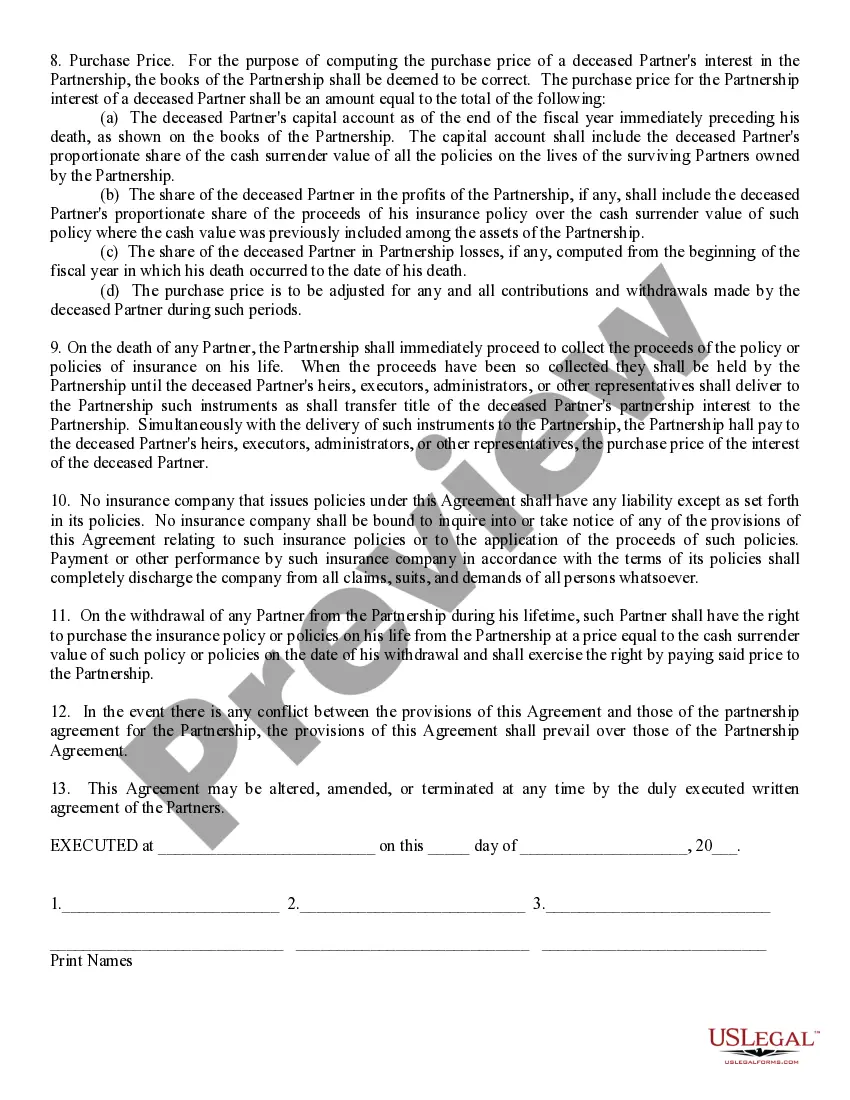

Georgia Sale of Deceased Partner's Interest refers to the legal process in the state of Georgia that allows the surviving partners of a partnership to acquire the deceased partner's share. This typically occurs when a partner passes away, and the remaining partners wish to continue the business without bringing in a new partner. The Georgia Sale of Deceased Partner's Interest can be categorized into two types: voluntary buyout and mandatory buyout. 1. Voluntary Buyout: In this type, the surviving partners can choose to purchase the deceased partner's interest voluntarily. This allows the remaining partners to maintain control over the business and continue its operations without interference from external parties. The voluntary buyout may involve negotiations between the surviving partners and the deceased partner's estate to determine a fair price for the deceased partner's interest. 2. Mandatory Buyout: In some cases, the partnership agreement or state laws may stipulate a mandatory buyout of the deceased partner's interest. This means that the surviving partners are legally obligated to purchase the deceased partner's share. The terms and conditions for the mandatory buyout may vary depending on the partnership agreement and relevant laws. Key Factors in Georgia Sale of Deceased Partner's Interest: 1. Partnership Agreement: The terms and conditions outlined in the partnership agreement play a vital role in determining how the sale of a deceased partner's interest will be executed. It may include provisions related to valuation methods, buyout terms, and procedures to be followed in case of a partner's death. 2. Valuation of Deceased Partner's Interest: Establishing the fair market value of the deceased partner's interest is essential in determining the purchase price. Various valuation methods such as book value, capitalization of earnings, or appraisals may be used. The chosen method must conform to the partnership agreement and Georgia law. 3. Funding the Purchase: The surviving partners need to arrange for the necessary funds to complete the purchase of the deceased partner's interest. They may utilize personal savings, obtain loans, or seek external financing options to cover the acquisition costs. 4. Legal Formalities: Completing the sale requires adherence to legal formalities such as drafting and signing a purchase agreement, transferring ownership rights, updating partnership documents, and fulfilling any statutory requirements or filings with the Georgia Secretary of State. 5. Tax Implications: The sale of a deceased partner's interest may have tax implications for both the estate and the surviving partners. Consulting with a tax advisor or attorney is crucial to understand and comply with tax obligations arising from the transaction. In conclusion, the Georgia Sale of Deceased Partner's Interest involves the legal procedures for the surviving partners to acquire the share of a deceased partner in a partnership. The process can be categorized as voluntary or mandatory buyout and involves factors such as partnership agreement provisions, valuation of the deceased partner's interest, funding the purchase, legal formalities, and tax implications.

Georgia Sale of Deceased Partner's Interest

Description

How to fill out Georgia Sale Of Deceased Partner's Interest?

Have you been in the situation where you need papers for sometimes company or personal uses just about every day? There are a lot of lawful papers layouts available on the net, but locating ones you can depend on isn`t simple. US Legal Forms provides 1000s of develop layouts, just like the Georgia Sale of Deceased Partner's Interest, that are written to satisfy federal and state requirements.

When you are currently informed about US Legal Forms website and possess your account, merely log in. Afterward, you are able to download the Georgia Sale of Deceased Partner's Interest template.

Should you not provide an profile and need to begin using US Legal Forms, adopt these measures:

- Obtain the develop you want and ensure it is to the appropriate town/region.

- Use the Review key to analyze the form.

- Browse the explanation to actually have chosen the right develop.

- When the develop isn`t what you`re trying to find, utilize the Look for area to obtain the develop that fits your needs and requirements.

- If you discover the appropriate develop, click on Acquire now.

- Opt for the costs program you would like, fill in the required details to produce your bank account, and purchase your order utilizing your PayPal or charge card.

- Select a handy document format and download your copy.

Locate all the papers layouts you might have purchased in the My Forms menus. You can get a further copy of Georgia Sale of Deceased Partner's Interest any time, if required. Just click on the required develop to download or printing the papers template.

Use US Legal Forms, one of the most considerable assortment of lawful forms, to save some time and avoid faults. The support provides professionally produced lawful papers layouts that can be used for a variety of uses. Create your account on US Legal Forms and commence creating your life easier.