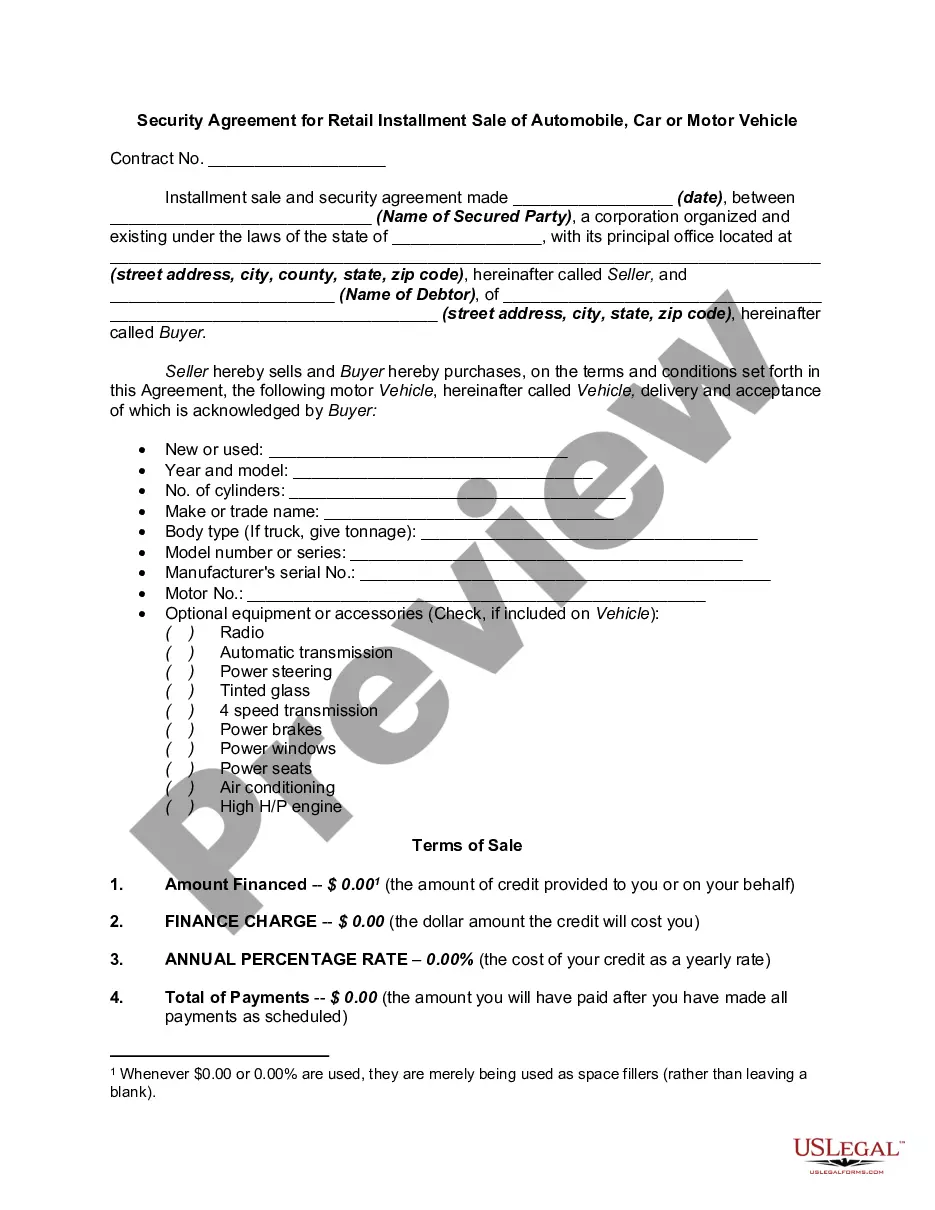

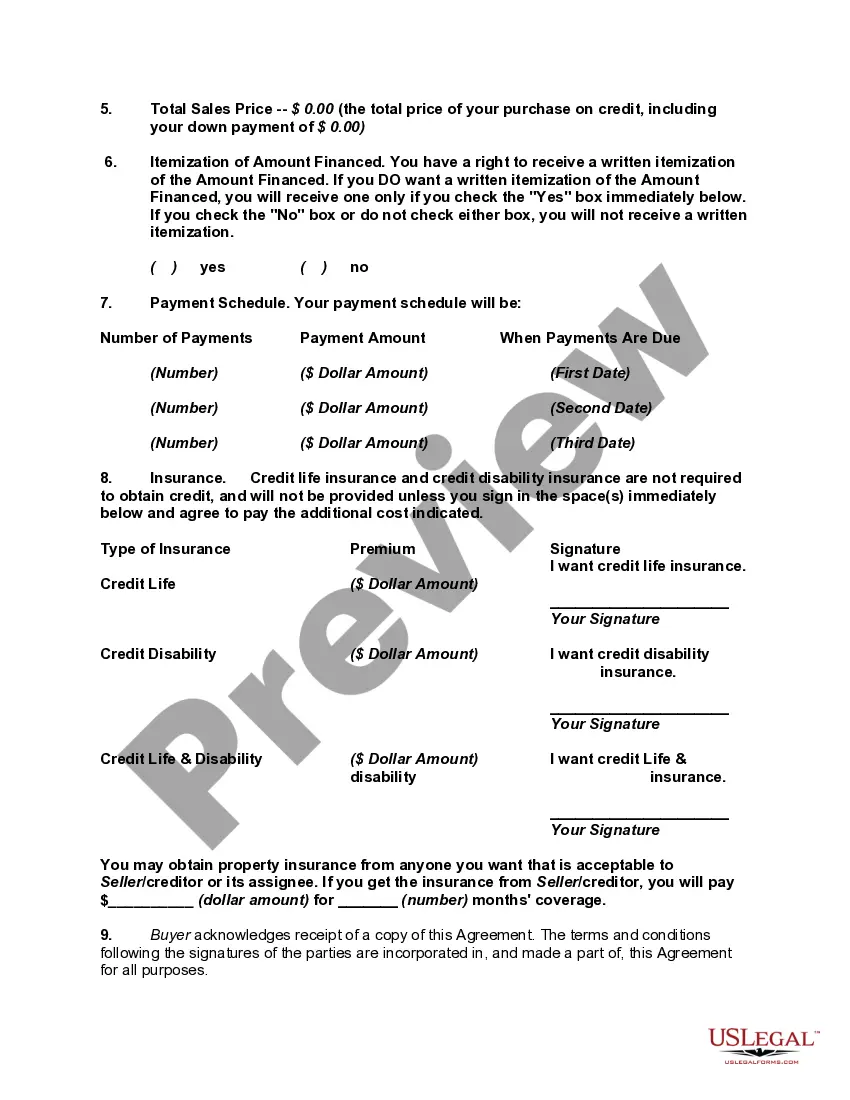

Disclosure of credit terms should have the content and form required under the federal Truth in Lending Act (15 U.S.C.A. §§ 1601 et seq.) and applicable regulations (Regulation Z, 12 C.F.R. § 226), and under state consumer credit laws to the extent that they differ from the federal Act. In connection with specified installment sales and other consumer credit transactions, these enactments require written disclosure and advice as to finance charges, annual percentage rates and other matters relating to credit. Under the federal Act, the disclosures may be set forth in the contract document itself or in a separate statement or statements.

