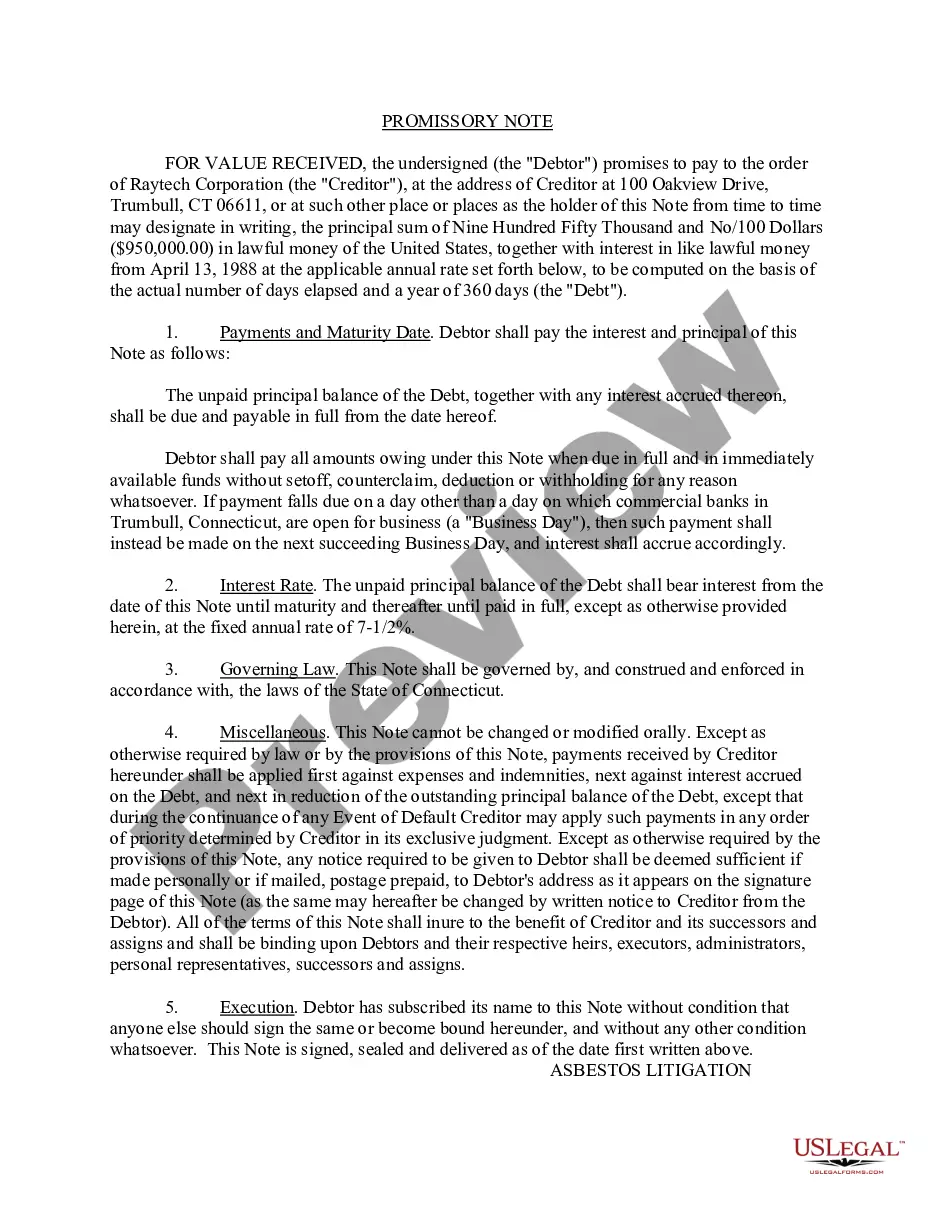

A Georgia promissory note is a legal document that outlines a borrower's promise to repay a specific amount of money to a lender within a designated timeframe. It serves as evidence of a loan agreement between two parties and includes essential terms and conditions to protect both the borrower and lender. One type of Georgia promissory note is a secured promissory note. In this case, the borrower pledges collateral, such as property or vehicles, to secure the loan. If the borrower defaults on payment, the lender has the legal right to seize the pledged assets to recover the outstanding amount. Another type is an unsecured promissory note, which does not require any collateral. It relies solely on the borrower's creditworthiness and trustworthiness. In case of default, the lender may pursue legal action or debt collection methods to recover the owed amount. Georgia promissory notes typically include key information, such as the names and addresses of both the borrower and lender, the loan amount, the interest rate (if any), repayment terms and schedule, late payment penalties, and any applicable default provisions. Both parties should carefully review and understand the terms before signing the promissory note. The Georgia promissory note must comply with the state's laws and regulations regarding interest rates, usury limits, and debt collection practices. It is advisable for both parties to seek legal advice or consult a knowledgeable professional when drafting or signing a promissory note to ensure compliance and protect their rights. In summary, a Georgia promissory note is a legally binding document that formalizes a loan agreement between a borrower and lender. Whether secured or unsecured, the promissory note outlines the terms and conditions of repayment, providing a clear understanding of the agreement and ensuring legal protection for both parties.

Georgia Promissory Note

Description

How to fill out Georgia Promissory Note?

Are you in the situation in which you need to have documents for sometimes organization or personal reasons just about every day time? There are a lot of authorized record layouts available online, but finding types you can rely is not simple. US Legal Forms provides a huge number of form layouts, just like the Georgia Promissory Note, which are composed to meet state and federal specifications.

In case you are already acquainted with US Legal Forms web site and possess a merchant account, just log in. Afterward, you are able to down load the Georgia Promissory Note template.

Unless you provide an profile and need to begin to use US Legal Forms, follow these steps:

- Obtain the form you will need and ensure it is to the appropriate area/region.

