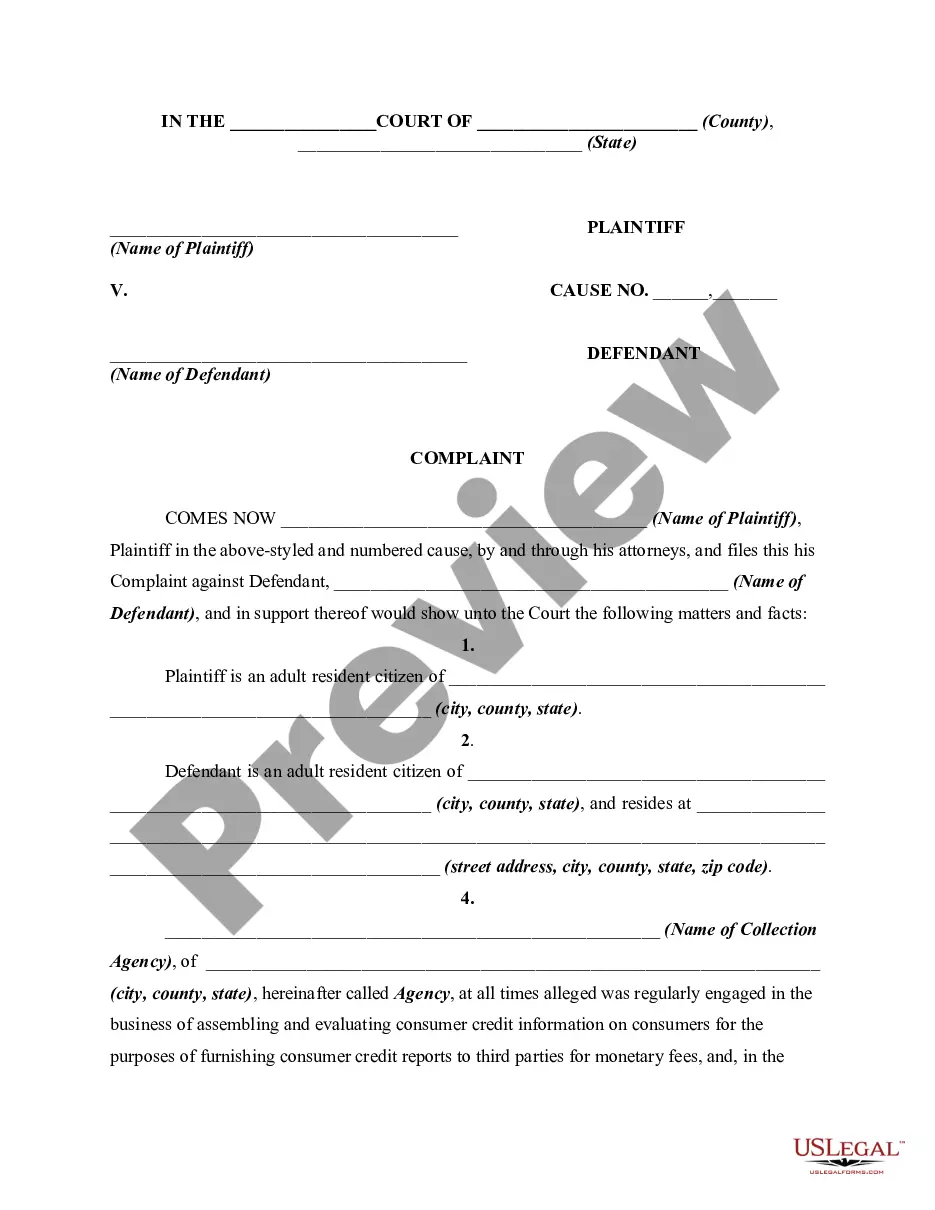

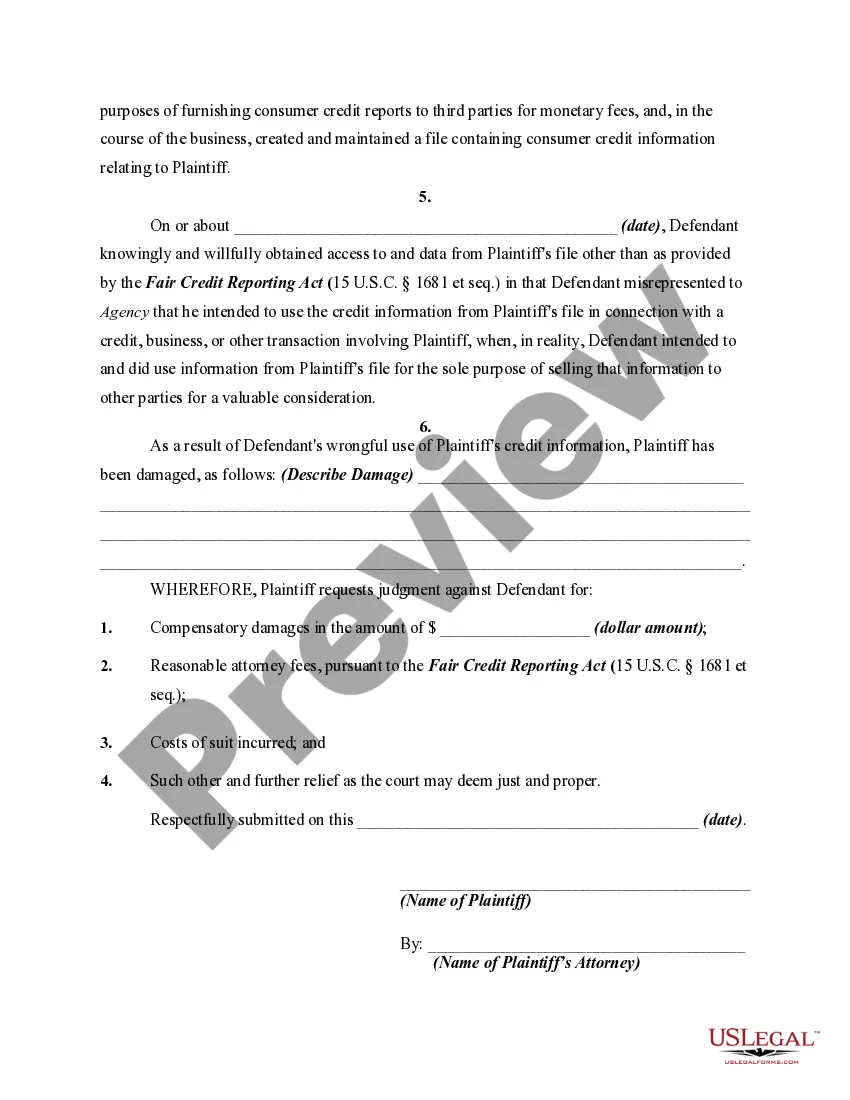

The Fair Credit Reporting Act regulates the use of information on a consumer's personal and financial condition. The most typical transaction which this Act would cover would be where a person applies for a personal loan or other consumer credit. Consumer credit is credit for personal, family, or household use, and not for business or commercial transactions. The purpose of the Act is to insure that consumer information obtained and used is done in such a way as to insure its confidentiality, accuracy, relevancy and proper utilization. Credit reporting bureaus are not permitted to disclose information to persons not having a legitimate use for this information. It is a federal crime to obtain or to furnish a credit report for an improper purpose.

Title: Holding Unlawful Parties Accountable: Guam Complaint by Consumer against Wrongful User of Credit Information Keywords: Guam, complaint, consumer, wrongful, credit information Description: Introduction: In Guam, consumers enjoy certain rights when it comes to the use and protection of their credit information. However, unfortunate instances may occur where individuals or organizations misuse or abuse this sensitive data, causing harm to the affected consumers. This article dives into the details of a Guam Complaint by a Consumer against Wrongful Users of Credit Information, shedding light on the possible types of such complaints and the actions consumers can take to seek justice. Types of Guam Complaints by Consumer against Wrongful User of Credit Information: 1. Identity Theft — This type of complaint arises when an individual's personal information, such as Social Security number, name, or address, is fraudulently used without their knowledge or consent, resulting in financial losses or damaged credit. 2. Unauthorized Credit Inquiries — Consumers may file a complaint when credit information is accessed without their permission by entities seeking to evaluate their creditworthiness or for other purposes without a valid reason. 3. Reporting Incorrect Information — A consumer may dispute a complaint against credit information reporting agencies, creditors, or financial institutions that furnish erroneous information. This could negatively impact credit scores, loan approvals, or employment opportunities. 4. Data Breach — In the unfortunate event of a data breach, where consumer credit information in an entity's possession is compromised, individuals affected may raise a complaint against the responsible party for their failure to adequately protect and secure their data. 5. Discriminatory Lending Practices — Consumers may file complaints if they suspect that lenders or financial institutions unlawfully discriminate based on their race, gender, religion, nationality, disability, or other protected characteristics when determining credit eligibility. Steps to Resolution: 1. Gather evidence — Consumers must collect supporting documents such as credit reports, correspondence, bank statements, and any other relevant information related to the complaint. 