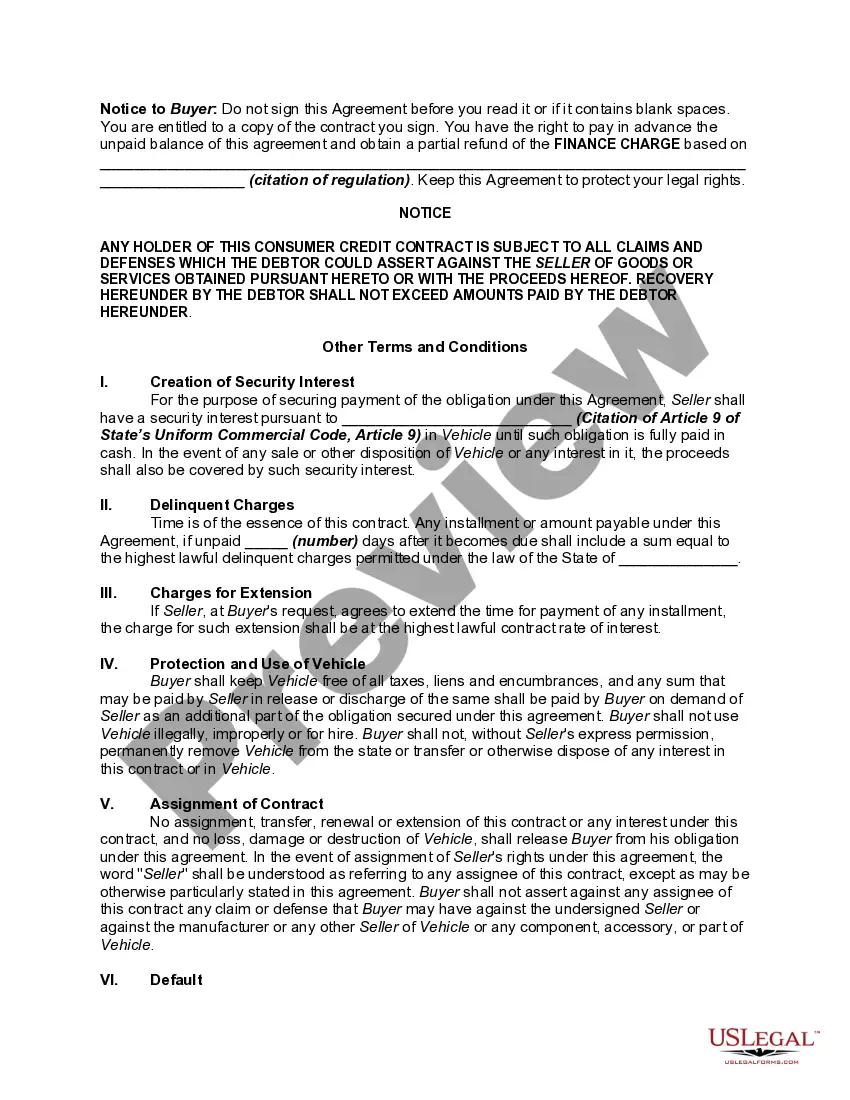

A federal notice regarding preservation of the consumer's claims and defenses is required on all consumer credit contracts by Federal Trade Commission regulation. 16 C.F.R. § 433.2. The notice must appear in 10-point bold type or print and must be worded as set forth in the above form.

The Guam Security Agreement for Retail Installment Sale of Automobile, Car, or Motor Vehicle is a legal document that outlines the terms and conditions for the purchase of a vehicle through a retail installment sale in Guam. This agreement serves as a security measure to protect the interests of both the buyer and the seller. Keywords: Guam, Security Agreement, Retail Installment Sale, Automobile, Car, Motor Vehicle In Guam, there are different types of Security Agreements for Retail Installment Sale of Automobile, Car, or Motor Vehicle, designed to cater to various scenarios and specific types of sales: 1. Standard Retail Installment Sale Agreement: This type of agreement lays out the general terms and conditions for the purchase of a vehicle through a retail installment sale. It includes details such as the buyer's and seller's information, vehicle description, purchase price, down payment, interest rate, payment schedule, and default provisions. 2. Guarantor Security Agreement: In some cases, a guarantor may be required to back the buyer's obligations under the retail installment sale agreement. This type of security agreement specifies the role and responsibilities of the guarantor, ensuring that they will cover any outstanding payments in case the buyer defaults. 3. Negative Equity Security Agreement: Negative equity refers to the situation where the buyer owes more on the vehicle than its current market value. This agreement addresses the buyer's obligation to cover the negative equity, either by making additional payments or rolling it over into a new loan. 4. Co-signer Security Agreement: When a buyer does not meet the credit requirements for a retail installment sale, they may require a co-signer. This security agreement outlines the co-signer's responsibilities, ensuring they will be liable for the debt in case the buyer fails to make payments. 5. Lease Purchase Security Agreement: A lease purchase agreement is a hybrid contract where the buyer leases the vehicle for a certain period with an option to purchase at the end. The security agreement in this scenario ensures that the buyer follows the terms of the lease and has the right to purchase the vehicle at the agreed price. These different types of security agreements ensure that all parties involved are protected and obligations are clearly defined in the event of default or non-compliance. It is crucial for both buyers and sellers to understand and carefully review the terms of the agreement before entering into a retail installment sale of an automobile, car, or motor vehicle in Guam.