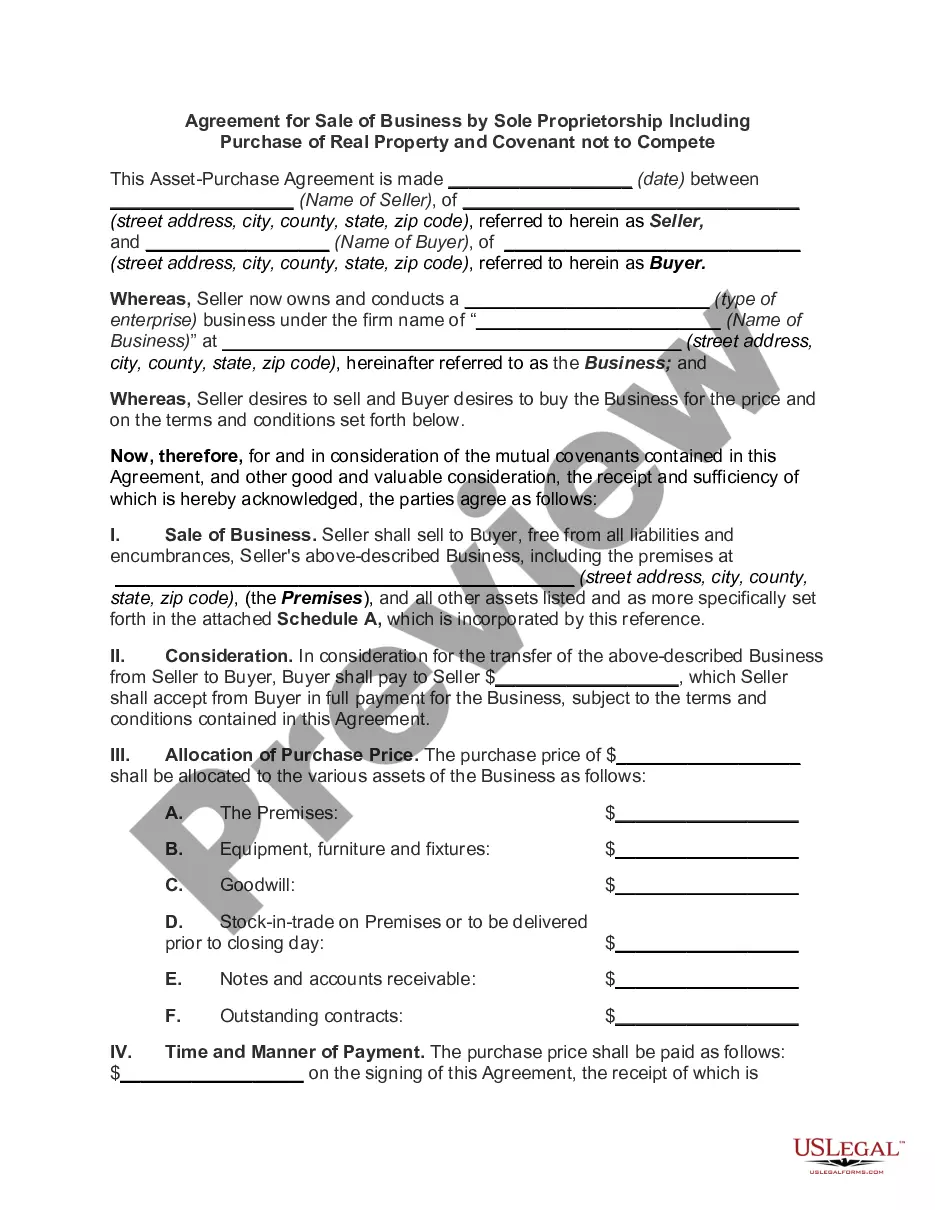

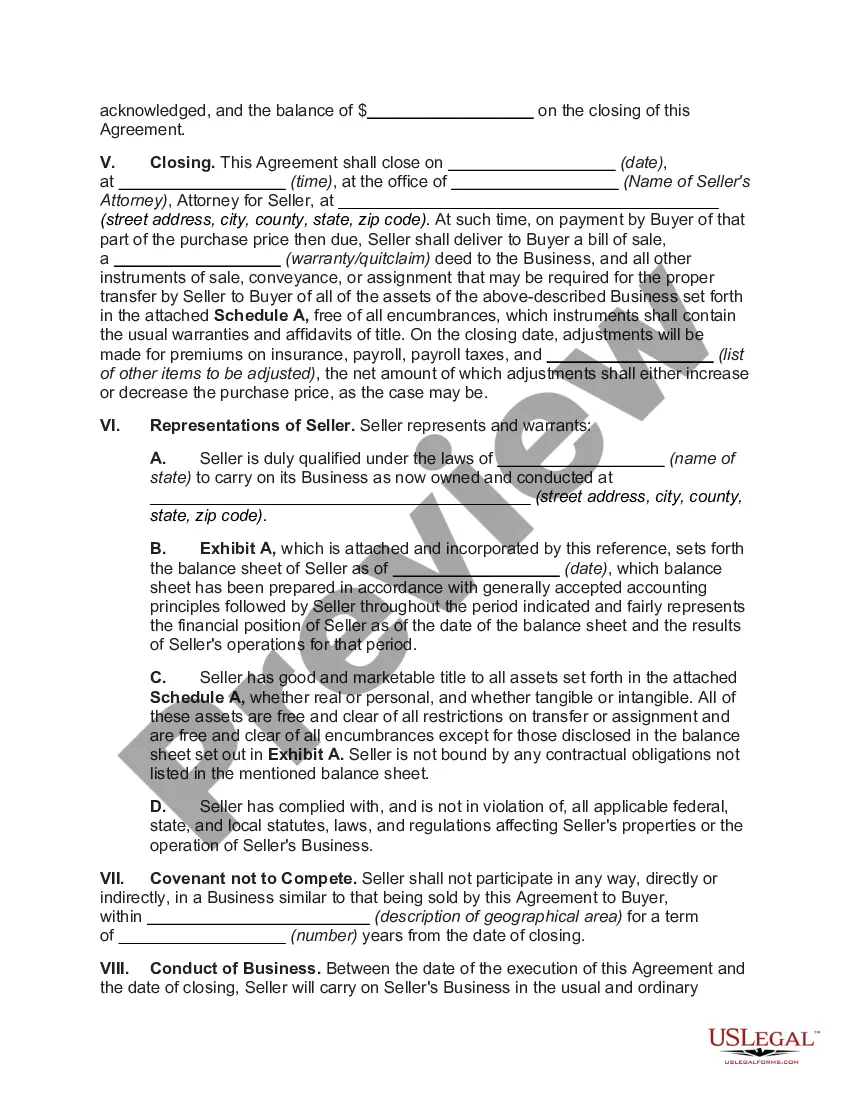

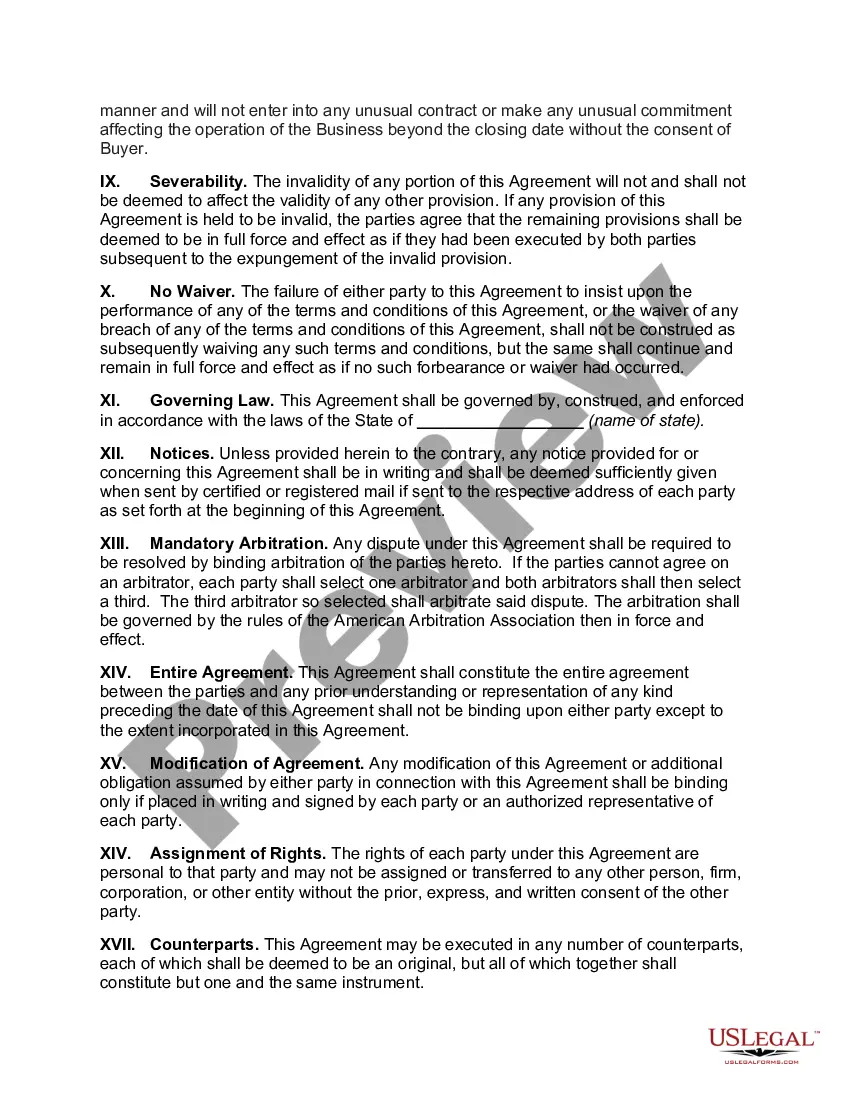

The Florida Agreement for Sale of Business by Sole Proprietorship is a legal document that outlines the terms and conditions between a sole proprietor selling their business and a buyer interested in purchasing the business, including any associated real property. This agreement is crucial in ensuring a smooth and fair transaction. Key elements that should be included in the Florida Agreement for Sale of Business by Sole Proprietorship, including Purchase of Real Property, are: 1. Parties involved: Clearly state the names and contact information of both the seller (sole proprietor) and the buyer. Also, mention any additional parties involved, such as brokers or attorneys. 2. Business details: Provide a detailed description of the business being sold, including its legal name, physical location, assets, inventory, intellectual property rights (if applicable), and any licenses or permits required for its operations. 3. Real property details: If the sale includes the purchase of real property, describe the property's location, dimensions, zoning information, any attached fixtures or improvements, and any licenses or permits associated with the property. 4. Purchase price and terms: Specify the agreed-upon purchase price for the business and any associated real property. Outline how the payment will be made, whether in a lump sum or installments, and the date by which it must be completed. Include any contingencies related to financing or appraisal. 5. Asset allocation: Determine how the purchase price will be allocated among the business assets, such as equipment, inventory, goodwill, and real estate. It may be necessary to consult with a tax advisor to ensure proper allocation for tax purposes. 