2. Contact the Guam Consumer Protection Division — Consumers should reach out to the appropriate government agency, such as the Guam Consumer Protection Division, to report the complaint and seek guidance on the necessary steps to follow. 3. File a formal complaint — Depending on the situation, consumers can file complaints with relevant regulatory bodies, law enforcement agencies, or credit bureaus. Providing comprehensive details regarding the wrongful use of credit information is crucial. 4. Cooperate and seek legal advice — Throughout the process, consumers are encouraged to maintain communication and provide any additional information requested by investigating authorities. Seeking legal advice from professionals familiar with consumer protection laws can be beneficial. 5. Seek resolution and compensation — Enforcing privacy rights and holding wrongful users accountable may result in compensation for damages endured by the consumer. Consumers should work towards attaining a satisfactory resolution, which may involve financial remedies, credit repairs, or corrective action taken by the responsible party. Conclusion: Consumers in Guam have the right to protect their credit information from wrongful use and should take appropriate actions by reporting complaints as soon as they discover any irregularities. By following the outlined steps and seeking assistance from the relevant authorities, consumers can work towards resolution, ensuring their credit information is safeguarded, and justice is served.

Title: Holding Unlawful Parties Accountable: Guam Complaint by Consumer against Wrongful User of Credit Information Keywords: Guam, complaint, consumer, wrongful, credit information Description: Introduction: In Guam, consumers enjoy certain rights when it comes to the use and protection of their credit information. However, unfortunate instances may occur where individuals or organizations misuse or abuse this sensitive data, causing harm to the affected consumers. This article dives into the details of a Guam Complaint by a Consumer against Wrongful Users of Credit Information, shedding light on the possible types of such complaints and the actions consumers can take to seek justice. Types of Guam Complaints by Consumer against Wrongful User of Credit Information: 1. Identity Theft — This type of complaint arises when an individual's personal information, such as Social Security number, name, or address, is fraudulently used without their knowledge or consent, resulting in financial losses or damaged credit. 