- Take advantage of the Review key to review the shape.

- Look at the description to actually have selected the correct form.

- In the event the form is not what you are searching for, take advantage of the Lookup discipline to find the form that meets your requirements and specifications.

- If you find the appropriate form, click Acquire now.

- Opt for the costs plan you would like, fill out the specified info to create your bank account, and buy an order utilizing your PayPal or bank card.

- Select a convenient data file structure and down load your version.

Find all of the record layouts you have purchased in the My Forms food list. You may get a extra version of Georgia Promissory Note any time, if possible. Just select the essential form to down load or produce the record template.

Use US Legal Forms, probably the most considerable collection of authorized types, in order to save some time and avoid faults. The service provides expertly created authorized record layouts which can be used for a selection of reasons. Produce a merchant account on US Legal Forms and start creating your life a little easier.

Form popularity

FAQ

Promissory notes may also be referred to as an IOU, a loan agreement, or just a note. It's a legal lending document that says the borrower promises to repay to the lender a certain amount of money in a certain time frame. This kind of document is legally enforceable and creates a legal obligation to repay the loan.

If the borrower does not repay you, your legal recourse could include repossessing any collateral the borrower put up against the note, sending the debt to a collection agency, selling the promissory note (so someone else can try to collect it), or filing a lawsuit against the borrower.

If timely payment is not made by the borrower, the note holder can file an action to recover payment. Depending upon the amount owed and/or specified in the note, a summons and complaint may be filed with the court or a motion in lieu of complaint may be filed for an expedited judgment.

Promissory notes are legally binding contracts that can hold up in court if the terms of borrowing and repayment are signed and follow applicable laws.

GA Statute of Limitations on Debt Promissory notes ? four-year statute. Oral contract ? four-year statute. Written contracts ? six-year statute.

A promissory note could become invalid if: It isn't signed by both parties. The note violates laws. One party tries to change the terms of the agreement without notifying the other party.

You can use a template or create a promissory note online. But before you begin, you'll need to gather some information and make decisions about the way the loan will be structured. First, you'll need the names and addresses of both the lender (or "payee") and the borrower.