Guam Elimination of the Class A Preferred Stock

Description

How to fill out Elimination Of The Class A Preferred Stock?

If you wish to total, obtain, or produce lawful papers web templates, use US Legal Forms, the most important assortment of lawful types, that can be found on-line. Take advantage of the site`s easy and hassle-free search to get the files you will need. Numerous web templates for enterprise and specific functions are sorted by groups and suggests, or keywords. Use US Legal Forms to get the Guam Elimination of the Class A Preferred Stock within a few clicks.

When you are previously a US Legal Forms buyer, log in for your bank account and then click the Down load option to have the Guam Elimination of the Class A Preferred Stock. You can even access types you in the past acquired within the My Forms tab of your respective bank account.

Should you use US Legal Forms the very first time, follow the instructions listed below:

- Step 1. Be sure you have chosen the shape for your appropriate city/region.

- Step 2. Take advantage of the Preview option to examine the form`s information. Never forget to read through the description.

- Step 3. When you are unsatisfied together with the develop, make use of the Look for field near the top of the monitor to discover other types of your lawful develop template.

- Step 4. After you have found the shape you will need, go through the Acquire now option. Choose the rates prepare you choose and include your accreditations to sign up for the bank account.

- Step 5. Method the deal. You can utilize your charge card or PayPal bank account to perform the deal.

- Step 6. Pick the file format of your lawful develop and obtain it in your gadget.

- Step 7. Full, edit and produce or indication the Guam Elimination of the Class A Preferred Stock.

Each and every lawful papers template you purchase is your own property permanently. You have acces to each develop you acquired inside your acccount. Click the My Forms portion and select a develop to produce or obtain again.

Contend and obtain, and produce the Guam Elimination of the Class A Preferred Stock with US Legal Forms. There are many skilled and state-specific types you can utilize for the enterprise or specific requires.

Form popularity

FAQ

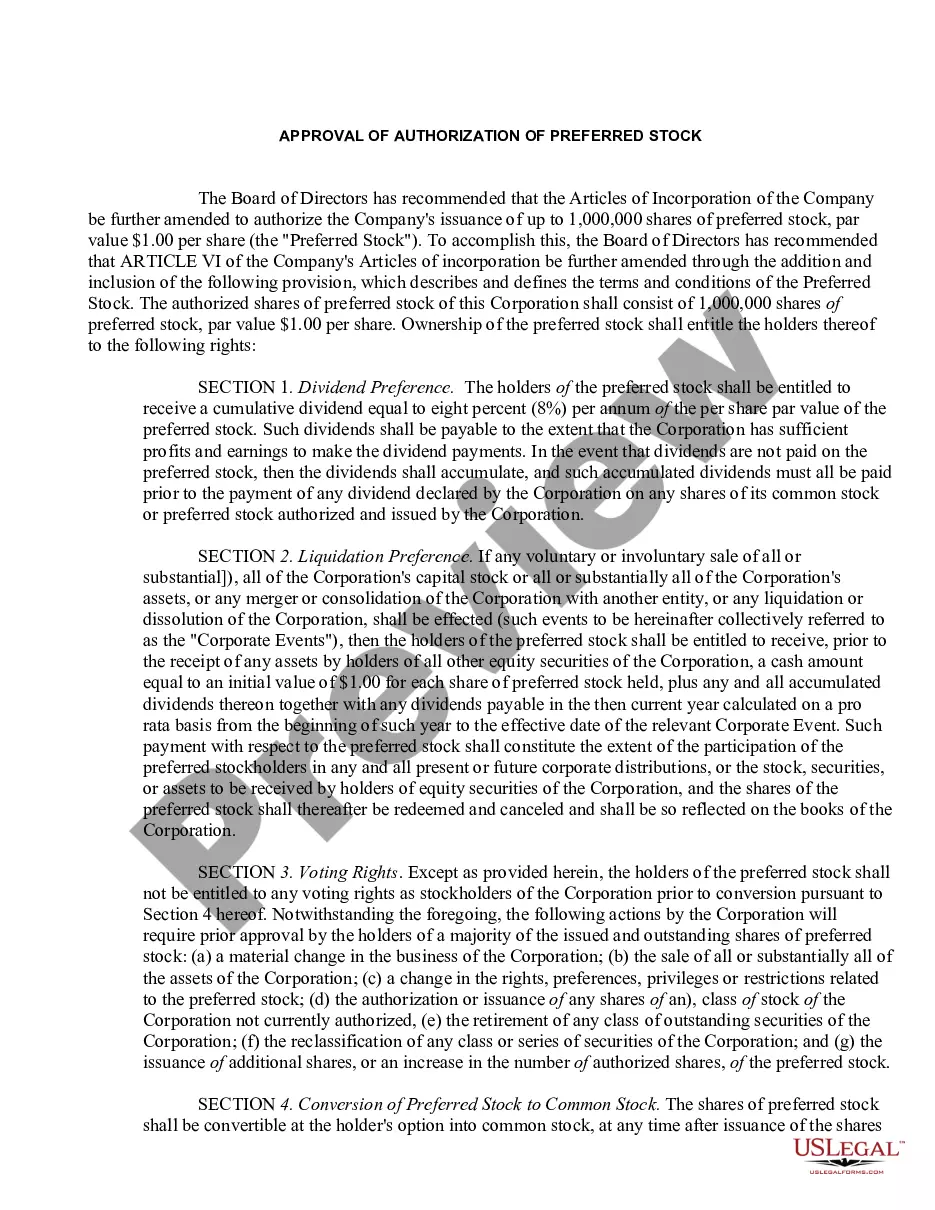

Preferred shares are a hybrid form of equity that includes debt-like features such as a guaranteed dividend. The four main types of preference shares are callable shares, convertible shares, cumulative shares, and participatory shares.

Cumulative preferred stock provides consistent income to shareholders. It ensures that if dividends are not paid in a particular period, they accumulate and must be paid in the future. This feature can attract risk-averse investors who seek reliable dividend payments and a degree of security.

§ When a corporation has only one class of stock it is common stock.

What Is Cumulative Preferred Stock? Cumulative preferred stock is a type of preferred stock with a provision that stipulates that if any dividend payments have been missed in the past, the dividends owed must be paid out to cumulative preferred shareholders first.

Preference Shares2 can be cumulative or non-cumulative. The former gives shareholders the right to receive cumulative dividend payouts from the company even if they are not profitable. That dividend payout can be made at some later point of time.

Whether a preferred stock is cumulative or straight (non-cumulative) determines if the issuer must make up skipped payments. If it's cumulative, the issuer must pay missed dividends to preferred stockholders at some point. If it's straight, the issuer will not make up skipped dividends.

When preferred stock is cumulative and the directors either do not declare a dividend to preferred stockholders or declare one that does not cover the total amount of cumulative dividend, the unpaid dividend amount is called dividend in arrears.

If the assessment results in an extinguishment, then the difference between the consideration paid (i.e., the fair value of the new or modified preferred stock) and the carrying value of the original preferred stock should be recognized as a reduction of, or increase to, retained earnings as a deemed dividend.