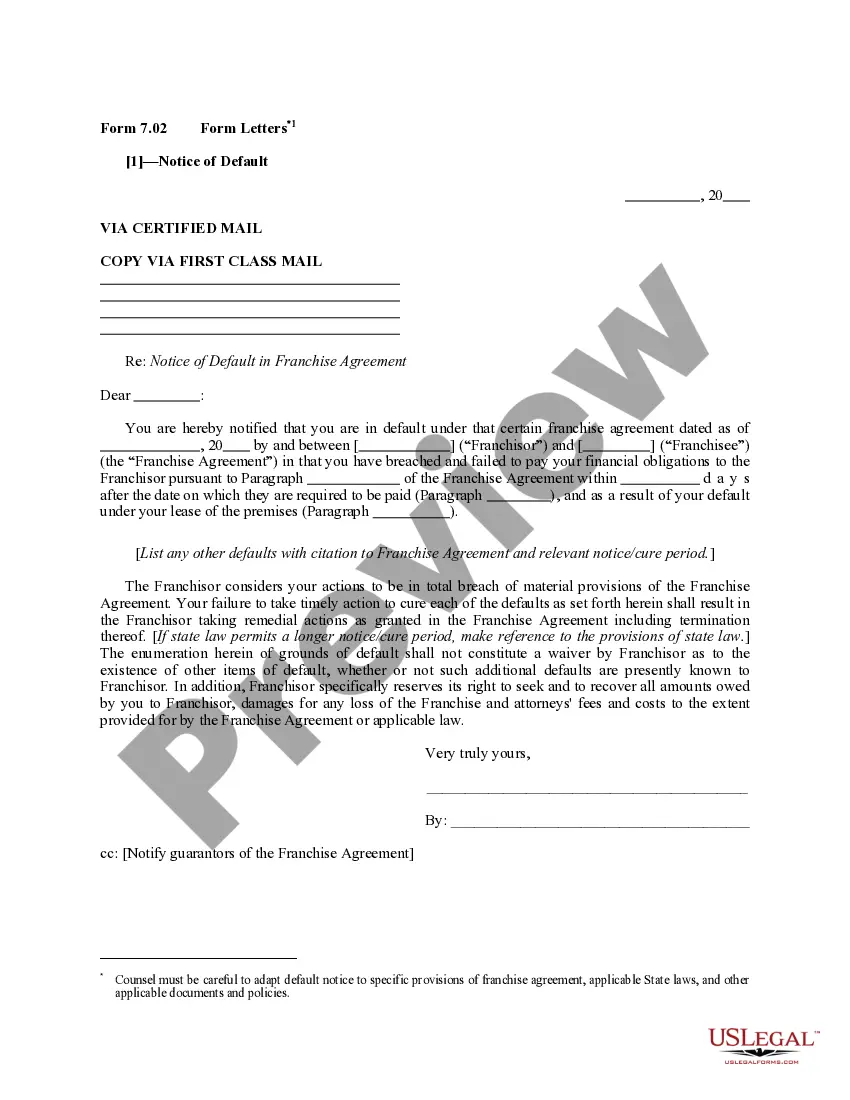

This letter informs a franchisee that he/she is in default of a franchise agreement and failure to take timely action to cure each of the defaults listed in the letter will result in the franchisor taking remedial actions as granted in the agreement.

Georgia Form Letters - Notice of Default

State:

Multi-State

Control #:

US-7-02-1-STP

Format:

Word;

Rich Text

Instant download

Description

How to fill out Form Letters - Notice Of Default?

If you wish to comprehensive, acquire, or print out authorized document themes, use US Legal Forms, the biggest assortment of authorized types, which can be found on the Internet. Use the site`s simple and handy research to obtain the files you will need. Different themes for enterprise and specific purposes are sorted by classes and says, or search phrases. Use US Legal Forms to obtain the Georgia Form Letters - Notice of Default in a handful of click throughs.

Should you be previously a US Legal Forms customer, log in to the account and click on the Acquire button to have the Georgia Form Letters - Notice of Default. You can even access types you earlier delivered electronically within the My Forms tab of the account.

If you are using US Legal Forms initially, follow the instructions under:

- Step 1. Ensure you have selected the shape for your right city/country.

- Step 2. Take advantage of the Review choice to look over the form`s content material. Don`t overlook to learn the explanation.

- Step 3. Should you be not happy together with the kind, take advantage of the Lookup field near the top of the display screen to locate other types in the authorized kind web template.

- Step 4. After you have found the shape you will need, select the Buy now button. Select the costs prepare you prefer and add your qualifications to sign up for an account.

- Step 5. Procedure the transaction. You can use your charge card or PayPal account to finish the transaction.

- Step 6. Select the formatting in the authorized kind and acquire it on the device.

- Step 7. Total, modify and print out or sign the Georgia Form Letters - Notice of Default.

Every authorized document web template you buy is the one you have for a long time. You might have acces to every single kind you delivered electronically inside your acccount. Click on the My Forms segment and choose a kind to print out or acquire yet again.

Remain competitive and acquire, and print out the Georgia Form Letters - Notice of Default with US Legal Forms. There are millions of professional and status-specific types you can utilize for your personal enterprise or specific demands.

Form popularity

FAQ

Property § 44-7-33. (a) Prior to tendering a security deposit, the tenant shall be presented with a comprehensive list of any existing damage to the premises which shall be for the tenant's permanent retention.

A ?default? is a failure to comply with a provision in the lease. ?Curing? or ?remedying? the default means correcting the failure or omission. A common example is a failure to pay the rent on time.

Landlord's Duties as to Repairs and Improvements. The landlord must keep the premises in repair. He shall be liable for all substantial improvements placed upon the premises by his consent.

If there is a tenancy-at-will, the landlord must give the tenant sixty (60) days' notice telling them to leave. If the landlord is willing to allow the tenant to remain but wishes to begin charging rent, the tenant must be given sixty (60) days' notice to start a new tenancy-at-will requiring rent payments.

Accrual of Interest on Rent Owed. All contracts for rent shall bear interest from the time the rent is due. History.

Your landlord is responsible for repairs to keep the property in good condition. Georgia law says that a landlord cannot make a tenant make or pay for repairs, unless that tenant, his/her family or guests caused the damage. For serious repair problems, local housing code departments can inspect for possible violations.

Property § 44-7-1. (a) The relationship of landlord and tenant is created when the owner of real estate grants to another person, who accepts such grant, the right simply to possess and enjoy the use of such real estate either for a fixed time or at the will of the grantor.

Tenancy at Will ? Notice Required for Termination. Sixty days' notice from the landlord or 30 days' notice from the tenant is necessary to terminate a tenancy at will.