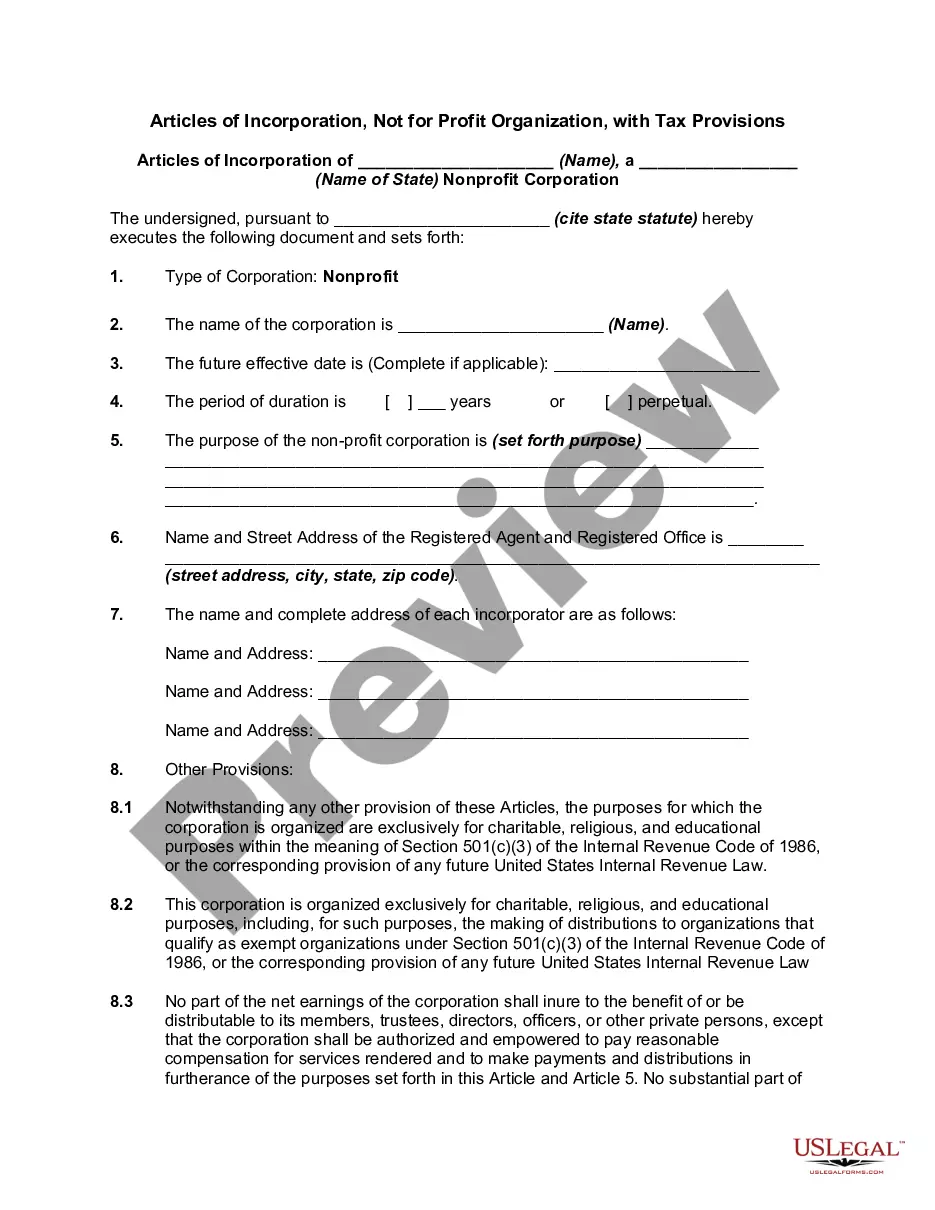

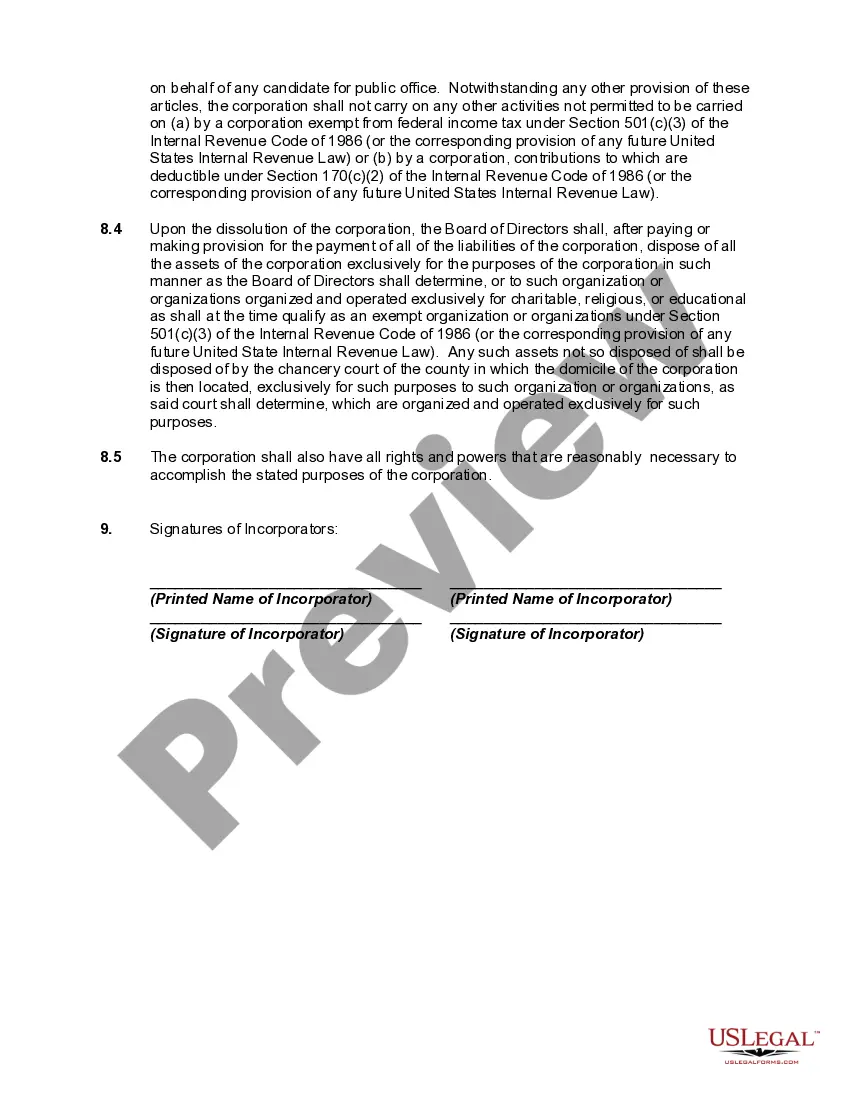

Guam Articles of Incorporation, Not for Profit Organization, with Tax Provisions: The Guam Articles of Incorporation for Not-for-Profit Organizations with Tax Provisions are legal documents that outline the establishment and functioning of a non-profit organization in Guam, a U.S. territory located in the Western Pacific Ocean. These articles serve as the foundation for the organization and its operation, providing important details about its mission, structure, governance, and tax-related obligations. Keywords: Guam, Articles of Incorporation, Not for Profit Organization, Tax Provisions, non-profit organization, mission, structure, governance, tax-related obligations. Types of Guam Articles of Incorporation, Not for Profit Organization, with Tax Provisions: 1. Regular Articles of Incorporation for Not-for-Profit Organizations: These articles are applicable to non-profit organizations that aim to carry out activities for the betterment of society without any revenue generation motive. They outline the organization's purpose, membership structure, governance, and tax provisions following Guam's laws. 2. Articles of Incorporation for Charitable Organizations: These articles specifically cater to non-profit organizations that primarily focus on charitable activities, such as providing assistance to the needy, advancing education, promoting health, or relieving poverty. The articles highlight the organization's charitable purpose and its compliance with Guam's legal requirements for tax-exempt status. 3. Articles of Incorporation for Public Benefit Organizations: These articles are designed for non-profit organizations committed to serving the public interest in areas such as arts, sciences, education, or the environment. They emphasize the organization's purpose, activities, and adherence to Guam's tax provisions to ensure the organization's smooth operation while serving the public benefit. 4. Articles of Incorporation for Religious Organizations: These articles cater to non-profit organizations formed for religious or faith-based purposes. They address specific considerations related to religious practice and worship while also including provisions for tax-exempt status, allowing these organizations to fulfill their spiritual mission while complying with Guam's legal requirements. 5. Articles of Incorporation for Membership Organizations: These articles are tailored for non-profit organizations that operate on a membership basis, such as trade associations, professional societies, or co-operative societies. Along with outlining the organization's purpose, governance, and tax provisions, these articles also detail the membership structure and rights, ensuring transparency and accountability within the organization. In conclusion, the Guam Articles of Incorporation for Not-for-Profit Organizations with Tax Provisions provide a legal framework for establishing and operating various types of non-profit organizations in Guam. These articles ensure compliance with tax laws while preserving the organization's mission and purpose, fostering their positive contributions to the community.

