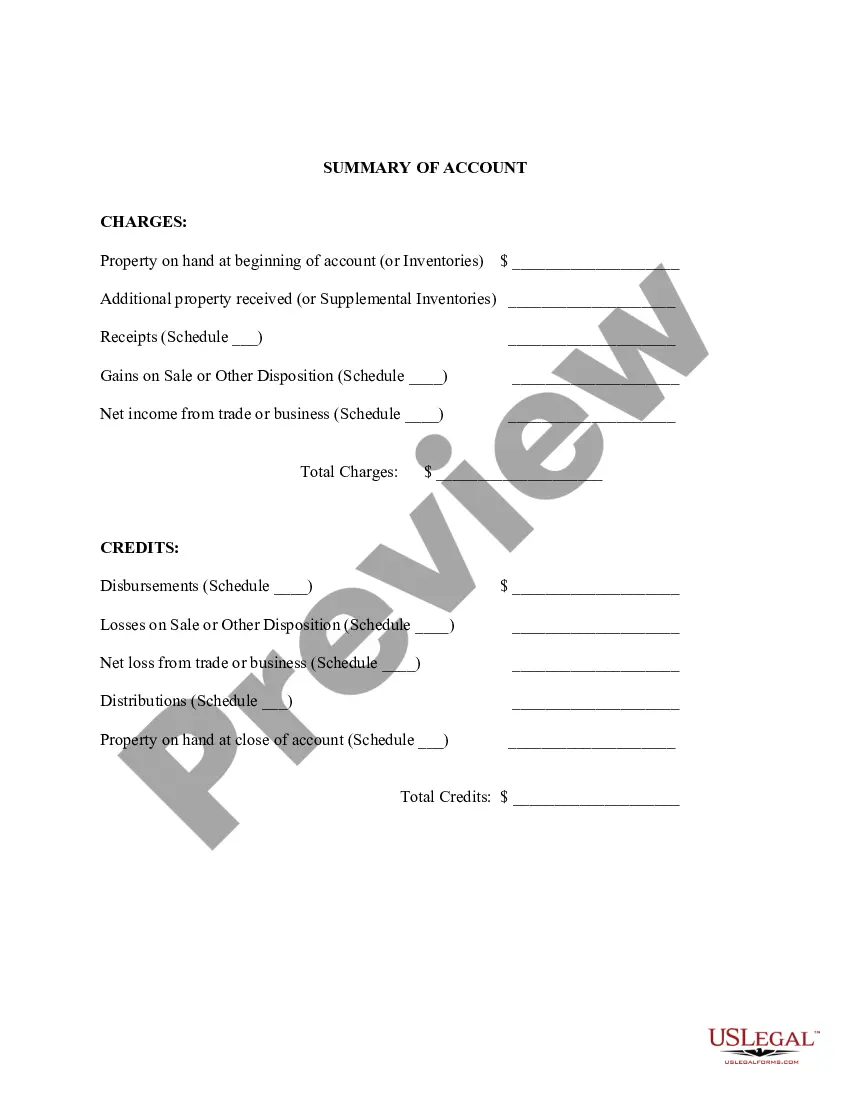

Georgia Summary of Account for Inventory of Business is a document that provides a comprehensive overview and analysis of the inventory held by a business in the state of Georgia. It serves as an important tool for both internal business management and external stakeholders, such as investors, creditors, and regulatory authorities. The Georgia Summary of Account for Inventory of Business includes various key components and relevant data points. These may vary depending on the nature of the business and the industry it operates in. Some common elements included in the summary are as follows: 1. Description of Inventory: This section provides a detailed description of the types of inventory held by the business. It encompasses raw materials, work-in-progress items, and finished goods, along with any unique characteristics or specifications. 2. Valuation Methods: The summary outlines the methodology used to value the inventory. It may include methods such as cost, lower of cost or market value, or specific identification, depending on the accounting principles followed by the company. 3. Quantity and Units: The summary includes the quantity of each inventory item held by the business, usually measured in physical units or standardized measurements. This information helps in assessing the overall size and scope of the inventory. 4. Value: This section provides an estimation of the monetary value associated with the inventory. It may include the total inventory value as well as the individual values assigned to each item. This valuation is crucial for financial reporting, taxation, and decision-making purposes. 5. Age Analysis: An age analysis of inventory is often included to track how long different items have been in stock. This helps in identifying slow-moving or obsolete inventory items that may require special attention or disposition. 6. Turnover Ratio: The summary may calculate the inventory turnover ratio, which indicates the efficiency of inventory management. It is calculated by dividing the cost of goods sold by the average inventory value during a specific period. A higher turnover ratio implies efficient inventory management. 7. Differences and Adjustments: If there are any significant variances or adjustments between physical counts and recorded quantities, they are duly noted. This section highlights potential discrepancies that may require further investigation and adjustment. Some different types of Georgia Summary of Account for Inventory of Business include: 1. Periodic Summary: This type of summary is prepared periodically, such as monthly, quarterly, or annually, to provide a snapshot of the current status and management of inventory. 2. Year-End Summary: This summary is prepared at the end of a business's fiscal year to finalize the inventory records, adjust any discrepancies, and facilitate the preparation of financial statements and tax returns. 3. Audit Summary: If the business undergoes an external audit, a specialized summary may be prepared to meet the audit requirements and provide assurance over the accuracy and completeness of the inventory records. In conclusion, the Georgia Summary of Account for Inventory of Business is a detailed document that outlines the various aspects of a business's inventory. It presents essential information related to inventory valuation, quantity, age analysis, and turnover ratio. Different types of summaries are prepared based on the frequency and purpose of reporting, such as periodic, year-end, and audit summaries. Efficient inventory management and accurate reporting of inventory play a significant role in the financial success and sustainability of businesses operating in Georgia.

