A nonprofit corporation is one that is organized for charitable or benevolent purposes. These corporations include certain hospitals, universities, churches, and other religious organizations. A nonprofit entity does not have to be a nonprofit corporation, however. Nonprofit corporations do not have shareholders, but have members or a perpetual board of directors or board of trustees.

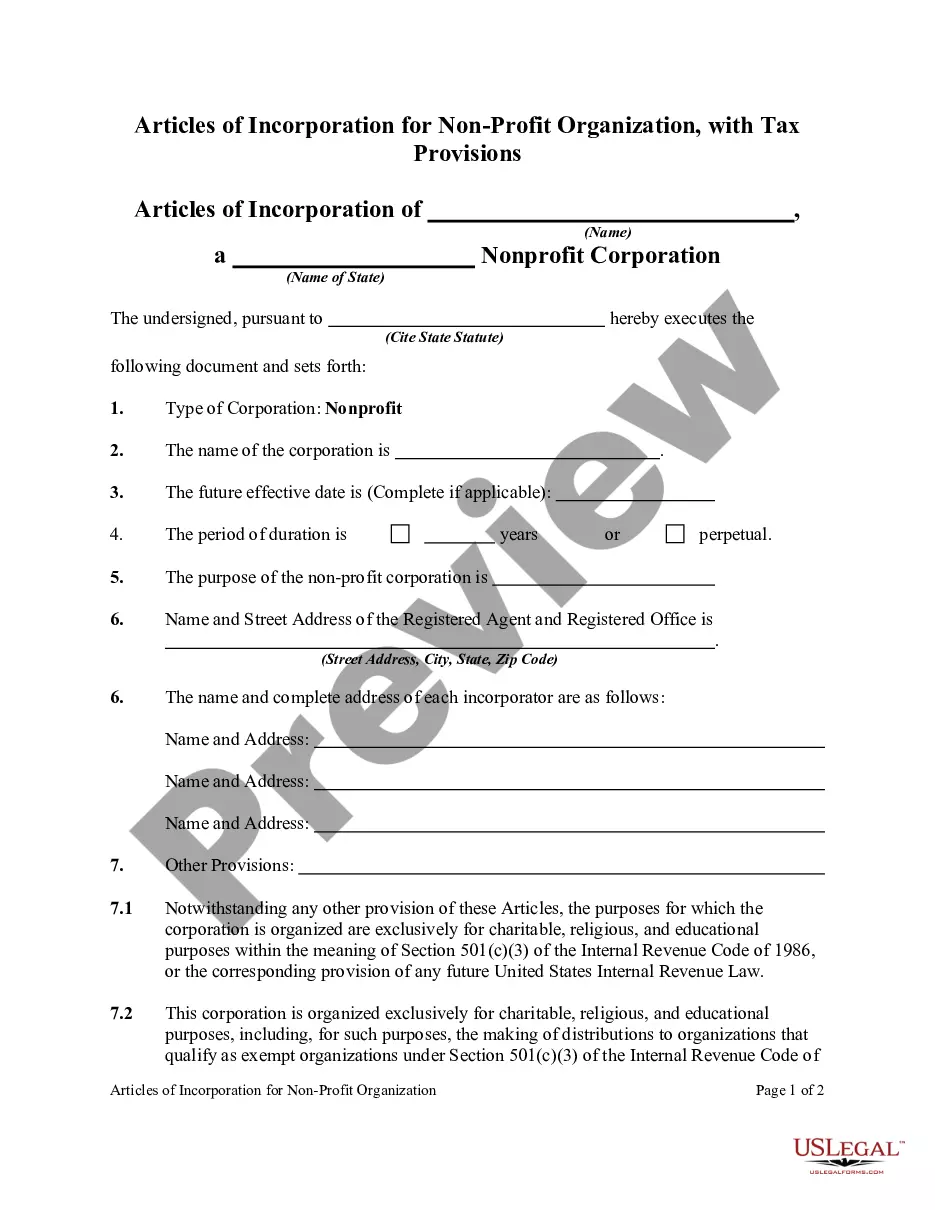

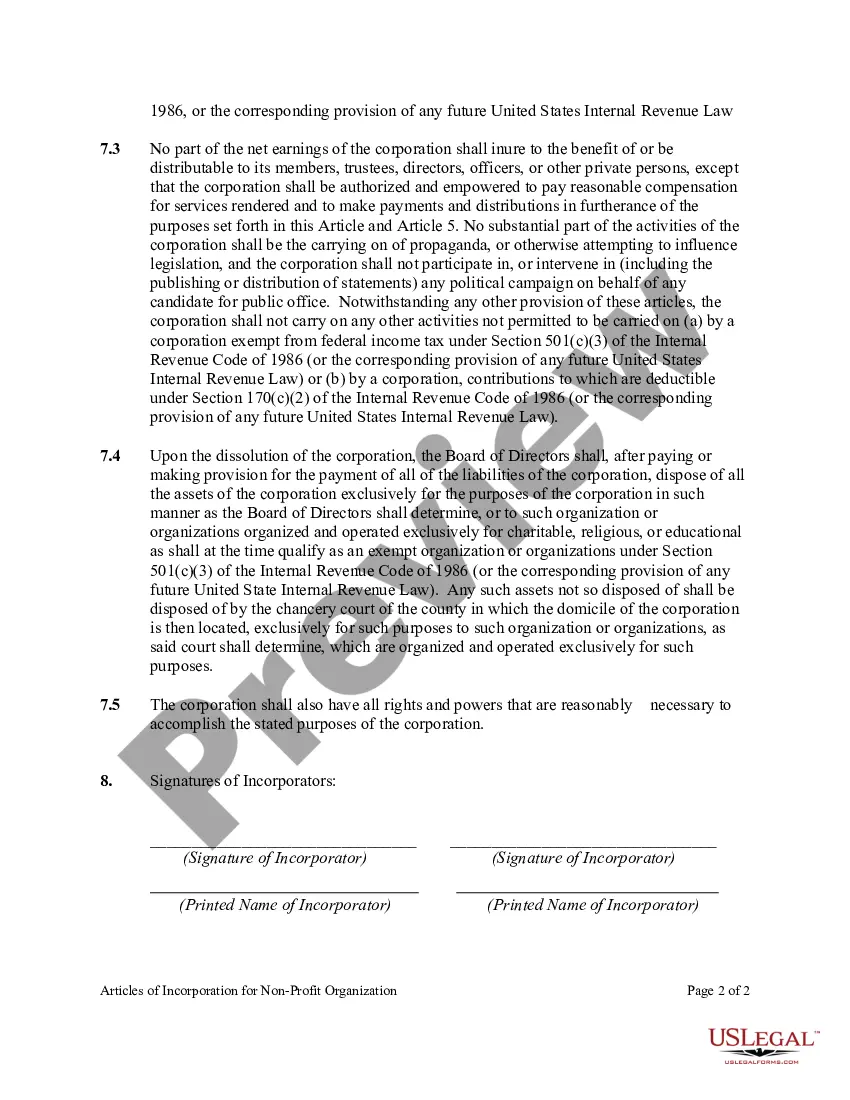

The Georgia Articles of Incorporation for Non-Profit Organizations with Tax Provisions is an essential legal document filed with the Georgia Secretary of State's office to establish the existence of a non-profit organization in the state. These articles outline various important aspects related to the organization, including its purpose, structure, governance, and tax-exempt status. The incorporation process not only grants legal recognition to the non-profit but also ensures compliance with state and federal regulations. Under Georgia law, there are two main types of Articles of Incorporation for Non-Profit Organizations: 1. Standard Articles of Incorporation: These articles contain the basic information required to form a non-profit organization in Georgia. They include key details such as the organization's name, purpose, registered agent and their address, duration of existence, initial registered office address, and the names and addresses of the incorporates. While these standard articles establish the organization's legal existence, they do not include specific provisions related to tax-exempt status. 2. Articles of Incorporation with Tax Provisions: These articles expand upon the standard articles by including additional provisions required to meet the qualifications for federal tax-exempt status under Section 501(c)(3) of the Internal Revenue Code. These provisions outline the organization's specific charitable, educational, religious, scientific, or other exempt purposes, the way it will operate in accordance with these purposes, and the manner in which its assets will be distributed upon dissolution. These provisions are crucial for non-profit organizations seeking federal tax-exempt status and are submitted to the IRS along with the application for recognition as a tax-exempt entity. It is important to note that while these two types of articles are distinct, both are necessary for non-profit organizations in Georgia. The standard articles establish the legal foundation, while the articles with tax provisions enable the organization to qualify for federal tax-exempt status, making it eligible for certain tax benefits and charitable contributions. In conclusion, the Georgia Articles of Incorporation for Non-Profit Organizations with Tax Provisions serve as a crucial legal document that establishes the existence of a non-profit entity and outlines its purpose, governance, and