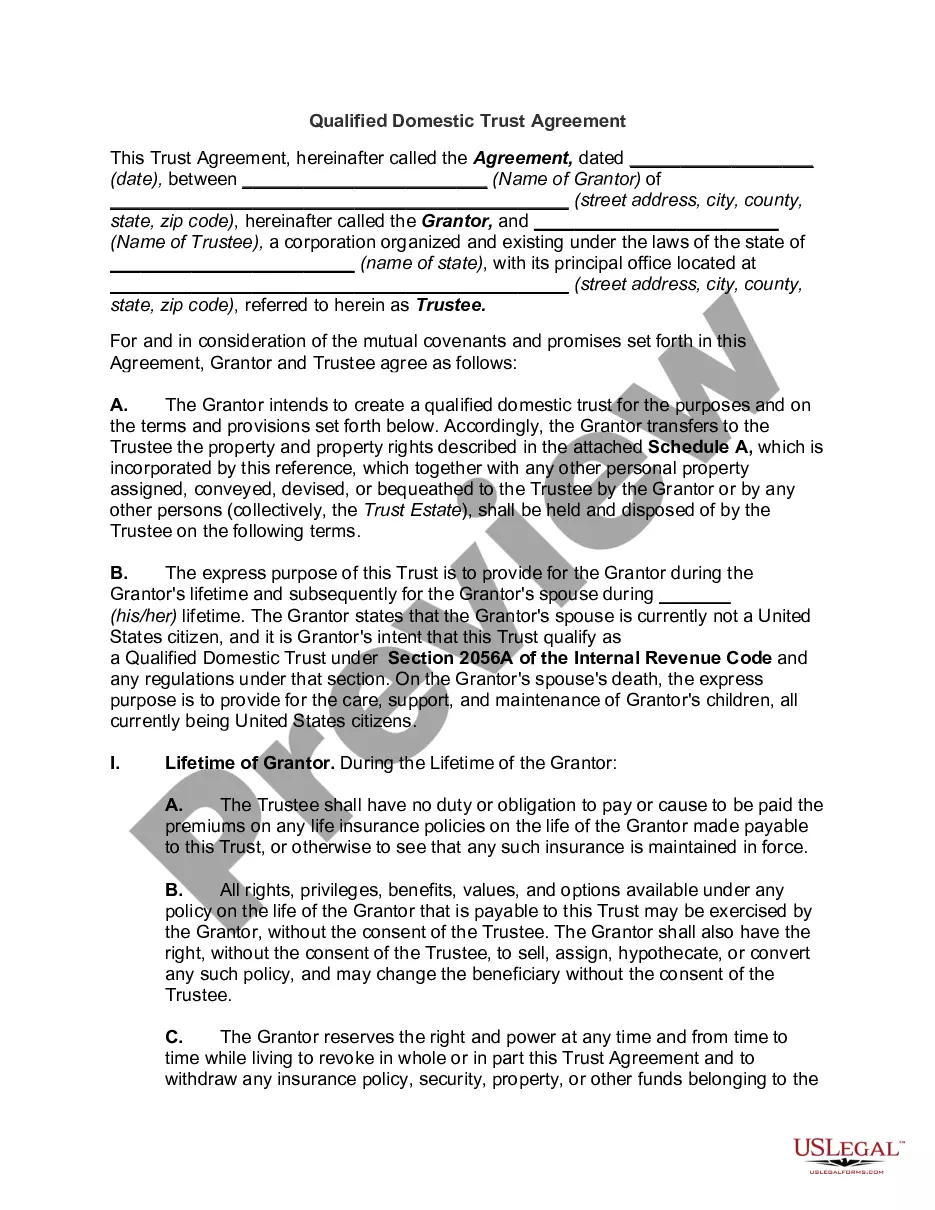

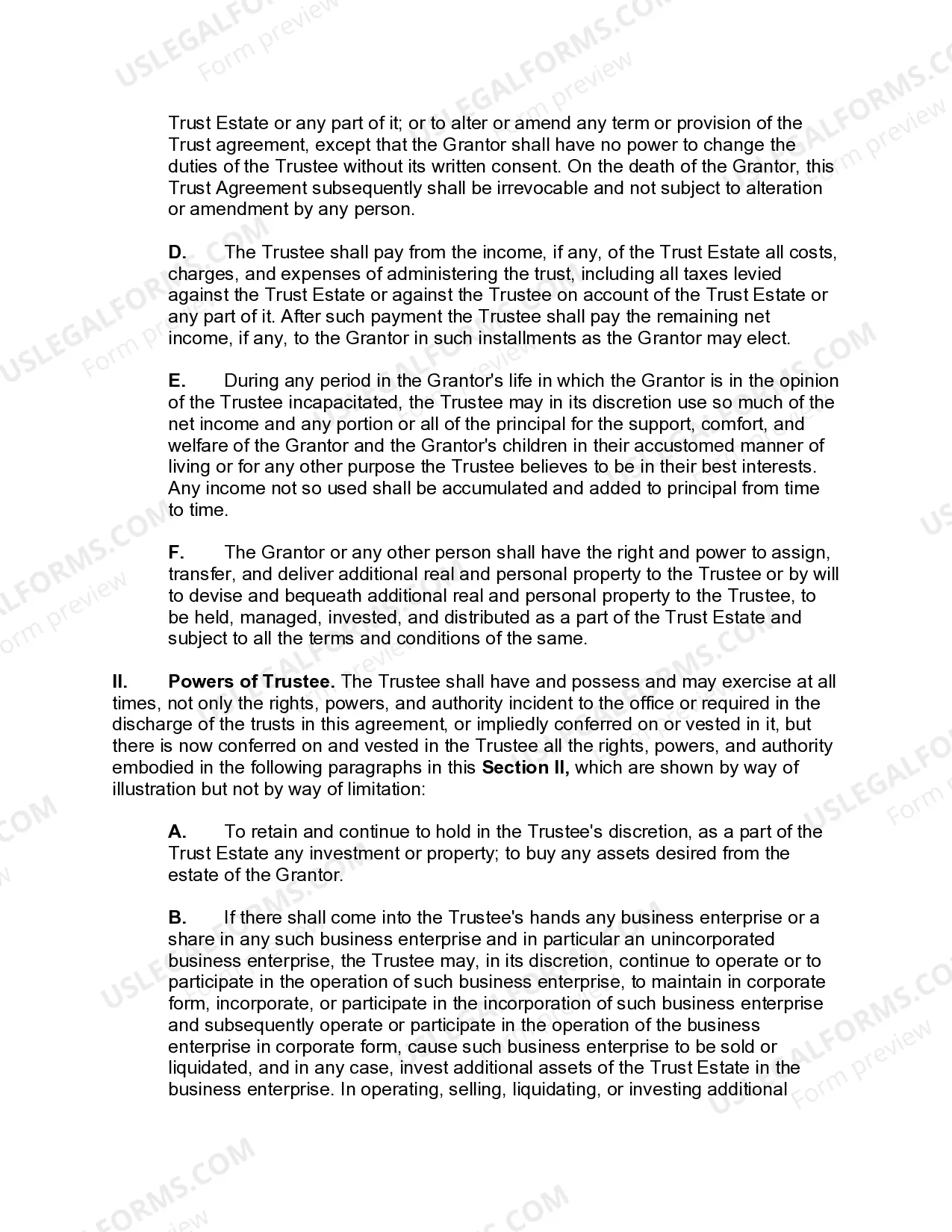

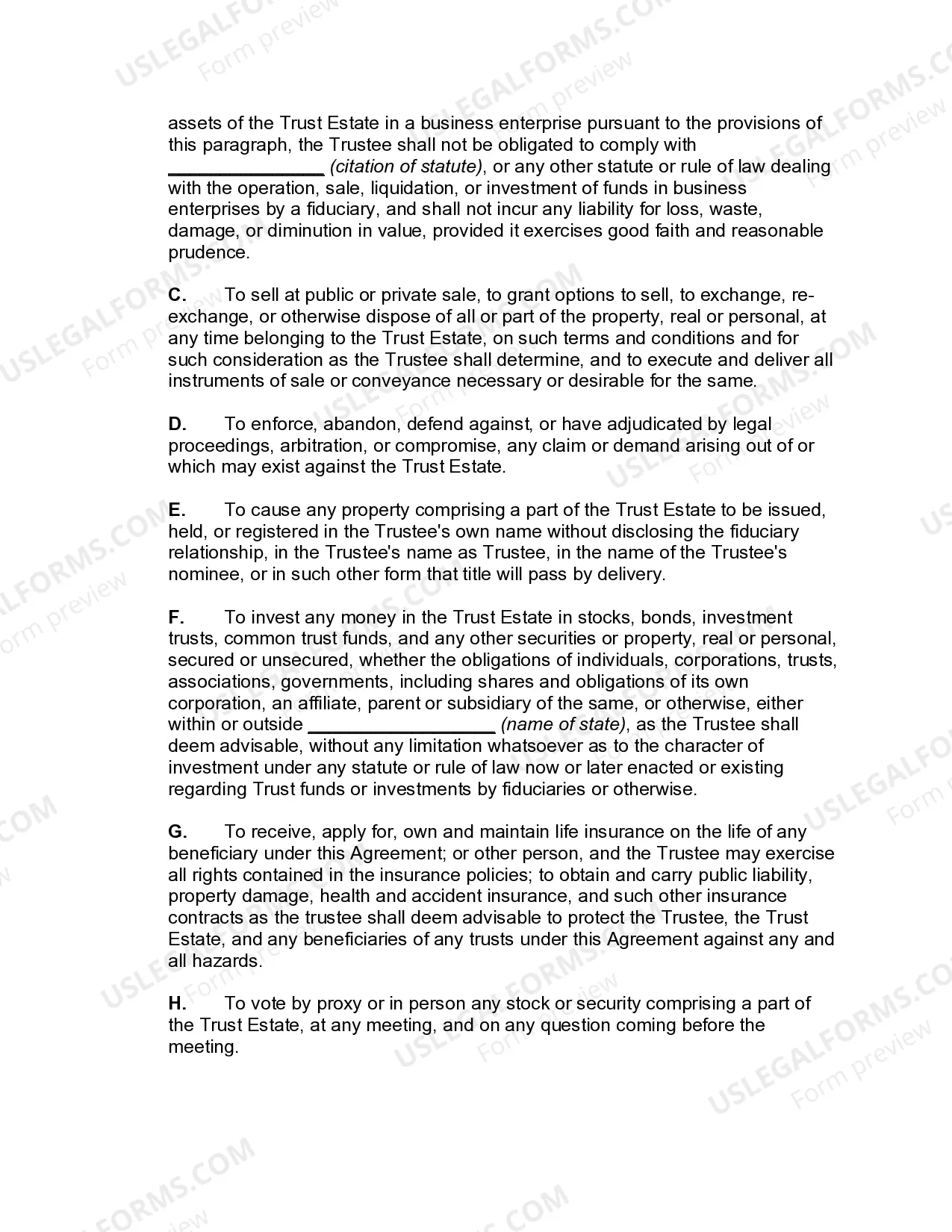

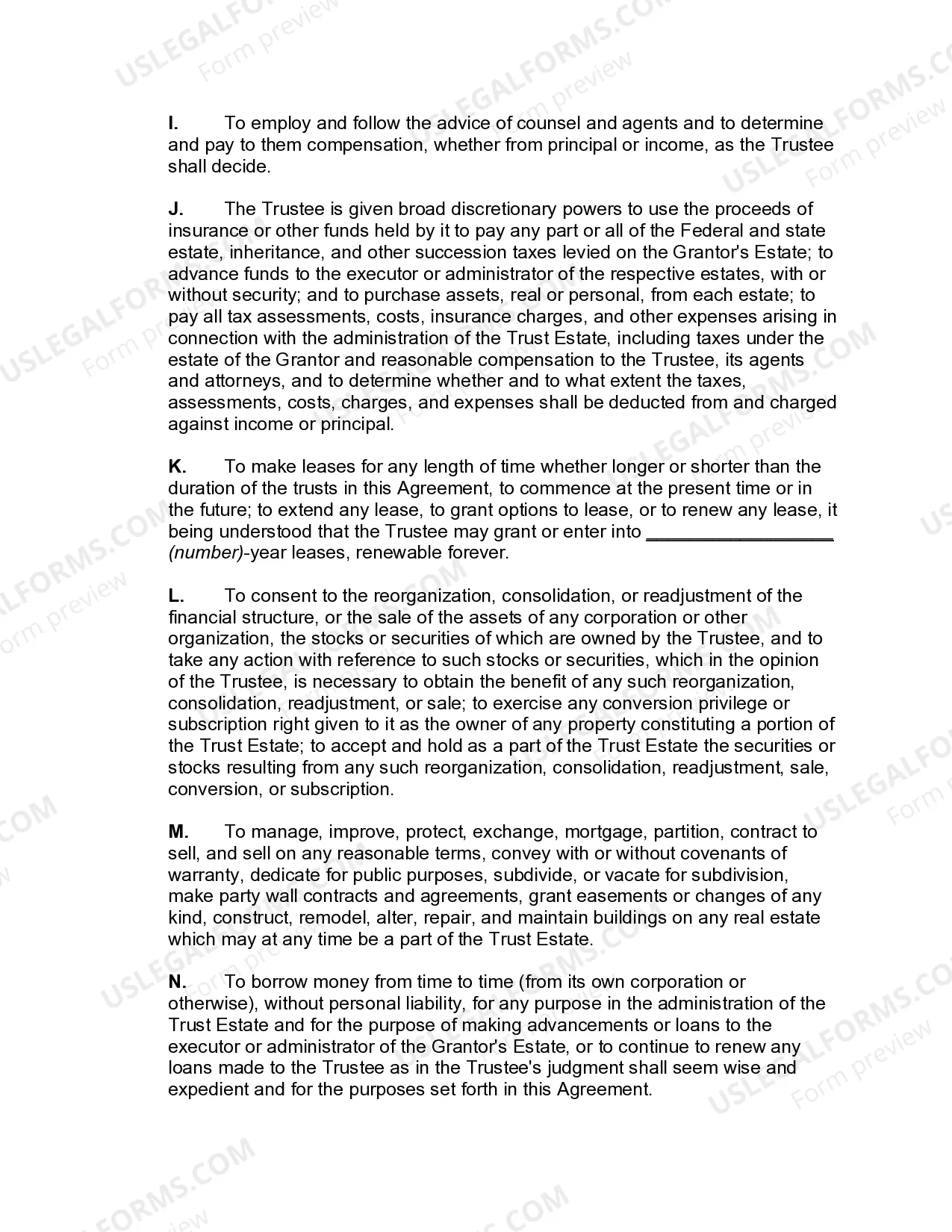

A Guam Qualified Domestic Trust Agreement is a legal document that allows non-U.S. citizen individuals who are beneficiaries of an estate or trust to qualify for the estate tax marital deduction. This agreement is specifically designed for residents of Guam, a U.S. territory located in the Western Pacific Ocean. A Qualified Domestic Trust (DOT) is required when a non-U.S. citizen surviving spouse inherits assets exceeding the federal estate tax exemption limit. Without