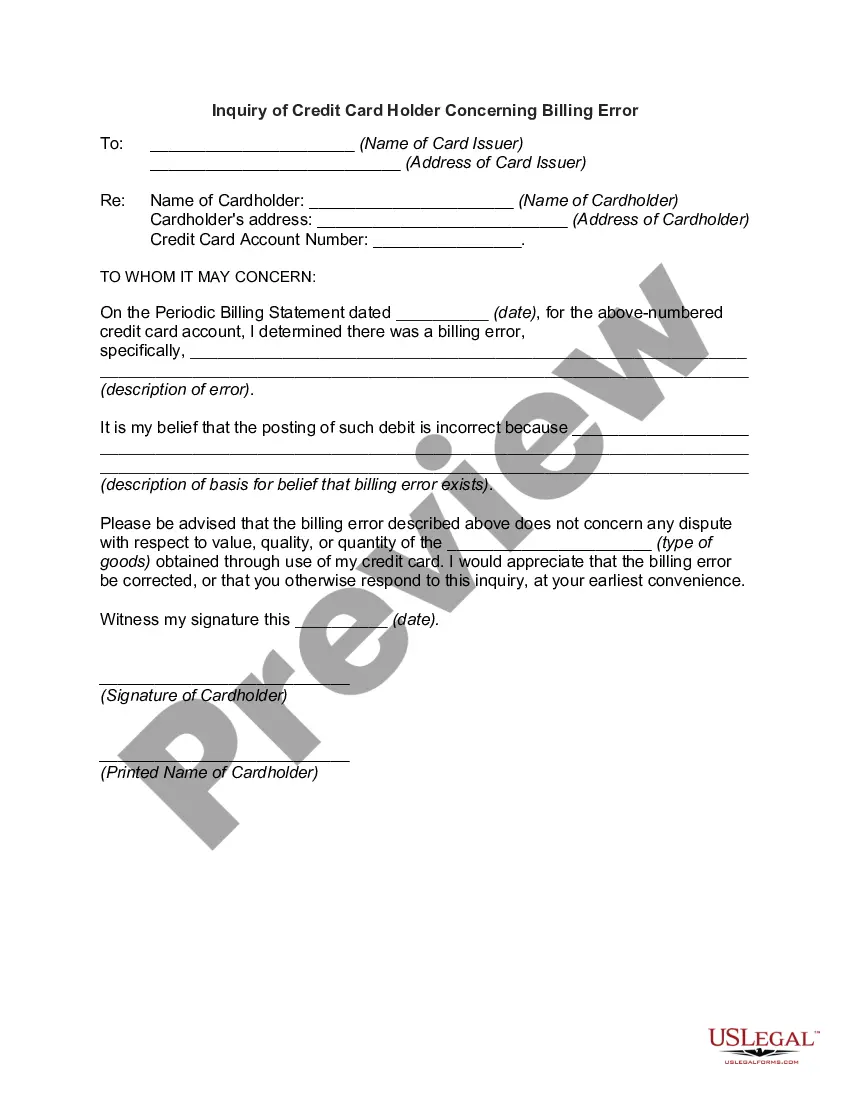

Georgia Inquiry of Credit Cardholder Concerning Billing Error is a legal process that allows credit cardholders in the state of Georgia to dispute and rectify billing errors on their credit card statements. This inquiry provides an avenue for consumers to seek resolution and potential reimbursement for any discrepancies or unauthorized charges. The Georgia Inquiry of Credit Cardholder Concerning Billing Error is governed by the Fair Credit Billing Act (CBA), a federal law that sets guidelines for resolving billing disputes. Under this act, credit cardholders have specific rights and procedures to follow when challenging inaccurate or fraudulent charges. There are several types of Georgia Inquiry of Credit Cardholder Concerning Billing Error, including: 1. Unauthorized Charges: This type occurs when the credit cardholder identifies charges on their statement that they did not authorize or make. It is vital for cardholders to act promptly in reporting such errors to their credit card issuer to ensure timely resolution and prevent further unauthorized activities. 2. Incorrect Amounts: Sometimes, credit card statements may show erroneous or incorrect billing amounts. This type of billing error may include overcharging, double billing, or incorrect calculations. Credit cardholders should thoroughly review their statements and compare them with receipts to identify and report any discrepancies promptly. 3. Non-Delivery of Goods or Services: This category pertains to situations where a credit cardholder made a purchase but did not receive the goods or services promised. If the cardholder has attempted to resolve the matter with the merchant but was unsuccessful, they can file an inquiry to dispute the charge and potentially secure a refund. 4. Defective Merchandise: In cases where the goods purchased using a credit card are faulty, damaged, or not as advertised, the cardholder can initiate an inquiry. By doing so, they seek resolution from the merchant or request a refund, if applicable. When faced with any of these possible billing errors, Georgia credit cardholders should take immediate action. They must contact their credit card issuer within 60 days of receiving the statement that contains the error. The cardholder should send a written inquiry, including their name, account number, the specific error details, and any supporting documentation. It is crucial for Georgia credit cardholders to keep records of all communications and documents related to their billing inquiry. This includes correspondence with the credit card issuer, receipts, invoices, and any evidence supporting their claim. The credit card issuer is required to acknowledge receipt of the inquiry within 30 days and investigate the matter within 90 days. In conclusion, the Georgia Inquiry of Credit Cardholder Concerning Billing Error offers an important recourse for Georgia residents who encounter billing discrepancies on their credit card statements. By actively engaging in the inquiry process and following the guidelines set forth by the CBA, credit cardholders can seek resolution and protect their rights as consumers.

Georgia Inquiry of Credit Cardholder Concerning Billing Error

Description

How to fill out Georgia Inquiry Of Credit Cardholder Concerning Billing Error?

Finding the right legal file web template could be a have a problem. Needless to say, there are a variety of layouts available on the Internet, but how will you find the legal develop you require? Utilize the US Legal Forms site. The assistance offers thousands of layouts, such as the Georgia Inquiry of Credit Cardholder Concerning Billing Error, that can be used for enterprise and private requirements. Each of the kinds are checked out by pros and fulfill state and federal demands.

If you are currently authorized, log in to the profile and click the Obtain button to get the Georgia Inquiry of Credit Cardholder Concerning Billing Error. Utilize your profile to look throughout the legal kinds you might have ordered formerly. Visit the My Forms tab of your own profile and get one more copy from the file you require.

If you are a brand new consumer of US Legal Forms, listed here are basic guidelines for you to comply with:

- Initially, make sure you have selected the appropriate develop for your personal town/region. You can examine the form making use of the Preview button and study the form information to guarantee this is basically the best for you.

- In case the develop is not going to fulfill your preferences, take advantage of the Seach field to obtain the correct develop.

- When you are certain that the form is suitable, click the Acquire now button to get the develop.

- Opt for the prices program you want and enter the essential information and facts. Design your profile and purchase the transaction making use of your PayPal profile or Visa or Mastercard.

- Pick the data file file format and download the legal file web template to the device.

- Total, edit and print and indicator the attained Georgia Inquiry of Credit Cardholder Concerning Billing Error.

US Legal Forms will be the largest catalogue of legal kinds where you can see numerous file layouts. Utilize the company to download professionally-created files that comply with status demands.