Guam Articles of Incorporation, Not for Profit Organization, with Tax Provisions

Description

How to fill out Guam Articles Of Incorporation, Not For Profit Organization, With Tax Provisions?

US Legal Forms - among the greatest libraries of legal types in America - provides an array of legal papers themes it is possible to down load or print out. Making use of the web site, you can find thousands of types for business and person functions, sorted by classes, states, or keywords and phrases.You will discover the latest versions of types like the Guam Articles of Incorporation, Not for Profit Organization, with Tax Provisions within minutes.

If you have a monthly subscription, log in and down load Guam Articles of Incorporation, Not for Profit Organization, with Tax Provisions through the US Legal Forms local library. The Download button will show up on each and every kind you see. You get access to all earlier acquired types in the My Forms tab of your own profile.

If you want to use US Legal Forms initially, here are easy directions to help you get started out:

- Be sure to have chosen the correct kind for your town/area. Select the Preview button to review the form`s content material. See the kind outline to ensure that you have selected the correct kind.

- When the kind doesn`t satisfy your needs, make use of the Look for industry on top of the display to discover the one who does.

- When you are pleased with the shape, validate your choice by simply clicking the Acquire now button. Then, opt for the costs plan you like and give your credentials to sign up for an profile.

- Method the deal. Use your Visa or Mastercard or PayPal profile to complete the deal.

- Find the formatting and down load the shape on your own device.

- Make adjustments. Fill up, change and print out and indicator the acquired Guam Articles of Incorporation, Not for Profit Organization, with Tax Provisions.

Each template you put into your bank account lacks an expiry particular date and it is the one you have eternally. So, if you want to down load or print out yet another duplicate, just check out the My Forms segment and click around the kind you require.

Obtain access to the Guam Articles of Incorporation, Not for Profit Organization, with Tax Provisions with US Legal Forms, probably the most substantial local library of legal papers themes. Use thousands of expert and status-distinct themes that meet your small business or person requires and needs.