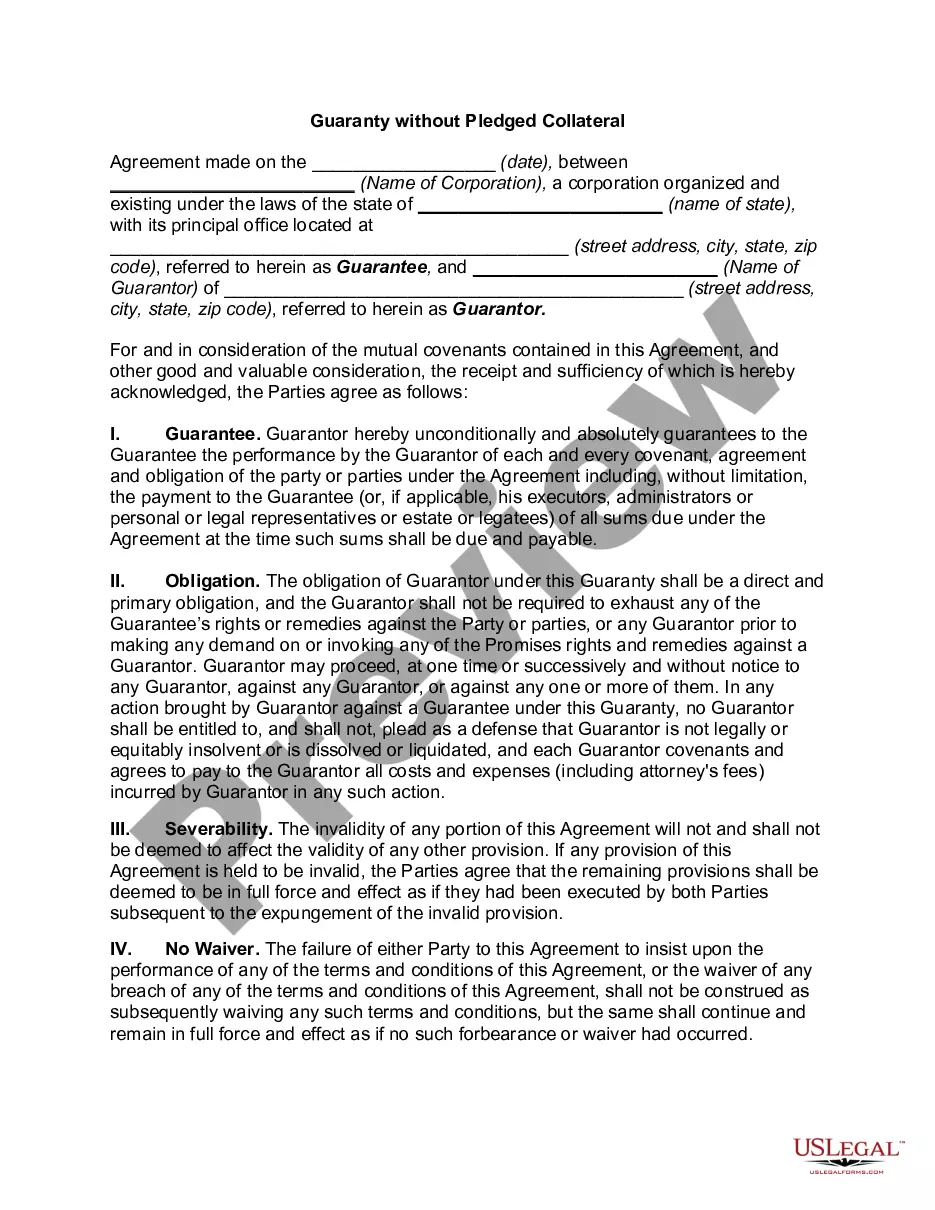

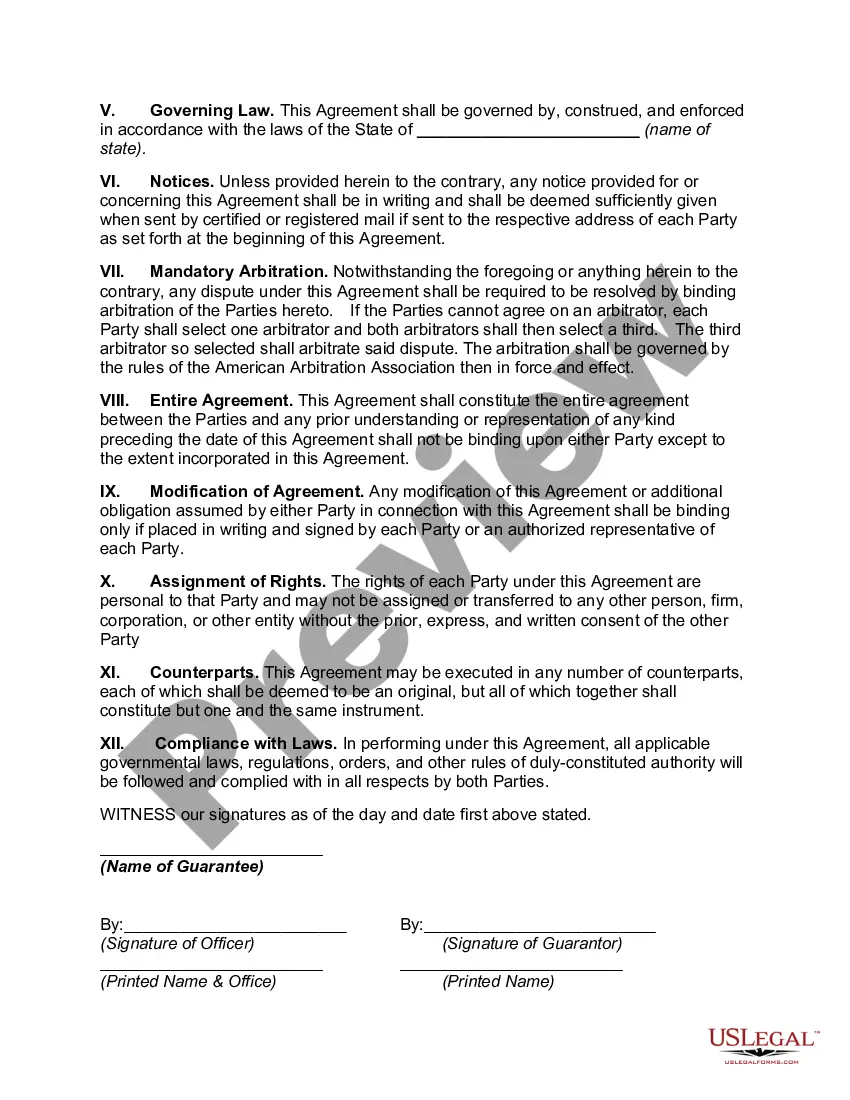

Florida Guaranty without Pledged Collateral is a legal provision that provides an enforceable pledge to repay a debt even without the presence of any collateral. A guaranty is a promise made by an individual or entity, known as the guarantor, to be responsible for the obligations of another party, known as the debtor. In Florida, this type of guaranty can be used to secure various types of loans, credit facilities, and financial transactions. When considering Florida Guaranty without Pledged Collateral, it is essential to be aware of its different types and variations. Here are some notable examples: 1. General Guaranty: This is the most common type of guaranty without pledged collateral. It involves a guarantor providing a promise to repay a debt if the primary debtor fails to do so. It applies to a broad range of financial obligations, such as commercial loans, lines of credit, leases, or bonds. 2. Limited Guaranty: A limited guaranty is a variation that covers only a portion or specific aspects of the debtor's obligations. For instance, the guarantor may agree to cover unpaid rent or a specific percentage of the loan amount. This type of guaranty allows the guarantor to limit their liability to a defined extent. 3. Continuing Guaranty: A continuing guaranty is one that remains in force until specifically revoked or terminated. Unlike a limited guaranty, which has a predefined end date or condition, a continuing guaranty persists until a formal notice of termination is provided by either party. It provides ongoing protection to the creditor for a range of future or unforeseen obligations. 4. Subsidiary Guaranty: In certain cases, a subsidiary company may provide a guaranty for the obligations of its parent company. This type of guaranty without pledged collateral ensures that the subsidiary will repay the debt if the parent company fails to meet its financial obligations. It can be essential for lenders when dealing with complex corporate structures or joint ventures. 5. Demand Guaranty: A demand guaranty grants the lender the right to demand repayment from the guarantor immediately upon the debtor's default. With this type, the lender does not need to wait for a predetermined event or timeline to pass before enforcing the guarantor's obligation. It offers a higher level of security to the creditor, particularly in situations where timely repayment is crucial. In conclusion, Florida Guaranty without Pledged Collateral refers to the legal provision that allows a party to secure a debt or obligation without the need for collateral. Being aware of the various types of guaranties, such as general guaranty, limited guaranty, continuing guaranty, subsidiary guaranty, and demand guaranty, is essential for individuals and businesses involved in financial transactions in the state of Florida.