Georgia Summary of Account for Inventory of Business

Description

How to fill out Georgia Summary Of Account For Inventory Of Business?

Have you been within a situation in which you need to have files for sometimes organization or individual functions just about every day? There are a lot of authorized file layouts accessible on the Internet, but getting versions you can rely is not easy. US Legal Forms provides a large number of form layouts, such as the Georgia Summary of Account for Inventory of Business, which can be written to satisfy federal and state specifications.

Should you be already informed about US Legal Forms web site and have a merchant account, basically log in. Afterward, you are able to download the Georgia Summary of Account for Inventory of Business web template.

Unless you provide an profile and want to start using US Legal Forms, abide by these steps:

- Get the form you want and make sure it is for that correct town/area.

- Take advantage of the Review switch to analyze the shape.

- Browse the outline to ensure that you have chosen the correct form.

- In case the form is not what you`re looking for, make use of the Search discipline to discover the form that fits your needs and specifications.

- Once you discover the correct form, simply click Purchase now.

- Opt for the rates program you need, complete the required info to make your account, and pay money for your order with your PayPal or Visa or Mastercard.

- Decide on a handy data file file format and download your backup.

Locate all of the file layouts you possess bought in the My Forms food list. You can obtain a more backup of Georgia Summary of Account for Inventory of Business at any time, if necessary. Just go through the needed form to download or print the file web template.

Use US Legal Forms, the most extensive variety of authorized kinds, to conserve time as well as stay away from blunders. The service provides professionally produced authorized file layouts which you can use for a selection of functions. Produce a merchant account on US Legal Forms and initiate creating your daily life a little easier.

Form popularity

FAQ

You'd be surprised to know that many people think inventory is simply an expense, because they are purchasing it for resale. It's an asset. You are buying/creating an asset, so it should be shown on your balance sheet as such in an inventory asset account.

Business inventory is exempt from state property taxes (as of January 1, 2016). Almost all (93 percent) of Georgia's counties and over 140 of the cities have adopted a Level One Freeport Exemption, set at 20, 40, 60, 80 or 100 percent of the inventory value.

Inventory tax is a property tax that is determined by the value of inventory and usually falls under a Business Tangible Personal Property tax. Other types of property that often fall under this same classification are machinery, office equipment, and furniture.

In fact, in some states, inventory carries additional taxes, though the exact amount varies by location. This means that inventory is one of those expenses that is very difficult to offset come tax time, and you need to be aware of how much you can afford to keep.

A company's inventory typically involves goods in three stages of production: raw goods, in-progress goods, and finished goods that are ready for sale. Inventory accounting will assign values to the items in each of these three processes and record them as company assets.

Businesses generally must use inventories for income tax purposes when necessary to clearly reflect income. To clearly reflect income, businesses must take inventories at the beginning and end of each tax year in which the production, purchase or sale of merchandise is an income-producing factor.

Some goods are exempt from sales tax under Georgia law. Examples include some prescription drugs, medical supplies, and manufacturing equipment. Non-prepared food items are exempt from state sales tax, but are subject to local sales taxes.

Licensed, nonprofit in-patient general hospitals, mental hospitals, nursing homes, and hospices. Nonprofit private schools any combination of grades 1-12. Nonprofit blood banks. Nonprofit groups whose primary activity is raising money for public libraries.