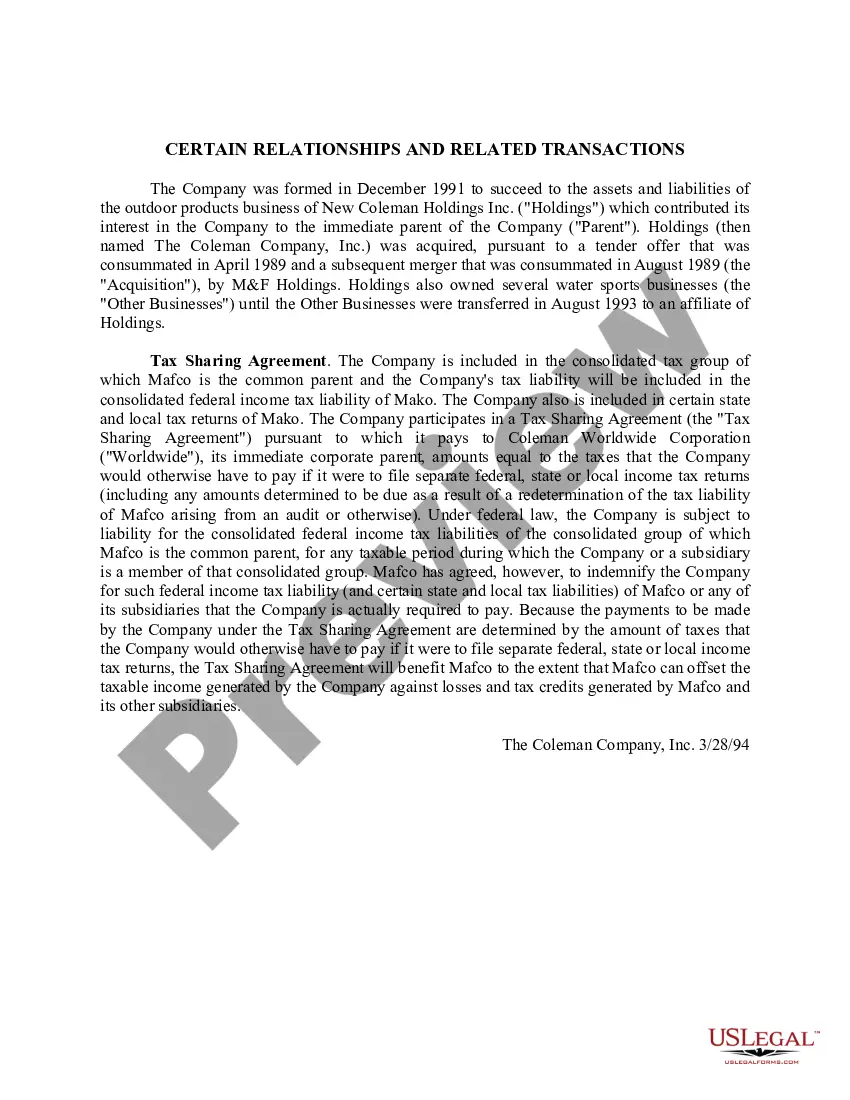

The Guam Tax Sharing Agreement is a legal framework established to distribute tax revenues between the government of Guam and the United States. It is aimed at ensuring a fair distribution of tax revenue to support various services and initiatives for the benefit of the people of Guam. The agreement defines the terms and conditions under which tax revenues generated in Guam, primarily from local businesses and individuals, are shared with the United States. This helps the Guam government maintain its financial stability while fulfilling its obligations to provide essential services such as education, healthcare, infrastructure development, and public safety. In terms of different types of Guam Tax Sharing Agreement, there are two main categories: 1. Organic Act Agreement: This refers to the initial tax sharing agreement established in 1950 when Guam became an organized, unincorporated territory of the United States. The Organic Act Agreement provided the legal basis for sharing tax revenues and outlined the specific terms and conditions applicable at that time. 2. Modern Agreements: Over the years, the tax sharing agreement has undergone modifications and updates to adapt to changing circumstances. These modern agreements aim to address emerging issues and ensure a more equitable distribution of tax revenues. One such example is the Revised Agreement between the Government of Guam and the United States for the Implementation of Section 30 of the Organic Act of Guam, commonly known as the Revised Section 30 Agreement. This revised agreement, signed in 2011, provided new terms and conditions for sharing tax revenues, taking into account the economic growth and evolving needs of the Guamanian community. The Guam Tax Sharing Agreement is a crucial aspect of Guam's financial management and plays a vital role in enabling the government to provide essential services to its residents. It ensures a fair distribution of tax revenues, which promotes economic stability and growth on the island.

Guam Tax Sharing Agreement

Description

How to fill out Guam Tax Sharing Agreement?

US Legal Forms - one of several largest libraries of legitimate kinds in the United States - gives a variety of legitimate papers web templates you are able to download or print. Making use of the web site, you can get thousands of kinds for enterprise and specific functions, categorized by categories, claims, or key phrases.You will discover the most up-to-date models of kinds just like the Guam Tax Sharing Agreement in seconds.

If you have a monthly subscription, log in and download Guam Tax Sharing Agreement from your US Legal Forms collection. The Acquire switch will show up on every develop you view. You have accessibility to all previously downloaded kinds inside the My Forms tab of your own accounts.

If you want to use US Legal Forms the very first time, listed below are basic recommendations to get you started out:

- Ensure you have picked the best develop to your metropolis/state. Click on the Preview switch to examine the form`s articles. Read the develop explanation to actually have chosen the right develop.

- In the event the develop doesn`t suit your demands, use the Research discipline towards the top of the screen to discover the one who does.

- When you are content with the form, verify your selection by clicking the Get now switch. Then, choose the pricing plan you like and provide your accreditations to sign up to have an accounts.

- Approach the purchase. Utilize your charge card or PayPal accounts to complete the purchase.

- Choose the formatting and download the form on your product.

- Make changes. Complete, revise and print and indicator the downloaded Guam Tax Sharing Agreement.

Each template you added to your money does not have an expiration time and is also the one you have eternally. So, in order to download or print yet another backup, just proceed to the My Forms area and then click about the develop you require.

Obtain access to the Guam Tax Sharing Agreement with US Legal Forms, probably the most extensive collection of legitimate papers web templates. Use thousands of skilled and status-distinct web templates that fulfill your organization or specific demands and demands.