a DOT, these assets may be subject to hefty estate taxes and potentially create financial burdens for the surviving spouse. By establishing a Guam DOT Agreement, the surviving spouse can defer estate taxes until the assets are distributed from the trust. The Guam DOT Agreement must meet certain requirements set forth by the Internal Revenue Service (IRS). Some key stipulations include: 1. Appointing a trustee: A Guam DOT requires the appointment of a U.S. citizen or domestic corporation as a trustee. The trustee is responsible for overseeing the administration of the trust and managing the assets in compliance with IRS regulations. 2. Annual distribution limitation: The surviving spouse may only receive income generated by the trust on an annual basis. Principal distributions are generally not allowed unless exceptional circumstances warrant it, such as medical emergencies or financial hardships. 3. Estate tax withholding: The trustee is mandated to withhold and pay any applicable estate taxes on distributions made to the surviving spouse. This helps ensure that the IRS receives its due taxes on the assets held in the trust. While there may not be different types of Guam Qualified Domestic Trust Agreements per se, the DOT itself can have various structures and provisions based on the specific needs of the beneficiaries and the complexity of the estate. These include discretionary Dots, marital deduction Dots, and special Dots, each tailored to the unique circumstances of the surviving spouse and the estate. In conclusion, a Guam Qualified Domestic Trust Agreement is an essential tool for non-U.S. citizen beneficiaries in Guam who want to ensure that estate taxes are deferred when inheriting assets beyond the federal estate tax exemption limit. Compliance with IRS regulations and appointing a qualified trustee are crucial for the successful implementation of a Guam DOT.

