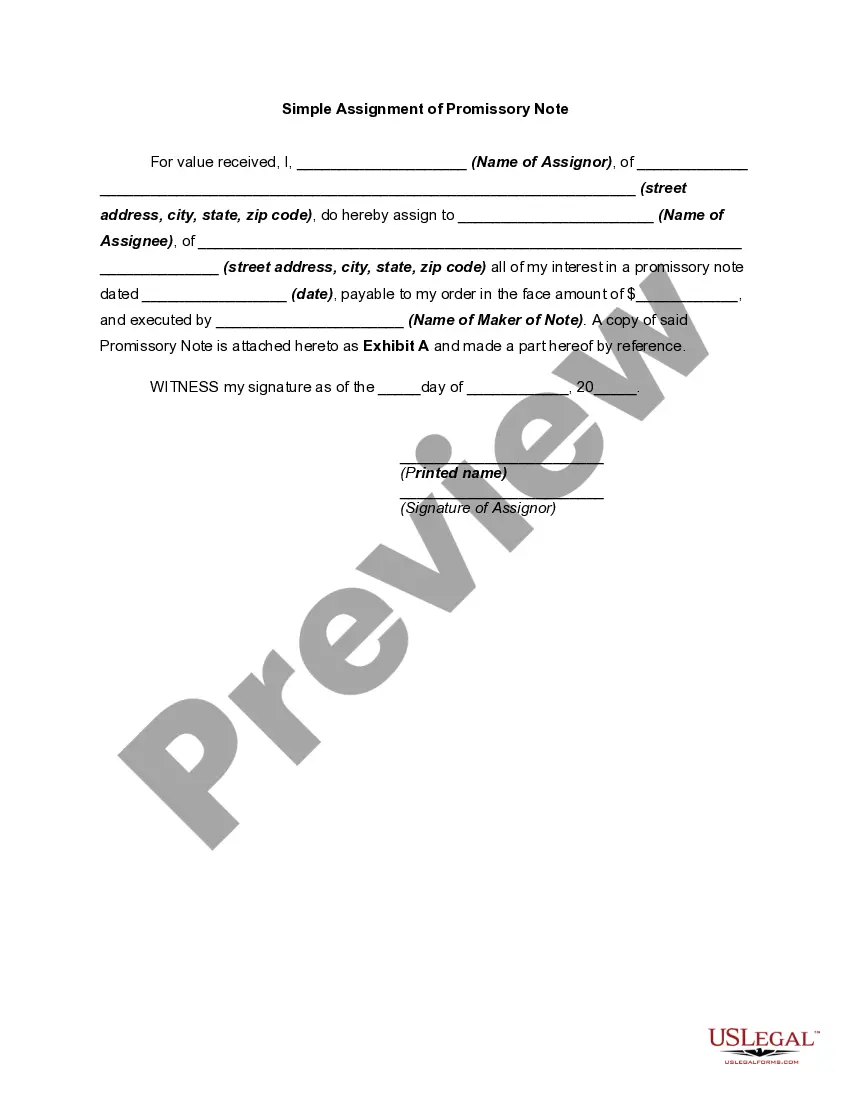

A Georgia Simple Promissory Note for Family Loan is a legally binding document that outlines the terms and conditions of a loan between family members. It serves as evidence of the loan agreement, specifying the amount borrowed, repayment terms, and any other pertinent details. This type of promissory note is typically used when a family member lends money to another family member for various purposes, such as education, medical expenses, or starting a business. It provides a formal structure to the loan, ensuring both parties are clear on their rights and obligations. The Georgia Simple Promissory Note for Family Loan may include the following key elements: 1. Parties Involved: It identifies the lender (the family member providing the loan) and the borrower (the family member receiving the loan). Their full legal names and contact information should be stated. 2. Loan Amount: This section specifies the total amount of money being borrowed. It is crucial to be precise and include the currency. 3. Repayment Terms: The note sets the repayment terms agreed upon by both parties. It outlines the repayment schedule, including the frequency of payments (monthly, bi-monthly, lump sum), the due dates, and the duration of the loan. The interest rate, if applicable, should also be mentioned. 4. Prepayment and Late Fees: This section clarifies whether the borrower can make early repayments without penalties and if there are any consequences for late payments. 5. Collateral or Security: If the loan is secured by any assets or properties, such as a car or house, it should be explicitly mentioned, along with relevant details. 6. Governing Law: As the Georgia Simple Promissory Note for Family Loan is specific to the state, it should state that Georgia law governs the agreement. Different types of Georgia Simple Promissory Notes for Family Loans can vary depending on their purpose or additional clauses involved. Some common variations include: 1. Interest-Free Promissory Note: This type of note specifies that the loaned amount is interest-free, meaning the borrower will not be required to pay any interest on the borrowed funds. 2. Demand Promissory Note: Unlike a regular promissory note with a fixed repayment schedule, a demand note allows the lender to request repayment at any time. 3. Balloon Promissory Note: This note structure includes periodic payments with a final "balloon" payment, where the remaining balance is due in full. It is often used for larger loans that the borrower intends to repay within a specific timeframe. 4. Installment Promissory Note: This type of note breaks down the loan repayment into equal installments over a predetermined period, making it easier for the borrower to manage the payments. In summary, a Georgia Simple Promissory Note for Family Loan establishes a formal agreement between family members for borrowing and lending money. It ensures transparency and protects the rights and interests of both parties, making clear the terms and conditions of the loan.

Georgia Simple Promissory Note for Family Loan

Description

How to fill out Georgia Simple Promissory Note For Family Loan?

US Legal Forms - one of the largest libraries of legal kinds in the United States - offers a wide array of legal record templates you can down load or print out. Utilizing the web site, you will get thousands of kinds for business and specific functions, categorized by types, states, or search phrases.You can find the most recent versions of kinds like the Georgia Simple Promissory Note for Family Loan in seconds.

If you already have a monthly subscription, log in and down load Georgia Simple Promissory Note for Family Loan through the US Legal Forms library. The Obtain button will appear on each kind you see. You have access to all formerly saved kinds inside the My Forms tab of the profile.

If you want to use US Legal Forms the very first time, here are basic instructions to help you get started off:

- Be sure to have selected the right kind for your personal area/state. Select the Review button to analyze the form`s content material. Read the kind explanation to ensure that you have selected the appropriate kind.

- In case the kind doesn`t suit your demands, utilize the Lookup field towards the top of the screen to discover the one that does.

- If you are satisfied with the form, validate your decision by clicking the Purchase now button. Then, choose the prices plan you prefer and provide your qualifications to sign up to have an profile.

- Method the deal. Utilize your charge card or PayPal profile to complete the deal.

- Pick the formatting and down load the form in your system.

- Make modifications. Load, edit and print out and sign the saved Georgia Simple Promissory Note for Family Loan.

Every format you included in your bank account lacks an expiry particular date and is your own property for a long time. So, in order to down load or print out one more duplicate, just proceed to the My Forms portion and click on on the kind you want.

Get access to the Georgia Simple Promissory Note for Family Loan with US Legal Forms, by far the most substantial library of legal record templates. Use thousands of professional and status-certain templates that satisfy your business or specific requirements and demands.