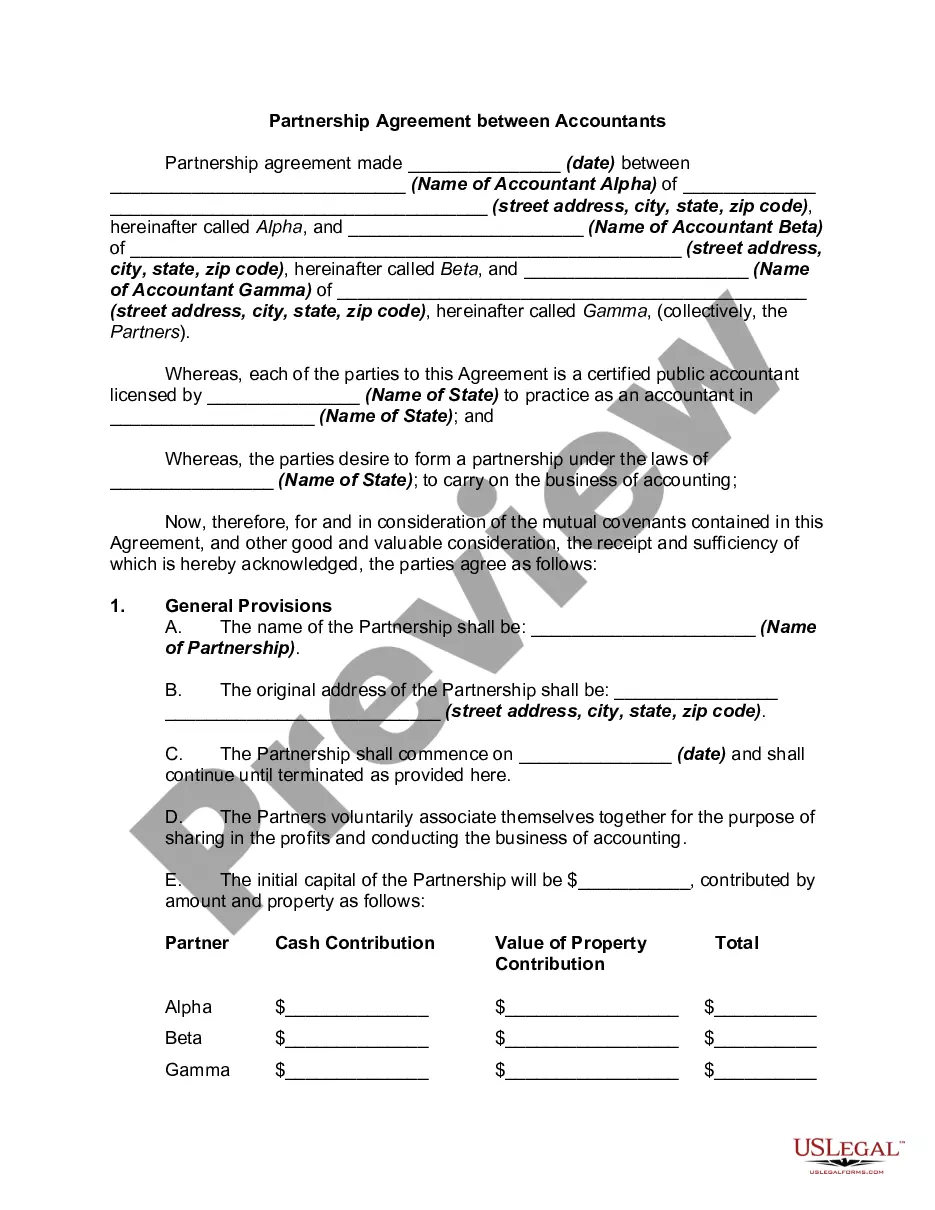

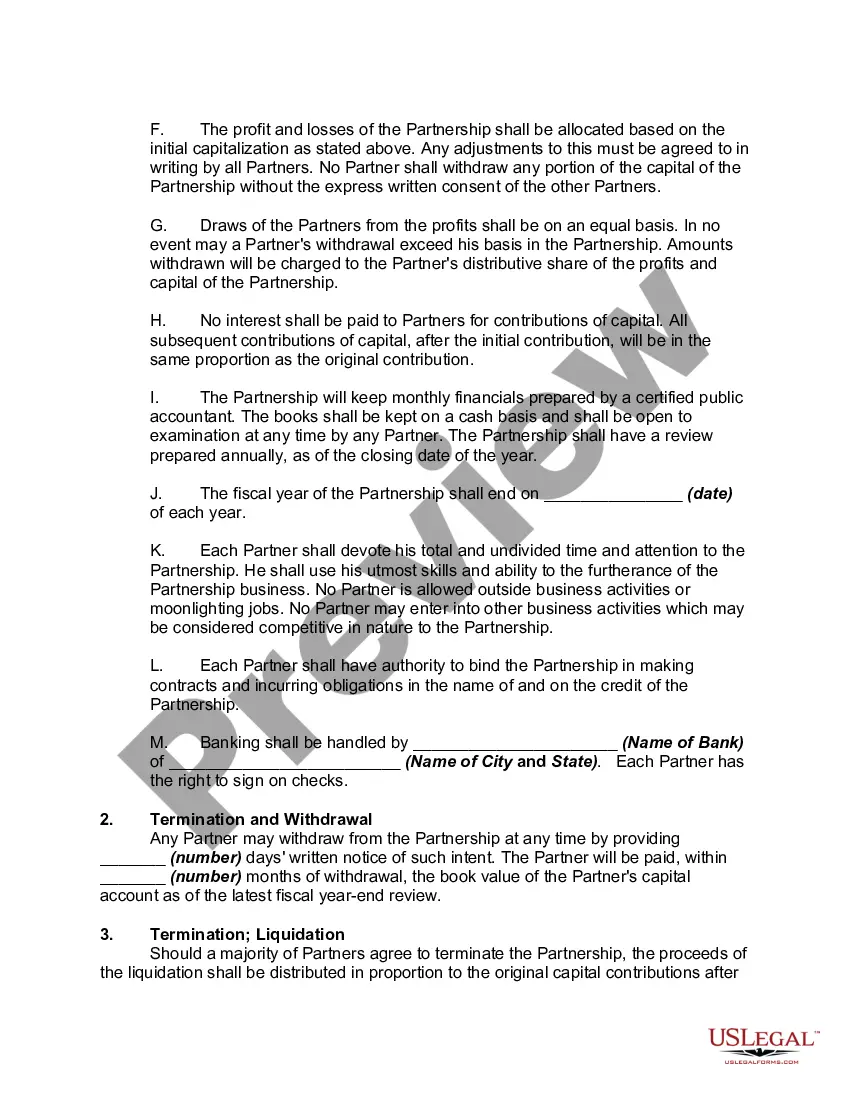

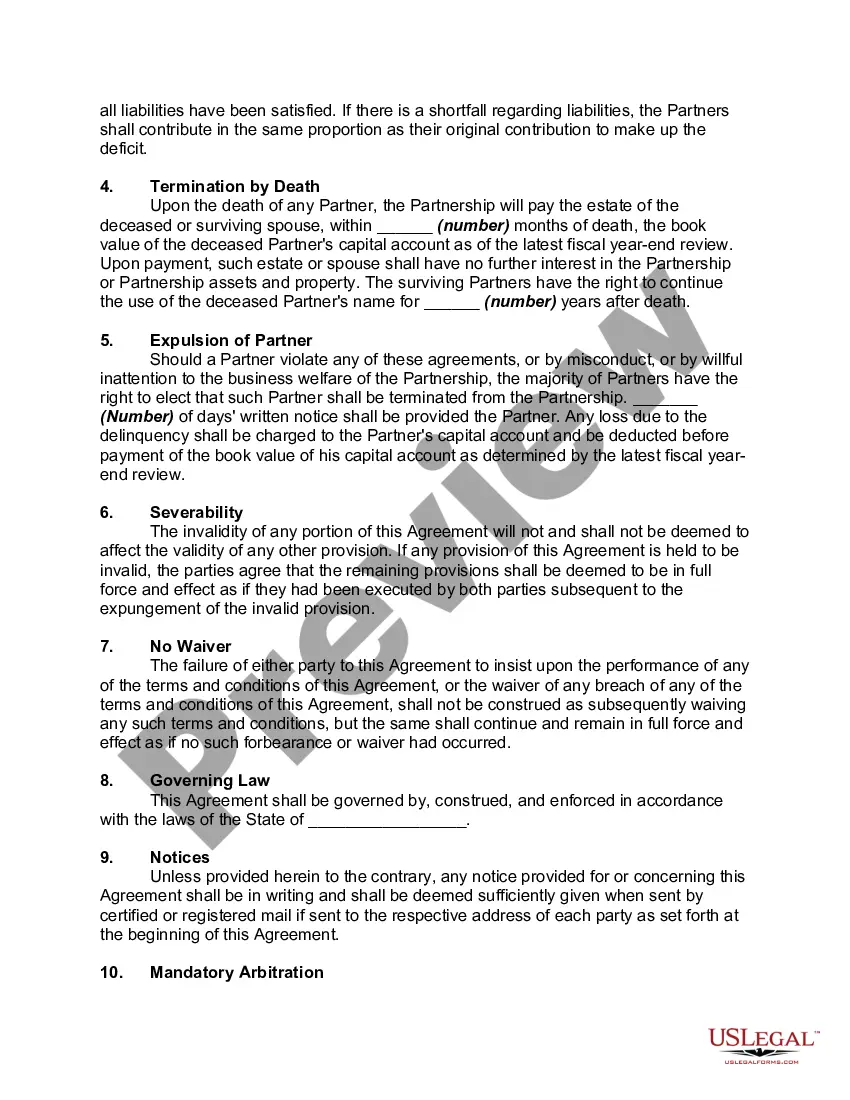

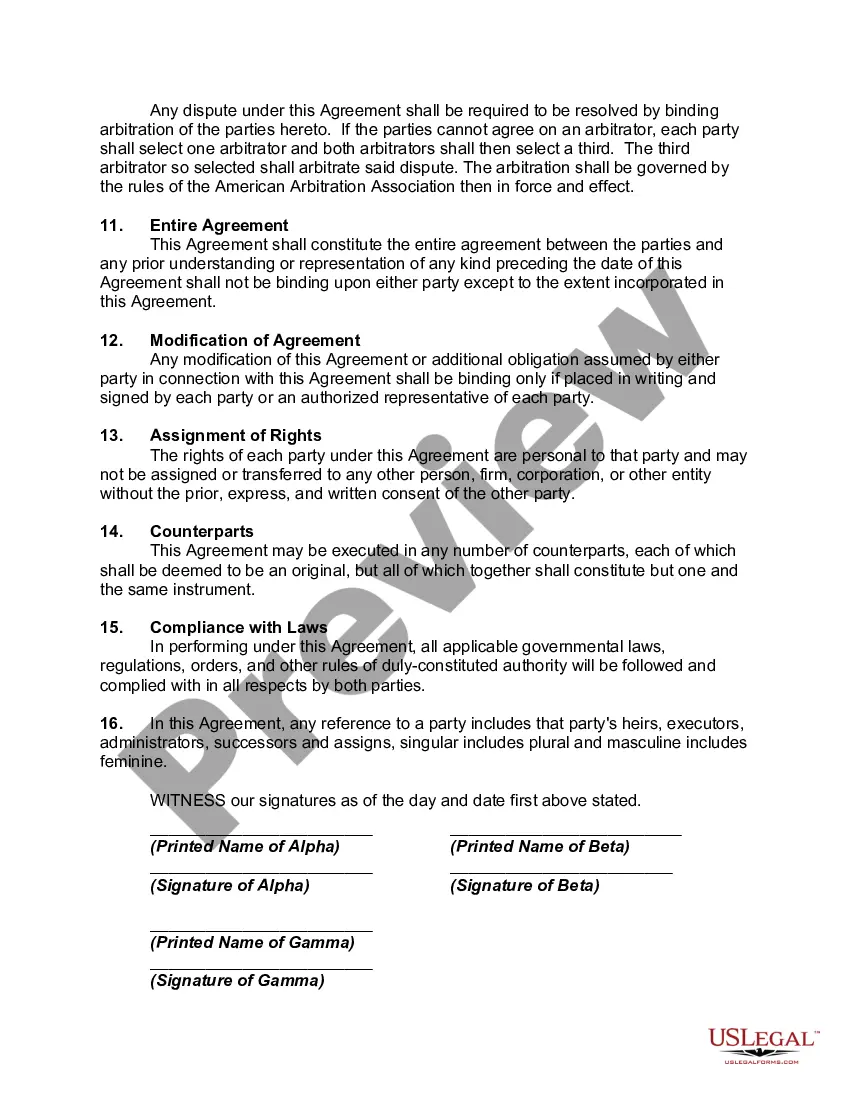

Partnership agreements are written documents that explicitly detail the relationship between the business partners and their individual obligations and contributions to the partnership. Since partnership agreements should cover all possible business situations that could arise during the partnership's life, the documents are often complex; legal counsel in drafting and reviewing the finished contract is generally recommended. If a partnership does not have a partnership agreement in place when it dissolves, the guidelines of the Uniform Partnership Act and various state laws will determine how the assets and debts of the partnership are distributed.

