Georgia Assignment of Life Insurance as Collateral

Description

How to fill out Assignment Of Life Insurance As Collateral?

You may commit several hours online searching for the legal document web template that fits the federal and state demands you want. US Legal Forms provides thousands of legal forms that are analyzed by professionals. It is simple to down load or printing the Georgia Assignment of Life Insurance as Collateral from my assistance.

If you have a US Legal Forms bank account, it is possible to log in and then click the Down load option. Afterward, it is possible to comprehensive, revise, printing, or sign the Georgia Assignment of Life Insurance as Collateral. Each legal document web template you get is yours permanently. To get one more duplicate for any obtained type, proceed to the My Forms tab and then click the corresponding option.

If you are using the US Legal Forms site for the first time, stick to the basic instructions listed below:

- Very first, be sure that you have selected the proper document web template for your area/metropolis of your liking. Look at the type information to make sure you have selected the proper type. If available, use the Preview option to appear from the document web template also.

- If you wish to get one more model from the type, use the Research industry to get the web template that suits you and demands.

- Upon having located the web template you desire, click on Acquire now to move forward.

- Find the rates prepare you desire, type your credentials, and register for your account on US Legal Forms.

- Total the transaction. You may use your credit card or PayPal bank account to cover the legal type.

- Find the file format from the document and down load it for your product.

- Make changes for your document if required. You may comprehensive, revise and sign and printing Georgia Assignment of Life Insurance as Collateral.

Down load and printing thousands of document layouts while using US Legal Forms site, that offers the largest assortment of legal forms. Use skilled and status-distinct layouts to tackle your business or personal demands.

Form popularity

FAQ

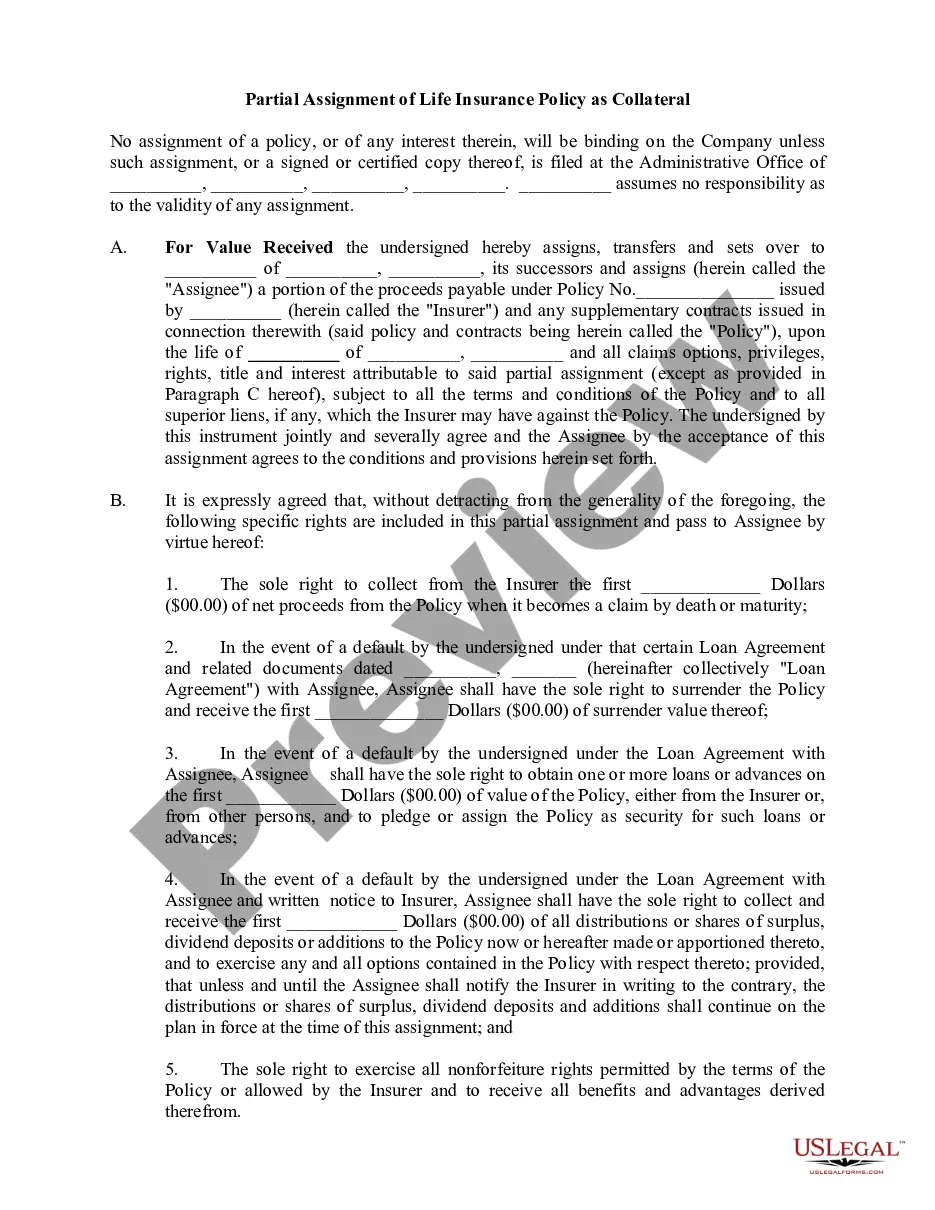

Which of these actions is taken when a policyowner uses a Life Insurance policy as collateral for a bank loan? Collateral assignment" A policyowner using the Life Insurance policy as collateral for a bank loan normally would make a collateral assignment.

A collateral assignment pledges a permanent life insurance policy's cash value and death benefits to another party and is most commonly used to secure a loan taken out by the policyowner. A collateral assignment primarily serves to protect the repayment interest of the lender.

A collateral assignment of life insurance is a conditional assignment appointing a lender as an assignee of a policy. Essentially, the lender has a claim to some or all of the death benefit until the loan is repaid. The death benefit is used as collateral for a loan.

Collateral assignment of life insurance is a method of providing a lender with collateral when you apply for a loan. In this case, the collateral is your life insurance policy's face value, which could be used to pay back the amount you owe in case you die while in debt.

A collateral assignment supersedes your beneficiaries' rights to the death benefit. If you die, the life insurance company pays the lender, or assignee, the loan balance. As noted earlier, any remaining benefit goes to your beneficiaries.

Life insurance can be used as collateral for auto or home loans, but it is also commonly used for small business loans. Often small business owners have to use most of their private money to fund their businesses.

Any type of life insurance policy is acceptable for collateral assignment, provided the insurance company allows assignment for the policy. Some banks may require an escrow account for the life insurance premiums, others may require proof of premiums paid or prepaid.

It shifts the ownership of the insurance policy to other parties without any terms and conditions. This assignment is usually done for money consideration such as raising a loan, out of love or affection towards family members.