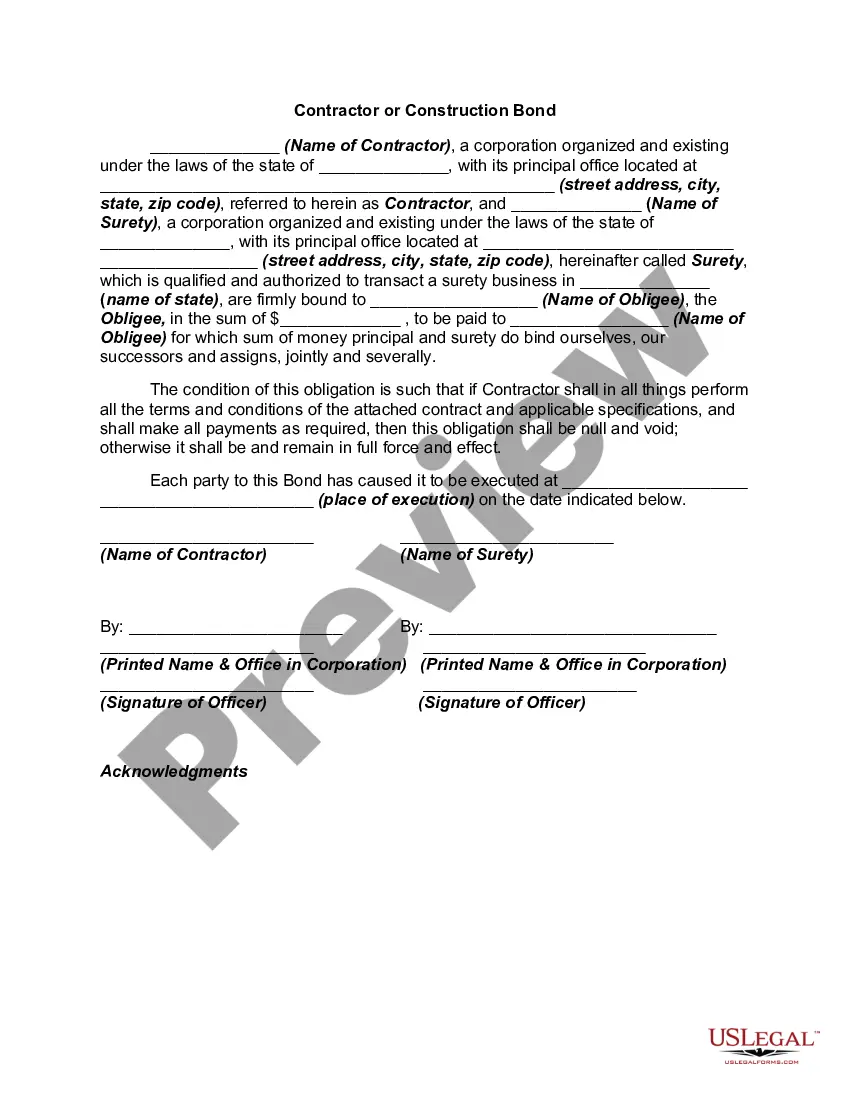

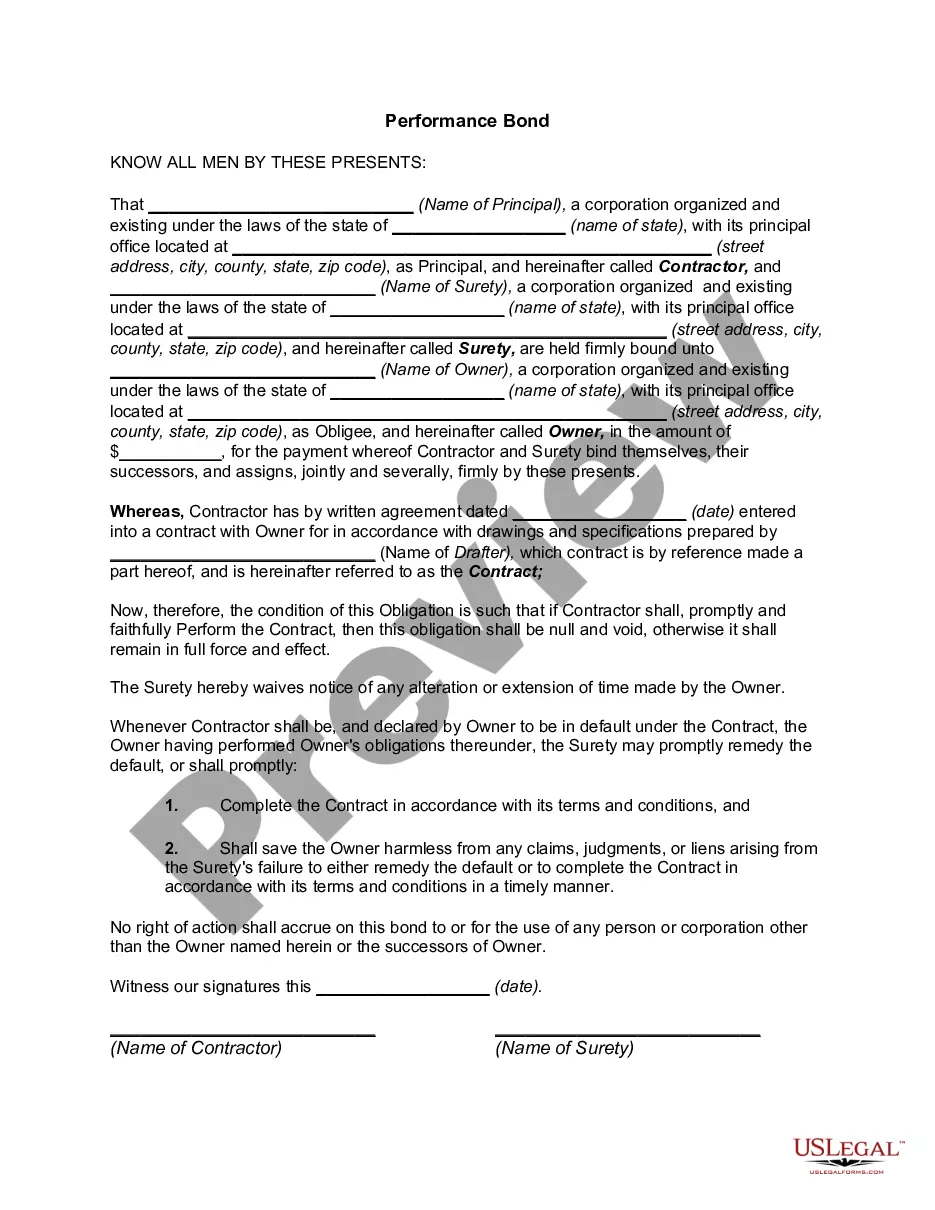

Guam Bond to Secure against Defects in Construction

Description

How to fill out Bond To Secure Against Defects In Construction?

US Legal Forms - among the largest libraries of legal kinds in the United States - offers a variety of legal file themes it is possible to acquire or produce. Using the internet site, you will get 1000s of kinds for business and personal uses, sorted by groups, claims, or keywords.You can get the latest versions of kinds like the Guam Bond to Secure against Defects in Construction in seconds.

If you currently have a subscription, log in and acquire Guam Bond to Secure against Defects in Construction from your US Legal Forms library. The Obtain key will appear on each and every form you view. You gain access to all in the past saved kinds from the My Forms tab of your own accounts.

If you want to use US Legal Forms for the first time, allow me to share easy guidelines to get you started:

- Be sure you have chosen the proper form for your personal town/region. Click the Preview key to examine the form`s content material. See the form information to actually have selected the right form.

- When the form does not satisfy your needs, make use of the Research area on top of the monitor to discover the the one that does.

- If you are pleased with the form, confirm your choice by clicking on the Purchase now key. Then, opt for the pricing strategy you like and give your references to register for the accounts.

- Procedure the deal. Utilize your Visa or Mastercard or PayPal accounts to accomplish the deal.

- Find the structure and acquire the form on your system.

- Make adjustments. Load, edit and produce and signal the saved Guam Bond to Secure against Defects in Construction.

Each and every template you added to your money does not have an expiry date which is yours eternally. So, if you want to acquire or produce another copy, just go to the My Forms segment and click around the form you will need.

Gain access to the Guam Bond to Secure against Defects in Construction with US Legal Forms, by far the most considerable library of legal file themes. Use 1000s of expert and status-certain themes that satisfy your company or personal demands and needs.

Form popularity

FAQ

A warranty bond is a financial guarantee made by a builder to protect the owner of a construction project from defects in materials or workmanship that might arise after the project is completed.