Florida Guaranty without Pledged Collateral

Description

How to fill out Florida Guaranty Without Pledged Collateral?

If you have to total, down load, or produce legitimate record themes, use US Legal Forms, the greatest selection of legitimate forms, which can be found on the web. Utilize the site`s easy and handy research to obtain the papers you require. Various themes for business and personal reasons are categorized by categories and claims, or keywords. Use US Legal Forms to obtain the Florida Guaranty without Pledged Collateral within a number of clicks.

If you are currently a US Legal Forms buyer, log in to your account and click on the Obtain option to find the Florida Guaranty without Pledged Collateral. You may also accessibility forms you in the past delivered electronically in the My Forms tab of the account.

If you are using US Legal Forms for the first time, follow the instructions under:

- Step 1. Be sure you have chosen the form for that appropriate city/country.

- Step 2. Make use of the Preview method to look through the form`s content. Don`t forget to learn the outline.

- Step 3. If you are not satisfied together with the form, make use of the Lookup industry at the top of the display screen to discover other types of your legitimate form format.

- Step 4. Once you have found the form you require, click the Get now option. Pick the costs plan you choose and add your credentials to register for an account.

- Step 5. Approach the purchase. You may use your bank card or PayPal account to finish the purchase.

- Step 6. Pick the formatting of your legitimate form and down load it on your system.

- Step 7. Total, revise and produce or indication the Florida Guaranty without Pledged Collateral.

Every legitimate record format you buy is the one you have forever. You possess acces to every form you delivered electronically with your acccount. Select the My Forms section and decide on a form to produce or down load once again.

Remain competitive and down load, and produce the Florida Guaranty without Pledged Collateral with US Legal Forms. There are millions of skilled and condition-distinct forms you can utilize for your business or personal requirements.

Form popularity

FAQ

A guarantee must be in writing (or evidenced in writing) and signed by the guarantor or a person authorised by the guarantor (section 4, Statute of Frauds 1677). Guarantees and indemnities are often executed as deeds to overcome any argument about whether good consideration has been given.

To be enforceable as a personal guaranty, the signatory must sign the guaranty in his or her personal capacity and not as the president or CEO of the company receiving the loan, which is its own legal entity, separate and apart from the people that run and operate it.

Non-recourse finance is a type of commercial lending that entitles the lender to repayment only from the profits of the project the loan is funding and not from any other assets of the borrower. Such loans are generally secured by collateral.

Non-Recourse Guarantee means any Guarantee by the Company or a Guarantor of Non-Recourse Debt incurred by an Excluded Project Subsidiary as to which the lenders of such Non-Recourse Debt have acknowledged that they will not have any recourse to the stock or assets of the Company or any Guarantor, except to the limited

A personal guarantee can be enforced the same way as any debt. If the business owner does not pay, the creditor can bring a lawsuit to receive a judgment and levy the owner's personal assets to cover the debt. The exact terms of a personal guarantee specify a creditor's options under the guarantee.

An unsecured loan is a loan that doesn't require any type of collateral. Instead of relying on a borrower's assets as security, lenders approve unsecured loans based on a borrower's creditworthiness. Examples of unsecured loans include personal loans, student loans, and credit cards.

There are two types of debts: recourse and nonrecourse. A recourse debt holds the borrower personally liable. All other debt is considered nonrecourse. In general, recourse debt (loans) allows lenders to collect what is owed for the debt even after they've taken collateral (home, credit cards).

An offer to guarantee must be accepted, either by express or implied acceptance. If a surety's assent to a guarantee has been procured by fraud by the person to whom it is given, there is no binding contract.

Florida law does not require a lender to elect to proceed separately against real and personal property. The lender may proceed in one action against both real and personal property collateral given for its loan.

Guarantee. 1) v. to pledge or agree to be responsible for another's debt or contractual performance if that other person does not pay or perform.