2. Unauthorized Credit Inquiries — Consumers may file a complaint when credit information is accessed without their permission by entities seeking to evaluate their creditworthiness or for other purposes without a valid reason. 3. Reporting Incorrect Information — A consumer may dispute a complaint against credit information reporting agencies, creditors, or financial institutions that furnish erroneous information. This could negatively impact credit scores, loan approvals, or employment opportunities. 4. Data Breach — In the unfortunate event of a data breach, where consumer credit information in an entity's possession is compromised, individuals affected may raise a complaint against the responsible party for their failure to adequately protect and secure their data. 5. Discriminatory Lending Practices — Consumers may file complaints if they suspect that lenders or financial institutions unlawfully discriminate based on their race, gender, religion, nationality, disability, or other protected characteristics when determining credit eligibility. Steps to Resolution: 1. Gather evidence — Consumers must collect supporting documents such as credit reports, correspondence, bank statements, and any other relevant information related to the complaint. 2. Contact the Guam Consumer Protection Division — Consumers should reach out to the appropriate government agency, such as the Guam Consumer Protection Division, to report the complaint and seek guidance on the necessary steps to follow. 3. File a formal complaint — Depending on the situation, consumers can file complaints with relevant regulatory bodies, law enforcement agencies, or credit bureaus. Providing comprehensive details regarding the wrongful use of credit information is crucial. 4. Cooperate and seek legal advice — Throughout the process, consumers are encouraged to maintain communication and provide any additional information requested by investigating authorities. Seeking legal advice from professionals familiar with consumer protection laws can be beneficial. 5. Seek resolution and compensation — Enforcing privacy rights and holding wrongful users accountable may result in compensation for damages endured by the consumer. Consumers should work towards attaining a satisfactory resolution, which may involve financial remedies, credit repairs, or corrective action taken by the responsible party. Conclusion: Consumers in Guam have the right to protect their credit information from wrongful use and should take appropriate actions by reporting complaints as soon as they discover any irregularities. By following the outlined steps and seeking assistance from the relevant authorities, consumers can work towards resolution, ensuring their credit information is safeguarded, and justice is served.