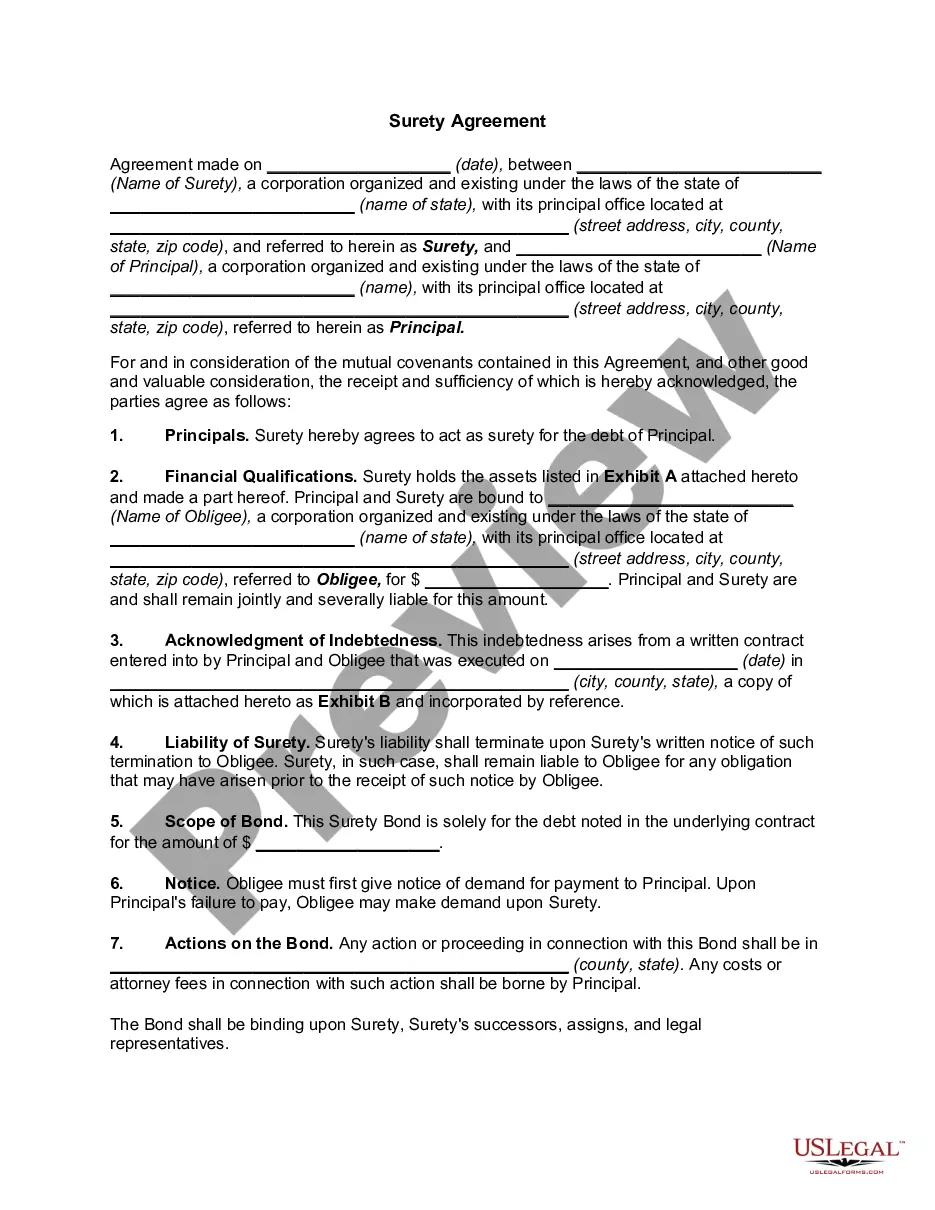

The obligee is the party requiring the principal to obtain a surety bond. They are usually government agencies, local municipalities, individuals, or companies. The surety bond safeguards the obligee from the failure of the principal to uphold their part of the agreement.

In fact, when you get a quote for a surety bond, the quote is a one-time payment quote. This means you will only need to pay it one time (not every month). Bonds are quoted in terms.

Bond, In law, a formal written agreement by which a person undertakes to perform a certain act (e.g., appearing in court or fulfilling the obligations of a contract). Failure to perform the act obligates the person to pay a sum of money or to forfeit money on deposit.

A contract bond is a guarantee the terms of a contract are fulfilled. If the contracted party fails to fulfill its duties ing to the agreed upon terms, the contract ?owner? can claim against the bond to recover financial losses or a stated default provision.

Being bonded means that an insurance and bonding company has procured funds that are available to the customer contingent upon them filing a claim against the company. If you are a contractor or other type of business owner, you may have good reason to explore what it means to be surety bonded.

Contract bonds may have two parts: Review the requirements of the project to see if a bond is necessary. Get a bid bond from an agent from the surety company and submit it with their bid for the contract. If they win the bid, they will go back to the surety company for a performance bond. Complete the project.

The surety's liability is generally limited to the face amount, or penal sum, of the bond, which is typically in the range of 5 to 20 percent of the contract bid price. Sometimes, however, owners require a forfeiture bid bond, which requires the surety to pay the owner the entire penal sum of the bond.