A Guam Partnership Agreement Between Accountants is a legally binding document that outlines the terms and conditions agreed upon by two or more accountants operating in Guam. This agreement serves as a framework for their partnership, guiding their professional relationship, and clarifying their roles, responsibilities, and financial arrangements. One primary type of Guam Partnership Agreement Between Accountants is the General Partnership Agreement. In this arrangement, two or more accountants come together to form a partnership, pooling their resources, skills, and expertise to provide accounting services in Guam. They share both the profits and liabilities of the partnership equally, unless specified otherwise in the agreement. Another variation is the Limited Partnership Agreement. This type of partnership involves one or more general partners who take on full responsibility for the partnership, while one or more limited partners contribute capital but have limited liability. Limited partners mainly invest in the partnership and are not actively involved in its day-to-day operations. A Guam Partnership Agreement Between Accountants typically includes several key provisions: 1. Partnership Name and Duration: It states the agreed-upon name of the partnership and specifies the duration for which the partnership will exist. This can be for a specific project or indefinitely. 2. Purpose and Scope: This section defines the scope of the partnership's activities and the services it intends to provide. It outlines the specific accounting services and areas of expertise the partnership will focus on. 3. Capital Contributions: The agreement details how much capital each partner will contribute to the partnership. It may specify both initial contributions and ongoing capital requirements. 4. Profit and Loss Distribution: This section outlines how profits and losses will be distributed among the partners. It can be equal for general partnerships or based on a pre-determined percentage for limited partnerships. 5. Decision-Making and Management: The agreement defines how decisions will be made within the partnership, whether it is through consensus, voting rights, or by designating one partner as the managing partner with broader decision-making authority. 6. Partner Roles and Responsibilities: It clearly outlines the roles and responsibilities of each partner, ensuring that all partners understand their duties and obligations. This section may also define the expected time commitment and any restrictions on competing activities. 7. Dispute Resolution: This provision outlines the procedures partners will follow to resolve conflicts or disagreements that may arise during the partnership. It may include mediation, arbitration, or other alternative dispute resolution methods. 8. Termination and Dissolution: This section explains the circumstances under which the partnership can be terminated or dissolved, including events such as retirement, death, bankruptcy, or the voluntary withdrawal of a partner. It also outlines the procedures for winding up the partnership's affairs and distributing assets. A Guam Partnership Agreement Between Accountants is a crucial document that provides a clear framework for accountants partnering together to offer their services in Guam. It establishes the rights, responsibilities, and expectations of each partner, ensuring a harmonious and successful professional collaboration.A Guam Partnership Agreement Between Accountants is a legally binding document that outlines the terms and conditions agreed upon by two or more accountants operating in Guam. This agreement serves as a framework for their partnership, guiding their professional relationship, and clarifying their roles, responsibilities, and financial arrangements. One primary type of Guam Partnership Agreement Between Accountants is the General Partnership Agreement. In this arrangement, two or more accountants come together to form a partnership, pooling their resources, skills, and expertise to provide accounting services in Guam. They share both the profits and liabilities of the partnership equally, unless specified otherwise in the agreement. Another variation is the Limited Partnership Agreement. This type of partnership involves one or more general partners who take on full responsibility for the partnership, while one or more limited partners contribute capital but have limited liability. Limited partners mainly invest in the partnership and are not actively involved in its day-to-day operations. A Guam Partnership Agreement Between Accountants typically includes several key provisions: 1. Partnership Name and Duration: It states the agreed-upon name of the partnership and specifies the duration for which the partnership will exist. This can be for a specific project or indefinitely. 2. Purpose and Scope: This section defines the scope of the partnership's activities and the services it intends to provide. It outlines the specific accounting services and areas of expertise the partnership will focus on. 3. Capital Contributions: The agreement details how much capital each partner will contribute to the partnership. It may specify both initial contributions and ongoing capital requirements. 4. Profit and Loss Distribution: This section outlines how profits and losses will be distributed among the partners. It can be equal for general partnerships or based on a pre-determined percentage for limited partnerships. 5. Decision-Making and Management: The agreement defines how decisions will be made within the partnership, whether it is through consensus, voting rights, or by designating one partner as the managing partner with broader decision-making authority. 6. Partner Roles and Responsibilities: It clearly outlines the roles and responsibilities of each partner, ensuring that all partners understand their duties and obligations. This section may also define the expected time commitment and any restrictions on competing activities. 7. Dispute Resolution: This provision outlines the procedures partners will follow to resolve conflicts or disagreements that may arise during the partnership. It may include mediation, arbitration, or other alternative dispute resolution methods. 8. Termination and Dissolution: This section explains the circumstances under which the partnership can be terminated or dissolved, including events such as retirement, death, bankruptcy, or the voluntary withdrawal of a partner. It also outlines the procedures for winding up the partnership's affairs and distributing assets. A Guam Partnership Agreement Between Accountants is a crucial document that provides a clear framework for accountants partnering together to offer their services in Guam. It establishes the rights, responsibilities, and expectations of each partner, ensuring a harmonious and successful professional collaboration.