Florida Installment Promissory Note and Security Agreement

Description

How to fill out Installment Promissory Note And Security Agreement?

Selecting the most suitable authorized document template can be a challenge. Of course, there are numerous templates accessible online, but how can you find the legal document you need? Utilize the US Legal Forms website. The service offers thousands of templates, including the Florida Installment Promissory Note and Security Agreement, that can be used for business and personal purposes. All forms are reviewed by experts and comply with federal and state requirements.

If you are already registered, Log In to your account and click the Download button to obtain the Florida Installment Promissory Note and Security Agreement. Use your account to browse through the legal forms you have purchased previously. Go to the My documents tab in your account to download another copy of the document you need.

If you are a new user of US Legal Forms, here are simple steps you can follow: First, make sure you have selected the correct form for your city/region. You can view the form using the Preview button and read the form description to ensure it is suitable for you. If the form does not meet your expectations, use the Search field to find the appropriate form. When you are sure that the form is suitable, click the Purchase now button to acquire the form. Choose the pricing plan you prefer and enter the required information. Create your account and complete the transaction using your PayPal account or credit card. Select the file format and download the legal document template to your device. Fill out, edit, print, and sign the downloaded Florida Installment Promissory Note and Security Agreement.

US Legal Forms is the largest collection of legal forms where you can find a variety of document templates. Take advantage of the service to obtain professionally crafted documents that meet state requirements.

- Utilize the US Legal Forms website for a wide selection of templates.

- All documents are reviewed for compliance with legal standards.

- Log in to access previously purchased documents easily.

- Follow simple steps to find and download the right form.

- Choose from various pricing options to suit your needs.

- Complete the form and keep it for your records.

Form popularity

FAQ

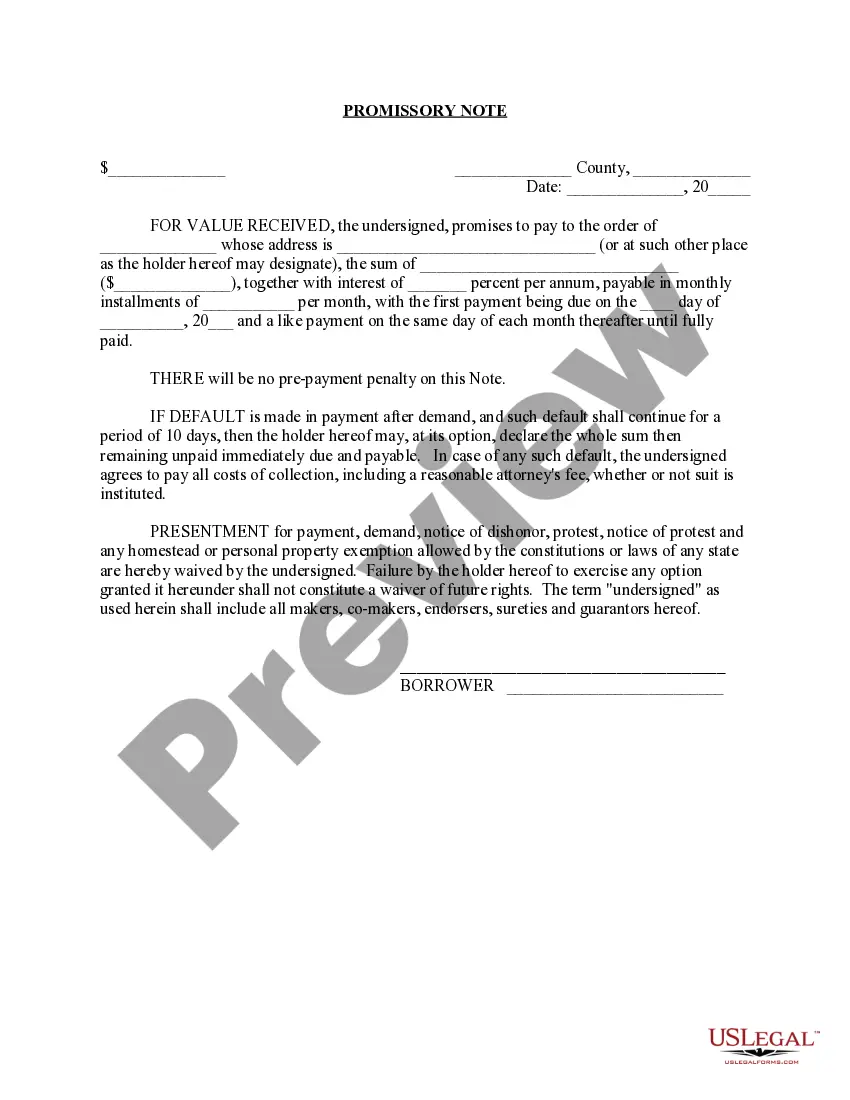

A promissory note must include the date of the loan, the dollar amount, the names of both parties, the rate of interest, any collateral involved, and the timeline for repayment. When this document is signed by the borrower, it becomes a legally binding contract.