Guam Qualified Domestic Trust Agreement

Description

How to fill out Guam Qualified Domestic Trust Agreement?

You are able to invest hrs on-line trying to find the authorized document web template that meets the state and federal needs you will need. US Legal Forms supplies 1000s of authorized types which are reviewed by specialists. You can easily acquire or print out the Guam Qualified Domestic Trust Agreement from our services.

If you already possess a US Legal Forms accounts, you can log in and click the Obtain switch. After that, you can complete, revise, print out, or signal the Guam Qualified Domestic Trust Agreement. Each and every authorized document web template you get is your own property permanently. To acquire one more version of any acquired type, check out the My Forms tab and click the related switch.

If you use the US Legal Forms web site for the first time, adhere to the simple instructions under:

- Initially, make certain you have chosen the best document web template for the region/metropolis that you pick. Read the type description to ensure you have picked the right type. If readily available, take advantage of the Review switch to check through the document web template at the same time.

- In order to get one more edition of your type, take advantage of the Lookup field to get the web template that fits your needs and needs.

- Once you have found the web template you would like, click on Buy now to carry on.

- Find the costs plan you would like, key in your references, and register for your account on US Legal Forms.

- Complete the transaction. You can utilize your Visa or Mastercard or PayPal accounts to purchase the authorized type.

- Find the structure of your document and acquire it to the gadget.

- Make changes to the document if possible. You are able to complete, revise and signal and print out Guam Qualified Domestic Trust Agreement.

Obtain and print out 1000s of document templates using the US Legal Forms web site, which offers the greatest collection of authorized types. Use specialist and status-certain templates to take on your organization or individual requirements.

Form popularity

FAQ

You can file your 1040EZ online using MyGuamTax.com, an official service of the Guam Department of Revenue and Taxation. You will need to create a separate user account on MyGuamTax to file your 1040EZ online.

See GRT E-Filing Help.Email grt@revtax.gov.gu.Call 671-635-1835/1836.Write to Department of Revenue and Taxation, BPTB, P.O. Box 23607, GMF, Guam, 96921.

Tax Consequences The QDOT is generally taxed as a simple trust for income tax purposes. This means that when the trust earns income, it MUST be distributed to the surviving spouse. The surviving spouse is then required to pay the income tax on that income based upon the surviving spouses own tax rates.

What Is a Qualified Domestic Trust? A qualified domestic trust (QDOT) is a special kind of trust that allows taxpayers who survive a deceased spouse to take the marital deduction on estate taxes, even if the surviving spouse is not a U.S. citizen.

Walk in to the Department of Revenue and Taxation, Collection branch. Make sure to bring a copy of your e-filed return with the watermark "E-Filed" shown across the page. Mail in your payment. Mail your check payable to "Treasurer of Guam" to the Department of Revenue and Taxation, P.O. Box 23607, GMF, Guam 96921.

A grantor trust is a trust in which the individual who creates the trust is the owner of the assets and property for income and estate tax purposes.

Title 11, Chapter 26, of the Guam Code Annotated provides the authority for imposing gross receipts taxes, and Section 26202(a) of Chapter 26 states that businesses (referred to in this report as taxpayers) selling goods and services will be taxed at a rate of 4 percent on the gross proceeds of sales.

All businesses with sales over $500,000 per year must file monthly GRT reports and pay 4% GRT on all sales to the Treasurer of Guam. All businesses with sales less than or equal to $500,000 per year must file monthly GRT rep01is and pay 4% GRT on all sales over $50,000 to the Treasurer of Guam.

Grantor Trusts are Trusts that can be specifically (and strategically) created for estate tax and income tax purposes. Because of their nature, Grantor Trusts are a type of Revocable Living Trust for the lifetime of the Grantor. A Grantor Trust allows the Grantor to maintain and protect his or her own wealth.

A domestic trust is any trust in which the following conditions are met: (1) A court within the U.S. must be able to exercise primary supervision over the administration of the trust. (2) One or more U.S. persons have the authority to control all substantial decisions of the trust.