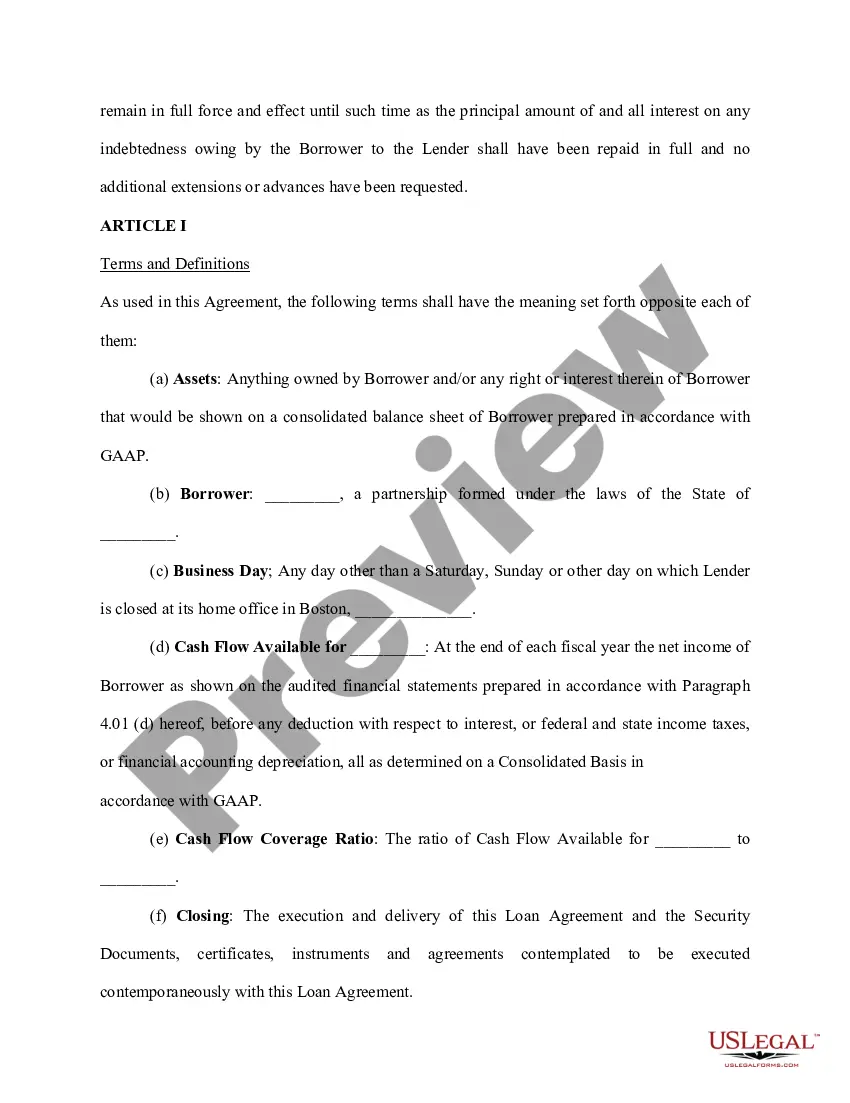

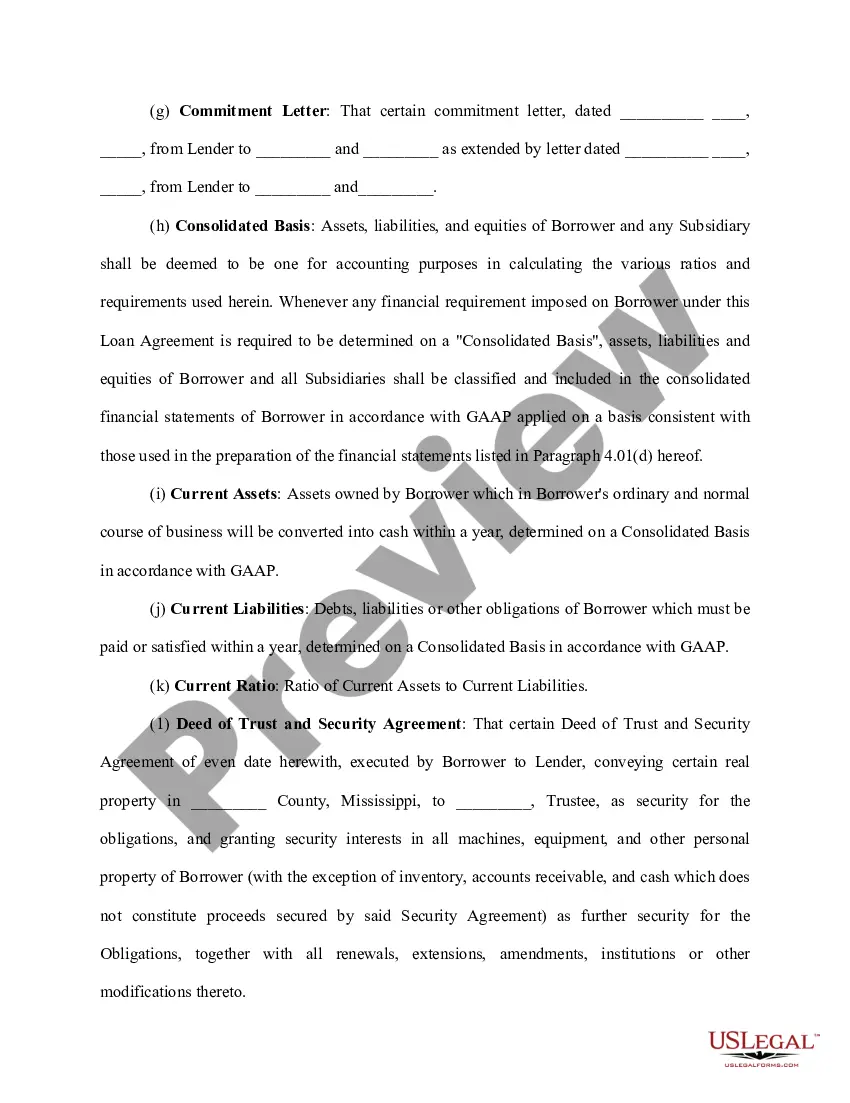

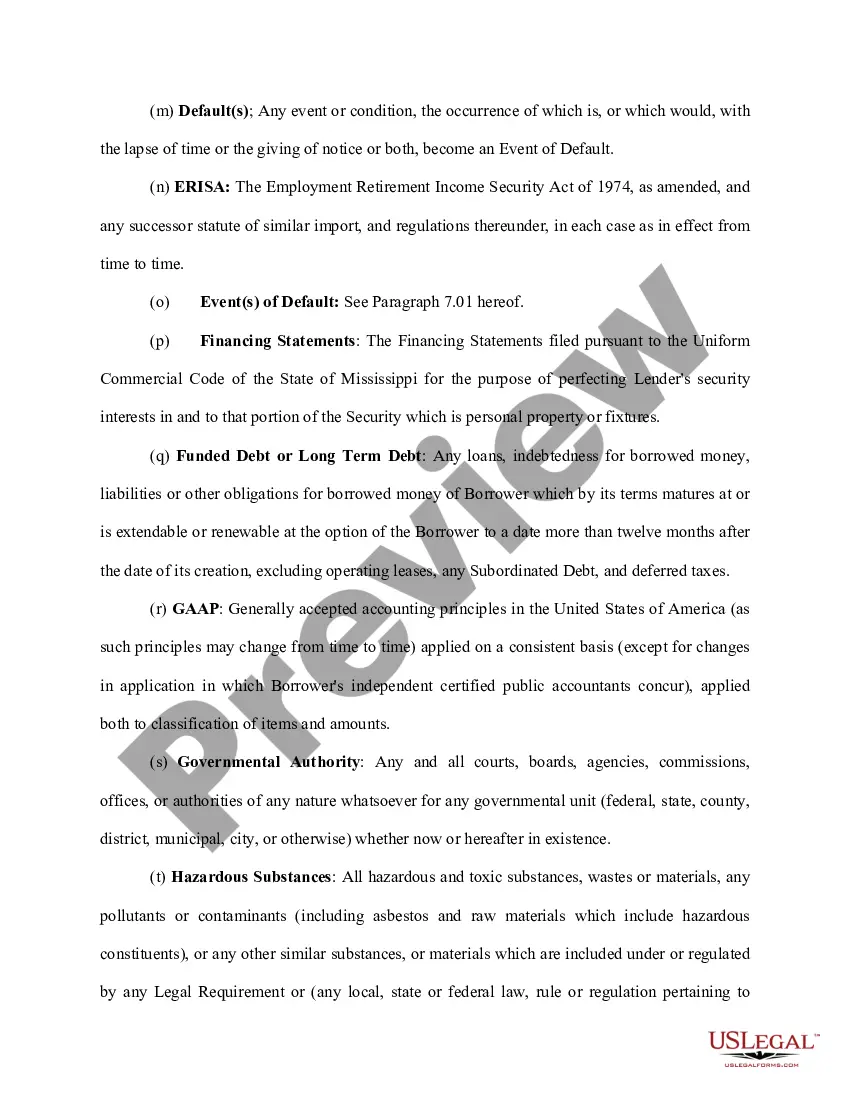

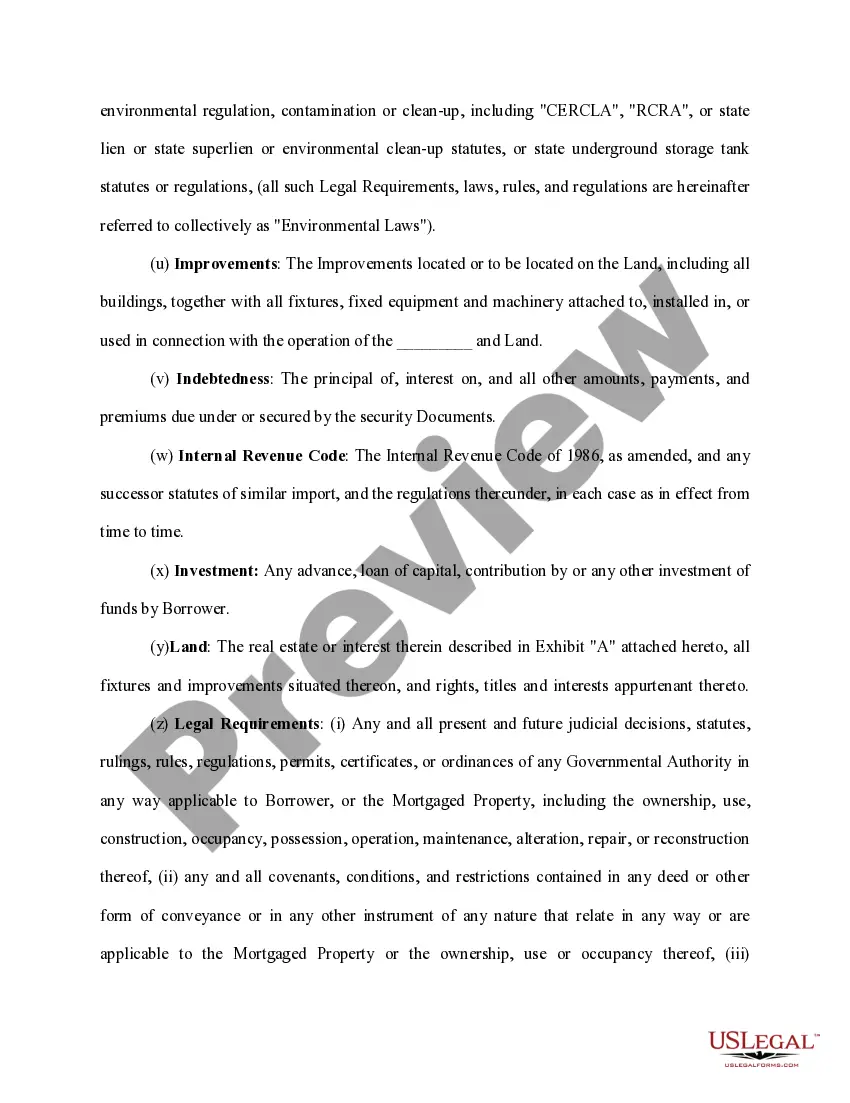

A Florida Loan Agreement is a legal contract entered into between a lender and a borrower that outlines the terms and conditions of a loan. It serves as a tool to ensure both parties understand their rights and obligations regarding the borrowed funds. In the state of Florida, there are various types of loan agreements tailored to specific borrowing needs, such as: 1. Personal Loan Agreement: This type of loan agreement is used when an individual borrower seeks to obtain funds for personal reasons, such as debt consolidation, home improvement, or purchasing a vehicle. 2. Business Loan Agreement: Small businesses or entrepreneurs often require financial assistance, and a business loan agreement is used to establish the terms of the loan with the lender. It typically addresses aspects such as loan purpose, repayment terms, interest rate, and collateral (if any). 