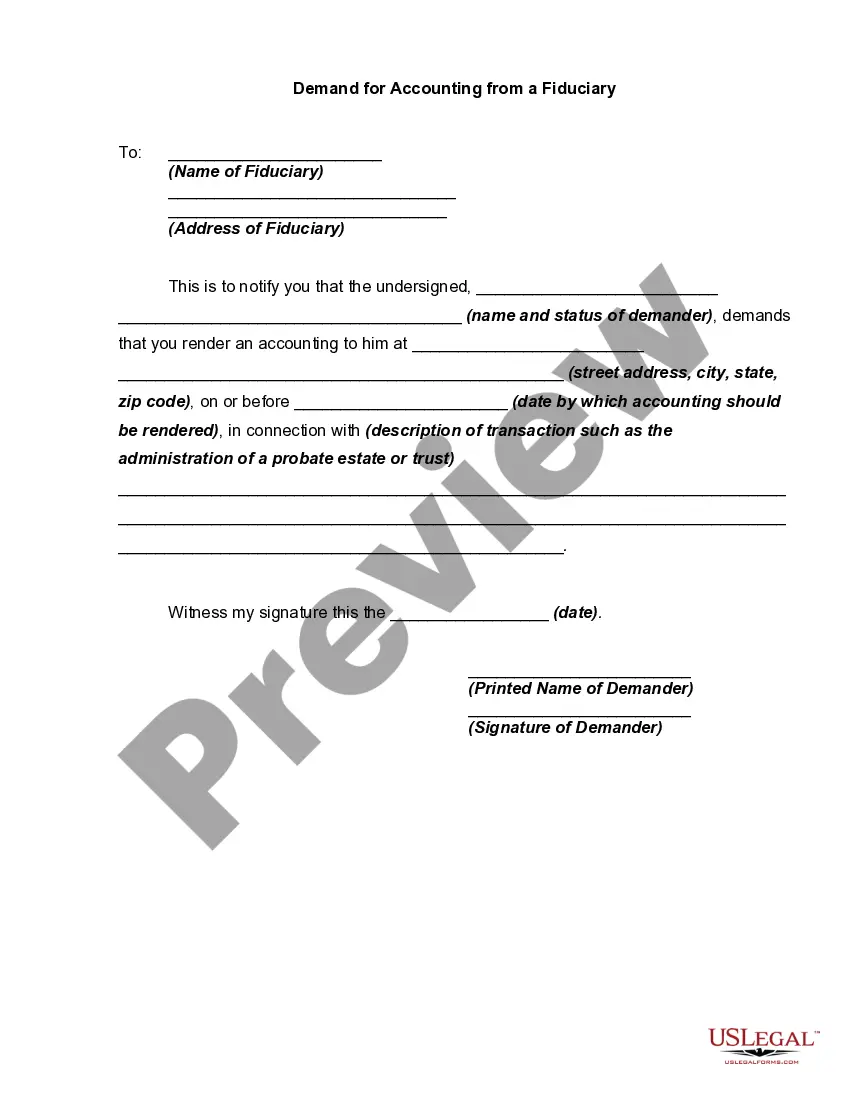

Sometimes, a prior demand by a potential plaintiff for an accounting, and a refusal by the fiduciary to account, are conditions precedent to the bringing of an action for an accounting. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Title: Understanding Guam Demand for Accounting from a Fiduciary: Exploring Types and Key Considerations Introduction: In the paradigm of fiduciary relationships, where a person or entity is entrusted to manage the affairs or assets of another, Guam Demand for Accounting from a Fiduciary plays a crucial role in maintaining transparency and accountability. This article aims to provide a detailed description of what Guam Demand for Accounting entails, including different types and factors to consider. 1. What is Guam Demand for Accounting from a Fiduciary? Guam Demand for Accounting refers to the legal right of a beneficiary or interested party to request a fiduciary to provide comprehensive, accurate, and transparent financial records and reports concerning the management of assets or affairs. It serves as a safeguard to prevent potential mismanagement, fraud, or other violations of fiduciary duty. 2. Types of Guam Demand for Accounting from a Fiduciary: a) Trust Accounting: Within trust agreements, beneficiaries possess the right to request an accounting of all trust activities, including transactions, asset values, income, expenses, and distributions. Trust accounting is vital, especially in complex and long-term trusts, to ensure adherence to the trust's terms and the fiduciary's obligations. b) Estate Accounting: In estate administration, beneficiaries of an estate can demand an accounting from the fiduciary, typically the executor or personal representative. Estate accounting involves a thorough examination of the estate's financial activities, including assets, debts, income, expenses, taxes, and distributions to heirs. c) Guardianship Accounting: Guardianship accounting primarily relates to minors, individuals with disabilities, or incapacitated adults under guardianship. Interested parties, including family members or court-appointed representatives, have the right to scrutinize the fiduciary's management of the ward's financial resources, ensuring responsible and ethical handling. 3. Key Considerations for Demand for Accounting from a Fiduciary in Guam: a) Legal Grounds: To request accounting, interested parties must establish a legal basis, such as beneficiary status, legal representation, or court orders authorizing accounting. Understanding the applicable Guam laws regarding fiduciary obligations and rights is essential. b) Timelines and Frequency: Guam demand for accounting may include specific timelines within which the fiduciary must comply. Beneficiaries should familiarize themselves with these deadlines and any provisions concerning the frequency of accounting reports. c) Scope of Accounting: Beneficiaries should understand the extent of the accounting, including the level of detail required, the type of records to be produced, and the format in which the information will be provided. Clarity here aids in obtaining the desired level of transparency. d) Professional Assistance: Beneficiaries may consider engaging an experienced attorney or accountant to help them navigate the complexities of demand for accounting, ensuring their rightful access to accurate financial information. Conclusion: In Guam, demand for accounting from a fiduciary provides essential protection for beneficiaries and interested parties. Trust accounting, estate accounting, and guardianship accounting represent key types that cater to different fiduciary relationships. Observing legal prerequisites, understanding timelines and scope, and seeking professional assistance can significantly enhance the effectiveness of Guam demand for accounting processes. By upholding