6. Due diligence: Allow a period for the buyer to conduct due diligence on the business, including reviewing financial statements, tax returns, legal documents, contracts, and any other relevant records. Specify the duration and scope of the due diligence process. 7. Representations and warranties: Both parties should make specific representations and warranties about the accuracy of the information provided, the legal compliance of the business, the absence of undisclosed liabilities, and any necessary authorizations or consents required for the sale. 8. Closing procedures: Clearly outline the steps to be followed during the closing process, including the transfer of ownership, delivery of necessary documents, and any required governmental approvals or notifications. Additional types of Florida Agreement for Sale of Business by Sole Proprietorship, including Purchase of Real Property, may exist based on specific business or transaction requirements. These variations could include agreements related to specific industries (e.g., restaurants, retail stores, or professional services) or agreements tailored for different sizes or complexities of businesses. It is important to consult with a qualified attorney or legal professional to ensure the specific agreement is appropriately customized and compliant with Florida state laws.

Florida Agreement for Sale of Business by Sole Proprietorship including Purchase of Real Property

Description

How to fill out Florida Agreement For Sale Of Business By Sole Proprietorship Including Purchase Of Real Property?

Finding the right legitimate file design might be a battle. Needless to say, there are a variety of layouts available online, but how will you obtain the legitimate kind you want? Make use of the US Legal Forms internet site. The services offers a huge number of layouts, such as the Florida Agreement for Sale of Business by Sole Proprietorship including Purchase of Real Property, which can be used for enterprise and personal requirements. Every one of the varieties are examined by pros and meet federal and state needs.

When you are already listed, log in in your account and click the Obtain option to get the Florida Agreement for Sale of Business by Sole Proprietorship including Purchase of Real Property. Use your account to appear with the legitimate varieties you possess acquired formerly. Go to the My Forms tab of your own account and obtain another copy from the file you want.

When you are a brand new end user of US Legal Forms, here are basic recommendations so that you can adhere to:

- Very first, be sure you have selected the right kind for your personal area/area. You may look over the shape while using Review option and read the shape description to guarantee it will be the right one for you.

- If the kind does not meet your preferences, use the Seach area to obtain the right kind.

- Once you are certain that the shape is proper, click the Acquire now option to get the kind.

- Choose the pricing strategy you desire and enter the necessary details. Design your account and buy an order making use of your PayPal account or charge card.

- Opt for the submit structure and acquire the legitimate file design in your product.

- Complete, change and print and sign the obtained Florida Agreement for Sale of Business by Sole Proprietorship including Purchase of Real Property.

US Legal Forms is the biggest collection of legitimate varieties that you can see numerous file layouts. Make use of the company to acquire appropriately-created documents that adhere to status needs.