3. Mortgage Loan Agreement: When purchasing real estate, individuals often rely on mortgage loans. A mortgage loan agreement in Florida defines the terms and conditions for the loan, including the loan amount, interest rate, repayment schedule, and property specifics. 4. Student Loan Agreement: Educational expenses often require financial aid, and a student loan agreement specifically caters to this need. It outlines the terms of the loan, including repayment commencement, interest rate, grace period, and the responsibilities of both the student borrower and the lending institution. 5. Auto Loan Agreement: Florida residents may require financing for automobile purchases, and an auto loan agreement facilitates this. It covers the details of the loan, such as the loan amount, repayment structure, interest rate, and information about the vehicle being financed. Regardless of the type of loan agreement, it is vital to include key provisions to protect both the lender and the borrower. These provisions may include loan repayment terms, late payment fees, default consequences, dispute resolution mechanisms, and any specific state-mandated disclosures that may pertain to the loan transaction. In conclusion, a Florida Loan Agreement is a legally binding contract that establishes the terms of a loan between a lender and a borrower. These agreements can encompass various types of loans, such as personal loans, business loans, mortgage loans, student loans, and auto loans. Understanding and adhering to the terms outlined in the loan agreement is crucial for both parties involved.

Florida Loan Agreement

Description

How to fill out Florida Loan Agreement?

Are you presently in the place where you need to have papers for possibly enterprise or specific purposes virtually every working day? There are plenty of legal document layouts accessible on the Internet, but locating ones you can rely on is not simple. US Legal Forms provides a large number of form layouts, much like the Florida Loan Agreement, which can be composed to satisfy state and federal demands.

Should you be currently familiar with US Legal Forms internet site and possess your account, just log in. Afterward, you may acquire the Florida Loan Agreement design.

Unless you provide an profile and need to begin using US Legal Forms, follow these steps:

- Find the form you require and ensure it is to the right town/county.

- Take advantage of the Preview key to check the shape.

- Read the explanation to actually have selected the proper form.

- When the form is not what you are seeking, take advantage of the Search area to get the form that meets your requirements and demands.

- If you discover the right form, click on Get now.

- Select the rates program you desire, fill out the necessary information and facts to make your money, and purchase your order making use of your PayPal or charge card.

- Decide on a handy data file structure and acquire your duplicate.

Get every one of the document layouts you have bought in the My Forms food list. You can get a further duplicate of Florida Loan Agreement at any time, if possible. Just select the required form to acquire or printing the document design.

Use US Legal Forms, by far the most comprehensive assortment of legal types, to conserve efforts and prevent mistakes. The support provides skillfully created legal document layouts that can be used for a variety of purposes. Generate your account on US Legal Forms and initiate creating your daily life easier.