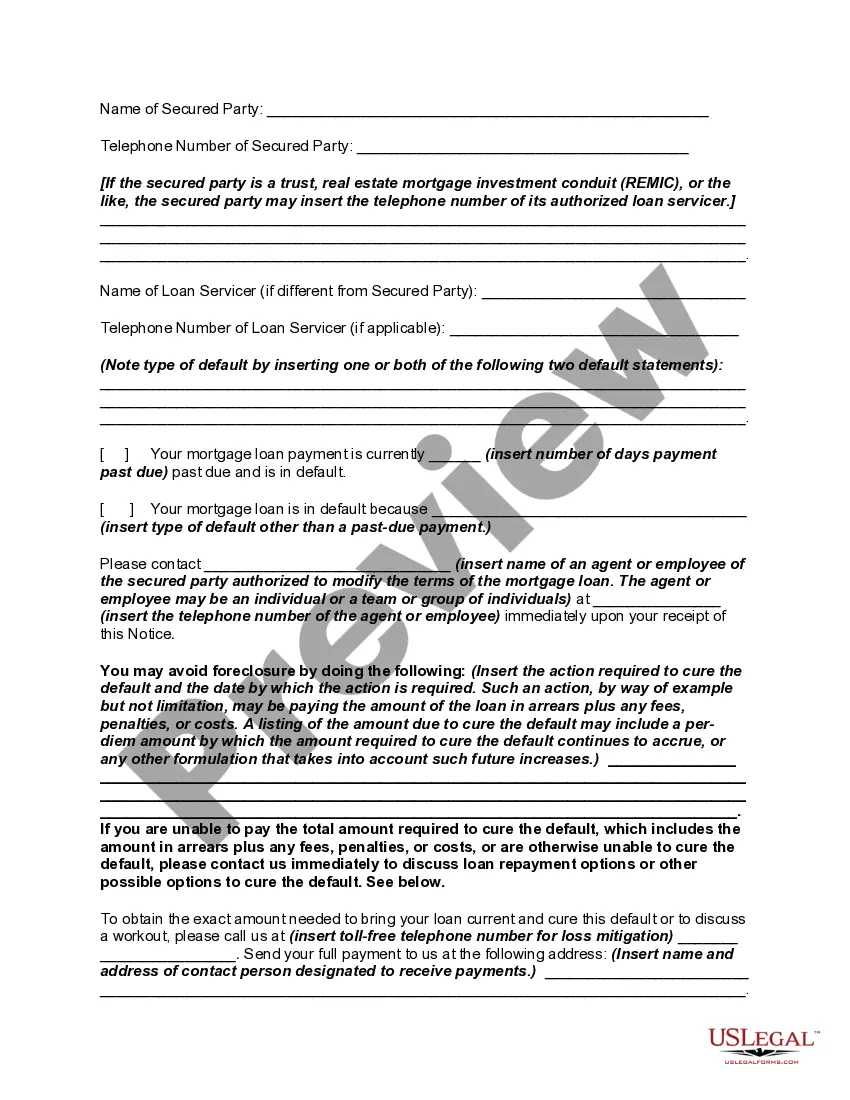

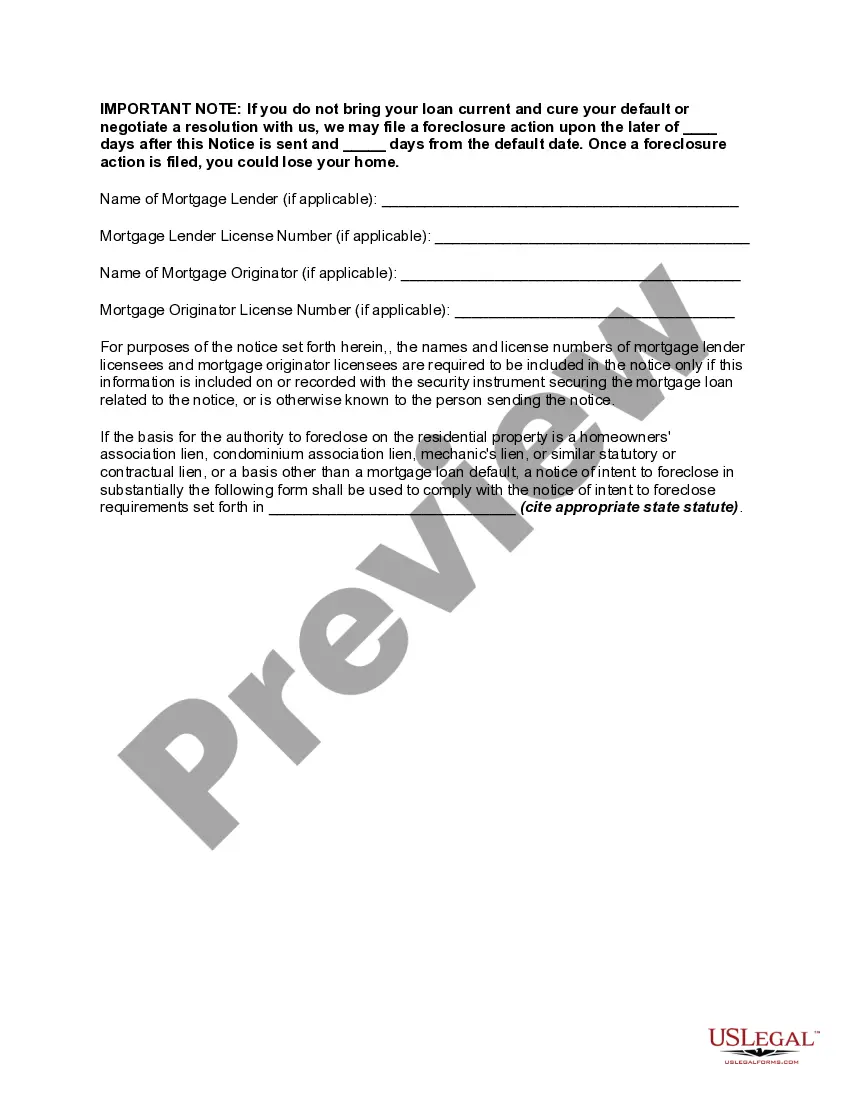

A number of states have enacted measures to facilitate greater communication between borrowers and lenders by requiring mortgage servicers to provide certain notices to defaulted borrowers prior to commencing a foreclosure action. The measures serve a dual purpose, providing more meaningful notice to borrowers of the status of their loans and slowing down the rate of foreclosures within these states. For instance, one state now requires a mortgagee to mail a homeowner a notice of intent to foreclose at least 45 days before initiating a foreclosure action on a loan. The notice must be in writing, and must detail all amounts that are past due and any itemized charges that must be paid to bring the loan current, inform the homeowner that he or she may have options as an alternative to foreclosure, and provide contact information of the servicer, HUD-approved foreclosure counseling agencies, and the state Office of Commissioner of Banks.

Title: Understanding Guam's Notice of Intent to Foreclose — Mortgage Loan Default Introduction: Guam's Notice of Intent to Foreclose — Mortgage Loan Default is a legal document issued by lenders or financial institutions to borrowers who have defaulted on their mortgage loans in Guam. This article aims to provide a detailed description of what this notice entails, its significance, and the possible types of notices that can be issued. 1. Overview: The Notice of Intent to Foreclose is an essential step in the foreclosure process initiated by lenders when borrowers fail to make timely mortgage payments. It serves as a legal warning that the lender intends to foreclose on the property if the borrower does not cure the default within a specific timeframe. 2. Purpose: The primary purpose of this notice is to inform borrowers about their default on the mortgage loan and provide them with an opportunity to take remedial action. It aims to ensure transparency and fairness by notifying borrowers of the consequences they may face if they continue to default on their payments. 