Florida Promissory Note RequirementsNames and contact information of all parties to the agreement;A statement of the promise to pay;Amount of the loan;Collateral used to secure the loan, if any;Repayment schedule (amounts, frequency) and interest;Date repayment is due;Penalties and late fees;More items...?

In general, under the federal Securities Acts, promissory notes are defined as securities, but notes with a maturity of 9 months or less are not securities.

General Definition. Promissory notes are defined as securities under the Securities Act. However, notes that have a maturity of nine months or less are not considered securities.

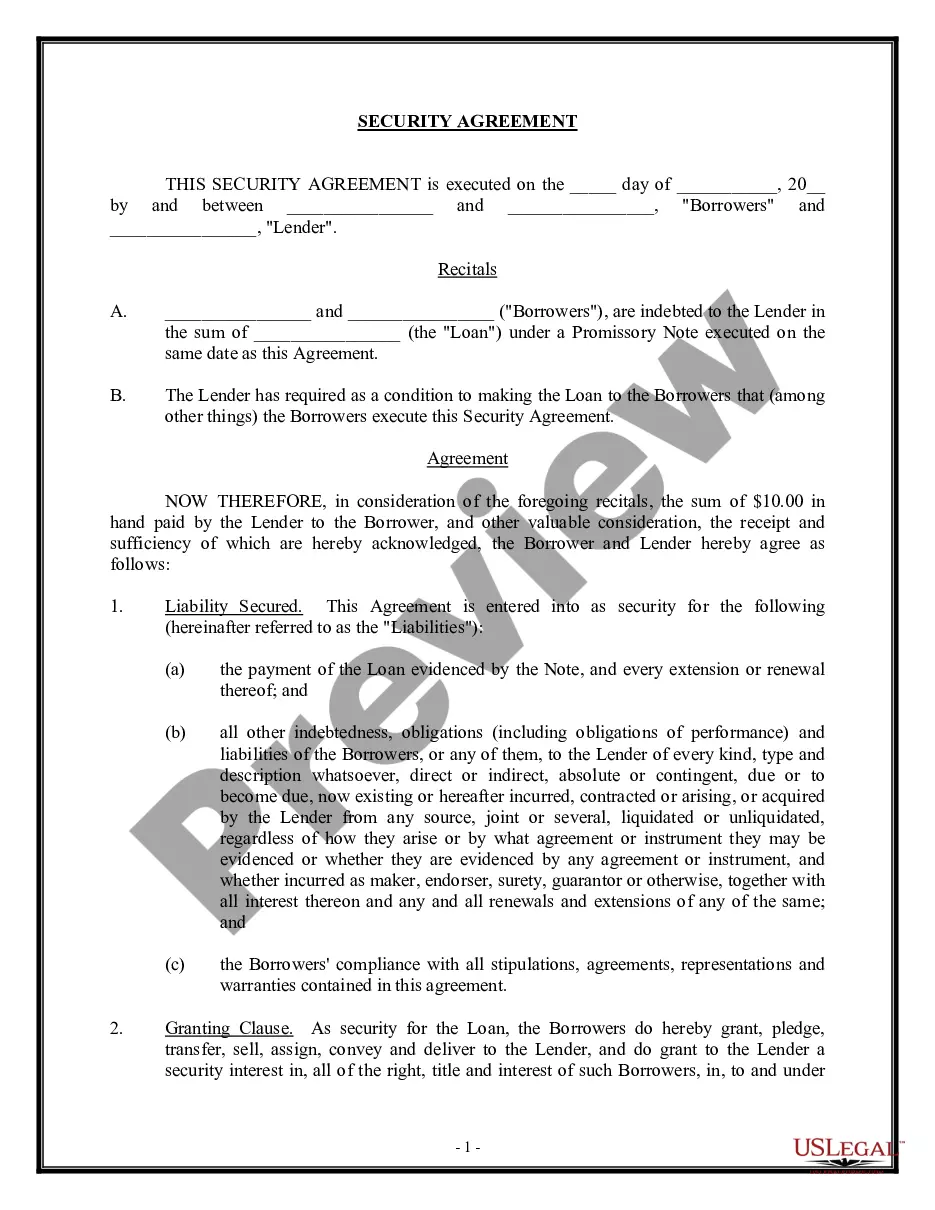

A security interest arising out of a sale of a promissory note (i.e., an instrument) is perfected automatically, without additional action, when it attaches. See Section 9-304(4) of the Uniform Commercial Code.

A promissory note secured by collateral will need a second document. If the collateral is real property, there will be either a mortgage or a deed of trust. If the collateral is personal property, there will be a security agreement.

A Promissory Note may be secured or unsecured. In case of a secured note, the borrower will be required to provide a collateral such as property, goods, services, etc., in the event that they fail to repay the borrowed amount.

A Florida promissory note can be either secured or unsecured. A secured promissory note is one that is backed by collateral (e.g., real estate, a business interest, intellectual property, or some other personal property held by the borrower). An unsecured promissory note has no collateral.

A secured promissory note may include a security agreement as part of its terms. If a security agreement lists a business property as collateral, the lender might file a UCC-1 statement to serve as a lien on the property. A security agreement mitigates the default risk faced by the lender.