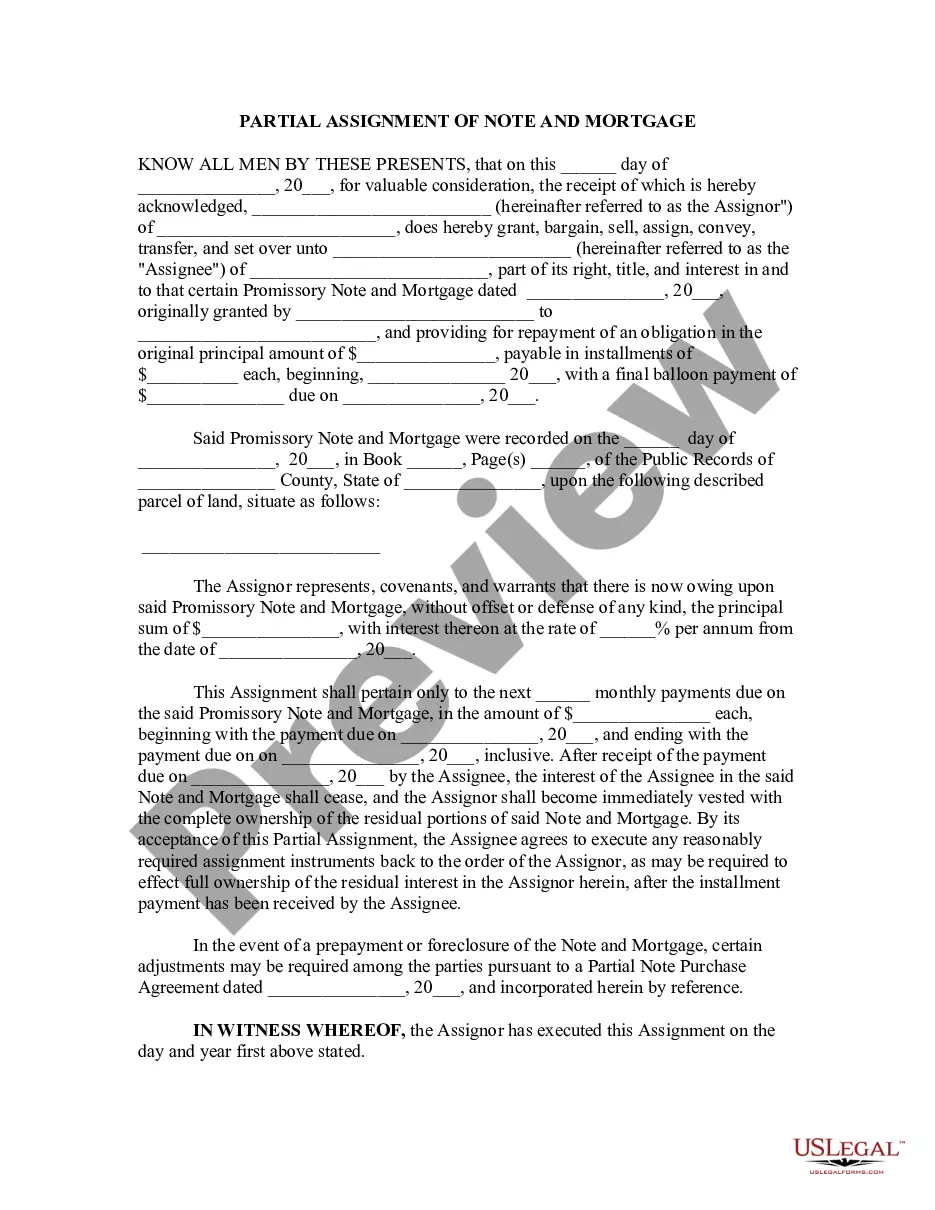

Georgia Partial Assignment of Life Insurance Policy as Collateral

Description

How to fill out Partial Assignment Of Life Insurance Policy As Collateral?

Have you been in the place in which you need to have files for both organization or personal reasons almost every working day? There are a variety of lawful record templates available online, but locating types you can rely is not simple. US Legal Forms gives a large number of type templates, just like the Georgia Partial Assignment of Life Insurance Policy as Collateral, that happen to be written in order to meet federal and state demands.

When you are already knowledgeable about US Legal Forms website and possess an account, merely log in. After that, it is possible to down load the Georgia Partial Assignment of Life Insurance Policy as Collateral format.

If you do not provide an accounts and wish to start using US Legal Forms, follow these steps:

- Discover the type you will need and make sure it is for that right area/county.

- Make use of the Preview option to check the form.

- Browse the explanation to actually have chosen the proper type.

- When the type is not what you are looking for, take advantage of the Search discipline to obtain the type that meets your needs and demands.

- Once you get the right type, click on Acquire now.

- Choose the prices prepare you want, complete the specified information to generate your account, and pay for your order with your PayPal or charge card.

- Choose a hassle-free document format and down load your duplicate.

Get every one of the record templates you might have bought in the My Forms menus. You can get a extra duplicate of Georgia Partial Assignment of Life Insurance Policy as Collateral anytime, if necessary. Just go through the necessary type to down load or print out the record format.

Use US Legal Forms, by far the most considerable variety of lawful types, in order to save time and steer clear of blunders. The assistance gives expertly produced lawful record templates which can be used for a range of reasons. Produce an account on US Legal Forms and start creating your lifestyle easier.

Form popularity

FAQ

Collateral assignment of life insurance is a method of providing a lender with collateral when you apply for a loan. In this case, the collateral is your life insurance policy's face value, which could be used to pay back the amount you owe in case you die while in debt.

Under partial assignment, only the designated amount is paid to the assignee. Rest of the proceeds are paid to the nominee. If your expected insurance proceeds are more than the loan amount, you should opt for partial assignment.

A collateral assignment of life insurance is a conditional assignment appointing a lender as an assignee of a policy. Essentially, the lender has a claim to some or all of the death benefit until the loan is repaid. The death benefit is used as collateral for a loan.

Collateral assignment, on the other hand, is a temporary and often revocable arrangement. The policyholder retains ownership and control over the policy but agrees that the lender has a claim to a part of the death benefit if the loan is not repaid.

Which of these actions is taken when a policyowner uses a Life Insurance policy as collateral for a bank loan? Collateral assignment" A policyowner using the Life Insurance policy as collateral for a bank loan normally would make a collateral assignment.

A collateral assignment pledges a permanent life insurance policy's cash value and death benefits to another party and is most commonly used to secure a loan taken out by the policyowner. A collateral assignment primarily serves to protect the repayment interest of the lender.

If you have a life insurance policy, you're in luck, because most businesses typically accept life insurance as collateral as they can guarantee funds if the borrower dies or defaults.

A life insurance policy can be assigned when rights of one person are transferred to another. The rights to your insurance policy can be transferred to someone else for various reasons. The process is known as assignment.