3. Key components of the Notice of Intent: a) Borrower's Information: This section includes the borrower's name, contact details, and property address associated with the mortgage loan. b) Lender's Information: It includes the name, contact information, and legal representation (if any) of the mortgage lender or service handling the foreclosure process. c) Default Details: The notice outlines the specific details of the default, such as the outstanding amount, missed payment dates, and any fees or penalties incurred due to non-payment. d) Cure Period: This section specifies the duration within which the borrower must cure the default by making the required payments or reaching a foreclosure avoidance agreement with the lender. e) Consequences of Non-Compliance: The notice clearly states the potential consequences if the borrower fails to cure the default, which may include foreclosure proceedings, loss of property, and damage to creditworthiness. 4. Possible types of Guam Notice of Intent: a) Notice of Intent to Foreclose: Standard notice issued when a borrower fails to make mortgage payments within the specified period. b) Notice of Intent to Accelerate: A more severe notice issued after the previous notice, signaling that the full loan amount has become due and payable, and foreclosure will proceed if not resolved promptly. c) Notice of Intent to Foreclose — Judicial Process: If the lender seeks to foreclose through a judicial process, this notice informs the borrower about the initiation of a legal action and subsequent steps to be taken. d) Notice of Intent to Foreclose — Non-Judicial Process: In cases where non-judicial foreclosure is permissible, this notice informs the borrower about the lender's intention to proceed with the foreclosure without court involvement. Conclusion: Understanding the implications of Guam's Notice of Intent to Foreclose — Mortgage Loan Default is crucial for borrowers to take immediate action to cure their defaults. By familiarizing themselves with the notice's contents, borrowers can explore options to resolve the default and avoid the potential consequences of foreclosure.