Guam Surety Agreement

Description

How to fill out Surety Agreement?

You can spend hours online searching for the legal document template that satisfies the federal and state requirements you need.

US Legal Forms offers a vast array of legal forms that can be reviewed by experts.

You can conveniently download or print the Guam Surety Agreement from my services.

If available, utilize the Review button to examine the document template as well.

- If you already have a US Legal Forms account, you can Log In and click the Download button.

- After that, you can complete, modify, print, or sign the Guam Surety Agreement.

- Each legal document template you obtain is yours permanently.

- To get another copy of any purchased form, go to the My documents tab and click the appropriate button.

- If you're using the US Legal Forms site for the first time, follow the simple instructions below.

- First, ensure you have selected the correct document template for your area/city of choice.

- Read the form description to ensure you have chosen the correct type.

Form popularity

FAQ

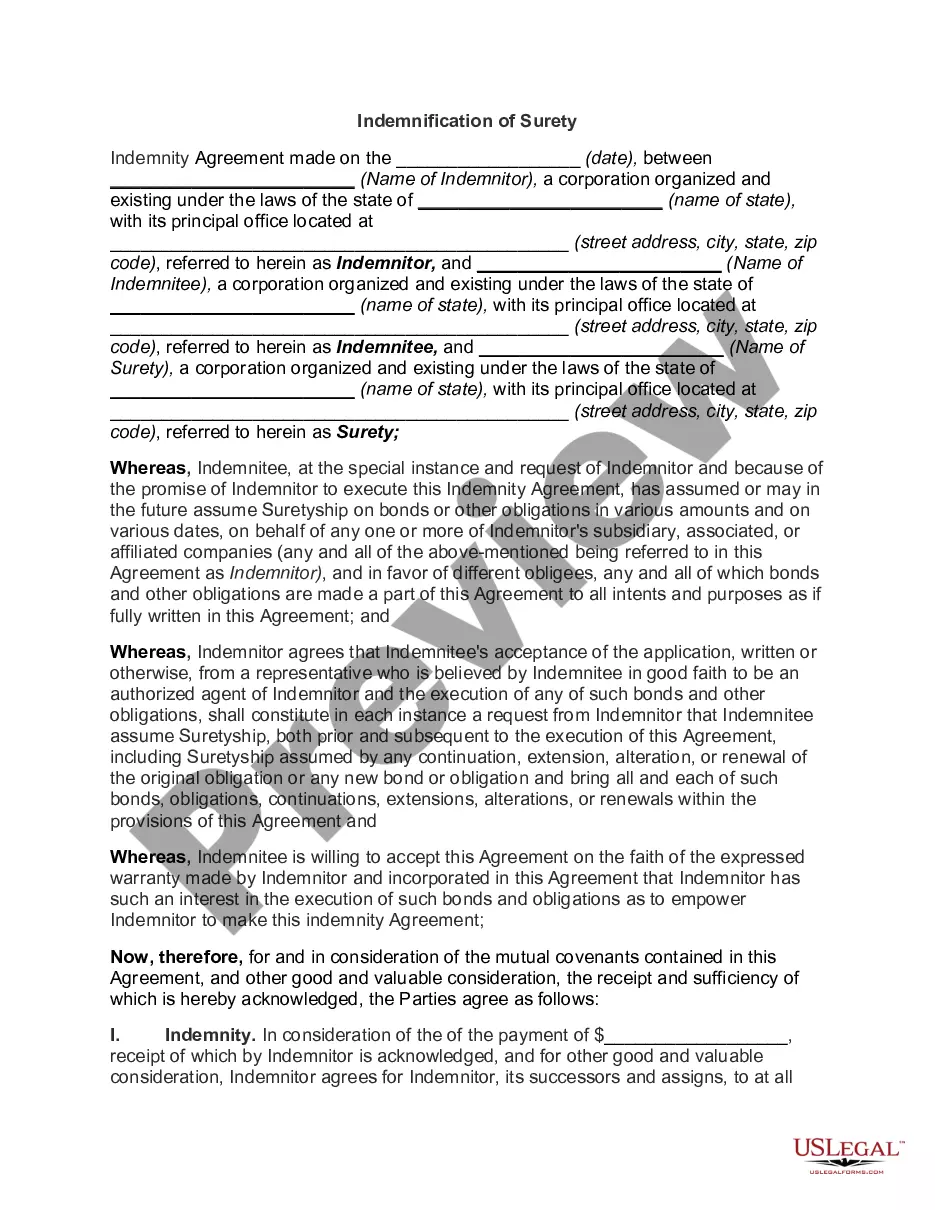

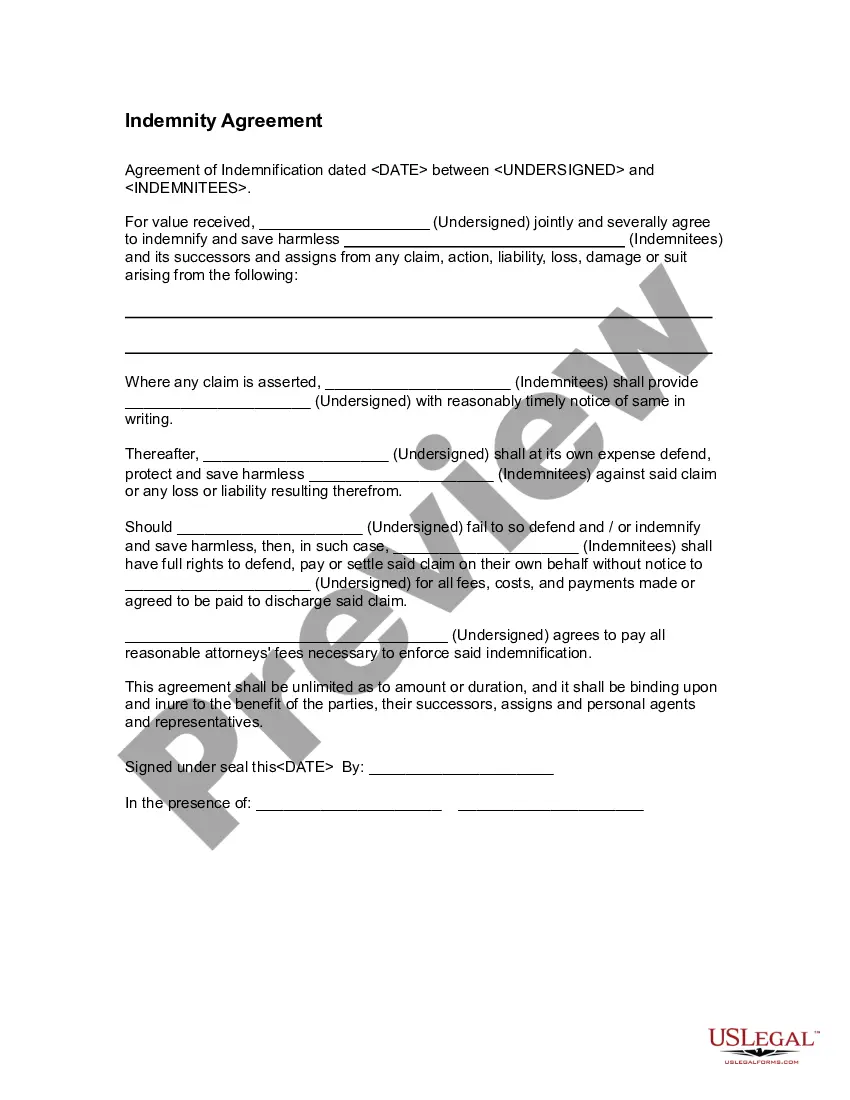

The surety is the guarantee of the debts of one party by another. A surety is an organization or person that assumes the responsibility of paying the debt in case the debtor policy defaults or is unable to make the payments. The party that guarantees the debt is referred to as the surety, or as the guarantor.

A: Surety bonds provide financial guarantees that contracts and other business deals will be completed according to mutual terms. Surety bonds protect consumers and government entities from fraud and malpractice. When a principal breaks a bond's terms, the harmed party can make a claim on the bond to recover losses.

