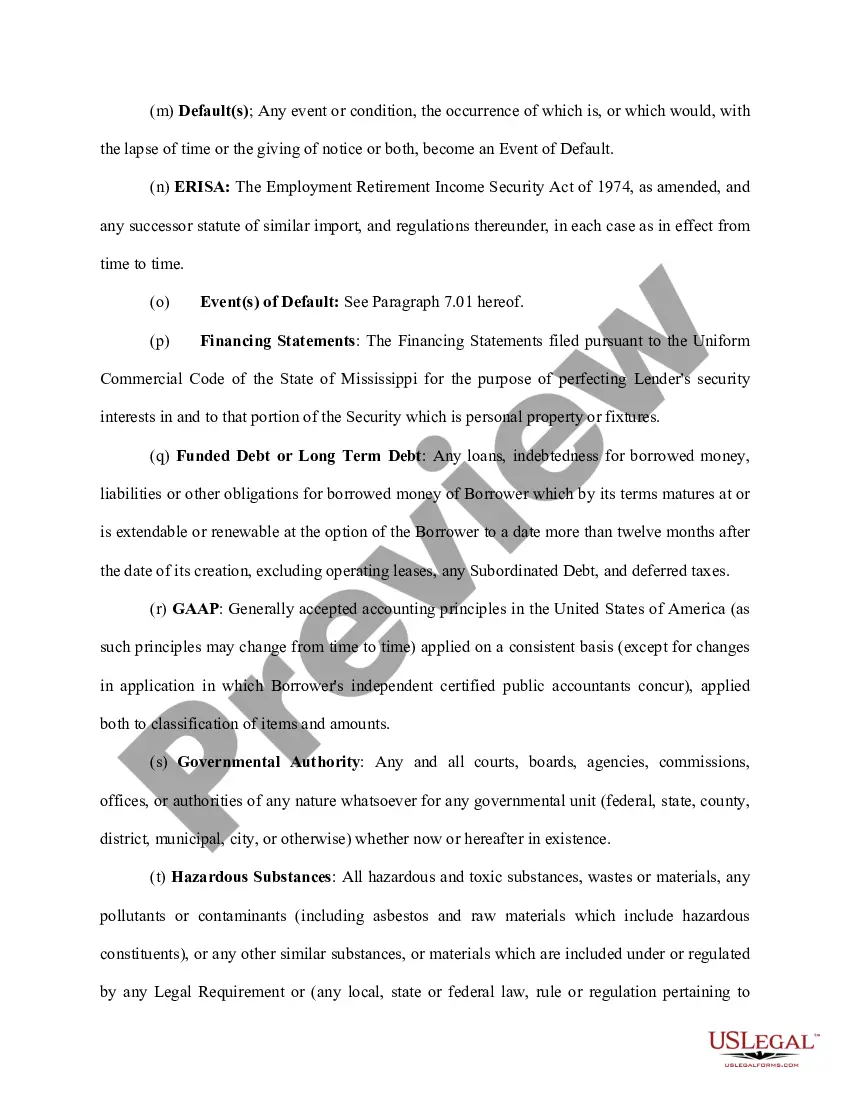

Florida Loan Agreement for Family Member is a legally binding contract that outlines the terms and conditions under which a family member loans money to another family member within the state of Florida. This agreement ensures that both parties involved are protected and aware of their rights and obligations during the loan transaction, avoiding any potential misunderstandings or disputes in the future. The main purpose of a Florida Loan Agreement for Family Member is to clearly define the loan amount being provided, the repayment terms, and any additional terms and conditions that both parties agree to. This agreement specifies important details such as the interest rate (if applicable), repayment schedule, and consequences in case of default or nonpayment. There are different types of Florida Loan Agreements for Family Members, depending on the specific circumstances and intentions of the involved parties. Here are a few types commonly used: 1. Simple Loan Agreement: This type of agreement is suitable for straightforward loans between family members, where the loan amount and repayment terms are clearly defined. It may include provisions for interest, collateral, and repayment schedule. 2. Demand Loan Agreement: This type of agreement allows the lender to request repayment of the loan at any time, without specifying a fixed repayment schedule. It provides flexibility for both parties but requires open communication and trust. 3. Installment Loan Agreement: In this type of agreement, the loan amount is divided into equal installments that the borrower repays periodically over a specified period. It provides a structured repayment schedule and may include interest charges. 4. Promissory Note: A promissory note is an essential part of any loan agreement, including Florida Loan Agreements for Family Members. It is a written promise by the borrower to repay the loan under the agreed terms and conditions. To create a valid Florida Loan Agreement for Family Member, it is recommended to consult with a qualified legal professional who can provide guidance and ensure that all relevant state laws are followed. Both parties should fully understand the terms and conditions before signing the agreement, protecting their rights and maintaining a healthy family relationship throughout the loan transaction.

Florida Loan Agreement for Family Member

Description

How to fill out Florida Loan Agreement For Family Member?

If you have to full, acquire, or print legitimate papers layouts, use US Legal Forms, the biggest collection of legitimate varieties, which can be found online. Make use of the site`s simple and convenient research to obtain the documents you want. Various layouts for organization and individual functions are categorized by categories and states, or key phrases. Use US Legal Forms to obtain the Florida Loan Agreement for Family Member within a couple of mouse clicks.

When you are already a US Legal Forms client, log in in your accounts and then click the Acquire switch to obtain the Florida Loan Agreement for Family Member. Also you can accessibility varieties you previously delivered electronically within the My Forms tab of your accounts.

If you use US Legal Forms initially, refer to the instructions listed below:

- Step 1. Be sure you have chosen the shape to the correct town/region.

- Step 2. Utilize the Review solution to check out the form`s content. Do not forget to see the description.

- Step 3. When you are unhappy using the kind, take advantage of the Look for industry near the top of the monitor to get other versions of the legitimate kind template.

- Step 4. Upon having located the shape you want, go through the Purchase now switch. Choose the prices prepare you prefer and add your accreditations to sign up for the accounts.

- Step 5. Procedure the transaction. You may use your charge card or PayPal accounts to finish the transaction.

- Step 6. Find the structure of the legitimate kind and acquire it on the system.

- Step 7. Total, edit and print or sign the Florida Loan Agreement for Family Member.

Each and every legitimate papers template you get is the one you have eternally. You possess acces to every kind you delivered electronically with your acccount. Go through the My Forms portion and choose a kind to print or acquire once more.

Be competitive and acquire, and print the Florida Loan Agreement for Family Member with US Legal Forms. There are many specialist and condition-specific varieties you can use for the organization or individual requires.