compliance with tax regulations. By carefully following the guidelines and including the necessary provisions, non-profit organizations can successfully navigate the incorporation process and obtain tax-exempt status for their operations.The Georgia Articles of Incorporation for Non-Profit Organizations with Tax Provisions is an essential legal document filed with the Georgia Secretary of State's office to establish the existence of a non-profit organization in the state. These articles outline various important aspects related to the organization, including its purpose, structure, governance, and tax-exempt status. The incorporation process not only grants legal recognition to the non-profit but also ensures compliance with state and federal regulations. Under Georgia law, there are two main types of Articles of Incorporation for Non-Profit Organizations: 1. Standard Articles of Incorporation: These articles contain the basic information required to form a non-profit organization in Georgia. They include key details such as the organization's name, purpose, registered agent and their address, duration of existence, initial registered office address, and the names and addresses of the incorporates. While these standard articles establish the organization's legal existence, they do not include specific provisions related to tax-exempt status. 2. Articles of Incorporation with Tax Provisions: These articles expand upon the standard articles by including additional provisions required to meet the qualifications for federal tax-exempt status under Section 501(c)(3) of the Internal Revenue Code. These provisions outline the organization's specific charitable, educational, religious, scientific, or other exempt purposes, the way it will operate in accordance with these purposes, and the manner in which its assets will be distributed upon dissolution. These provisions are crucial for non-profit organizations seeking federal tax-exempt status and are submitted to the IRS along with the application for recognition as a tax-exempt entity. It is important to note that while these two types of articles are distinct, both are necessary for non-profit organizations in Georgia. The standard articles establish the legal foundation, while the articles with tax provisions enable the organization to qualify for federal tax-exempt status, making it eligible for certain tax benefits and charitable contributions. In conclusion, the Georgia Articles of Incorporation for Non-Profit Organizations with Tax Provisions serve as a crucial legal document that establishes the existence of a non-profit entity and outlines its purpose, governance, and compliance with tax regulations. By carefully following the guidelines and including the necessary provisions, non-profit organizations can successfully navigate the incorporation process and obtain tax-exempt status for their operations.