Federal Bonds are surety bonds that are required by federal government agencies such as the Internal Revenue Service (IRS), the Alcohol and Tobacco Tax and Trade Bureau (TTB), the U.S. Customs and Border Protection (CBP) and the Federal Motor Carrier Safety Administration (FMCSA) among others.

Someone who assumes direct liability for another's obligation. Financial creditors may require the debtor to find a surety, who then signs the loan agreement along with the debtor.

The three most common types of contract surety bonds are bid bonds, performance bonds, and payment bonds. Bid bonds require that contractors enter into a contract if their bid for a project has been accepted by the obligee.

Definition of surety 1 : the state of being sure: such as. a : sure knowledge : certainty. b : confidence in manner or behavior : assurance.

A surety bond is defined as a three-party agreement that legally binds together a principal who needs the bond, an obligee who requires the bond and a surety company that sells the bond. The bond guarantees the principal will act in accordance with certain laws.

What is a surety bond indemnity agreement? When you obtain a surety bond, it constitutes a contract between three parties. The principal is either you or your business entity, the party that requires you to get bonded is the obligee, and the surety is the underwriter of the bond.

Usually renewal time is one year after purchasing your bond, but depending on the bond type and bond term, your bond might not renew for 2 or 3 years. Some bonds do not renew at all. In some cases, you can get a lower rate for your bond at renewal.

These bond types are also referred to as commercial bonds" or business bonds." Examples of license and permit surety bonds include auto dealer bonds, mortgage broker bonds, and collection agency bonds.