transparency and accountability, the demand for accounting safeguards the rights and interests of individuals involved in fiduciary arrangements.Title: Understanding Guam Demand for Accounting from a Fiduciary: Exploring Types and Key Considerations Introduction: In the paradigm of fiduciary relationships, where a person or entity is entrusted to manage the affairs or assets of another, Guam Demand for Accounting from a Fiduciary plays a crucial role in maintaining transparency and accountability. This article aims to provide a detailed description of what Guam Demand for Accounting entails, including different types and factors to consider. 1. What is Guam Demand for Accounting from a Fiduciary? Guam Demand for Accounting refers to the legal right of a beneficiary or interested party to request a fiduciary to provide comprehensive, accurate, and transparent financial records and reports concerning the management of assets or affairs. It serves as a safeguard to prevent potential mismanagement, fraud, or other violations of fiduciary duty. 2. Types of Guam Demand for Accounting from a Fiduciary: a) Trust Accounting: Within trust agreements, beneficiaries possess the right to request an accounting of all trust activities, including transactions, asset values, income, expenses, and distributions. Trust accounting is vital, especially in complex and long-term trusts, to ensure adherence to the trust's terms and the fiduciary's obligations. b) Estate Accounting: In estate administration, beneficiaries of an estate can demand an accounting from the fiduciary, typically the executor or personal representative. Estate accounting involves a thorough examination of the estate's financial activities, including assets, debts, income, expenses, taxes, and distributions to heirs. c) Guardianship Accounting: Guardianship accounting primarily relates to minors, individuals with disabilities, or incapacitated adults under guardianship. Interested parties, including family members or court-appointed representatives, have the right to scrutinize the fiduciary's management of the ward's financial resources, ensuring responsible and ethical handling. 3. Key Considerations for Demand for Accounting from a Fiduciary in Guam: a) Legal Grounds: To request accounting, interested parties must establish a legal basis, such as beneficiary status, legal representation, or court orders authorizing accounting. Understanding the applicable Guam laws regarding fiduciary obligations and rights is essential. b) Timelines and Frequency: Guam demand for accounting may include specific timelines within which the fiduciary must comply. Beneficiaries should familiarize themselves with these deadlines and any provisions concerning the frequency of accounting reports. c) Scope of Accounting: Beneficiaries should understand the extent of the accounting, including the level of detail required, the type of records to be produced, and the format in which the information will be provided. Clarity here aids in obtaining the desired level of transparency. d) Professional Assistance: Beneficiaries may consider engaging an experienced attorney or accountant to help them navigate the complexities of demand for accounting, ensuring their rightful access to accurate financial information. Conclusion: In Guam, demand for accounting from a fiduciary provides essential protection for beneficiaries and interested parties. Trust accounting, estate accounting, and guardianship accounting represent key types that cater to different fiduciary relationships. Observing legal prerequisites, understanding timelines and scope, and seeking professional assistance can significantly enhance the effectiveness of Guam demand for accounting processes. By upholding transparency and accountability, the demand for accounting safeguards the rights and interests of individuals involved in fiduciary arrangements.