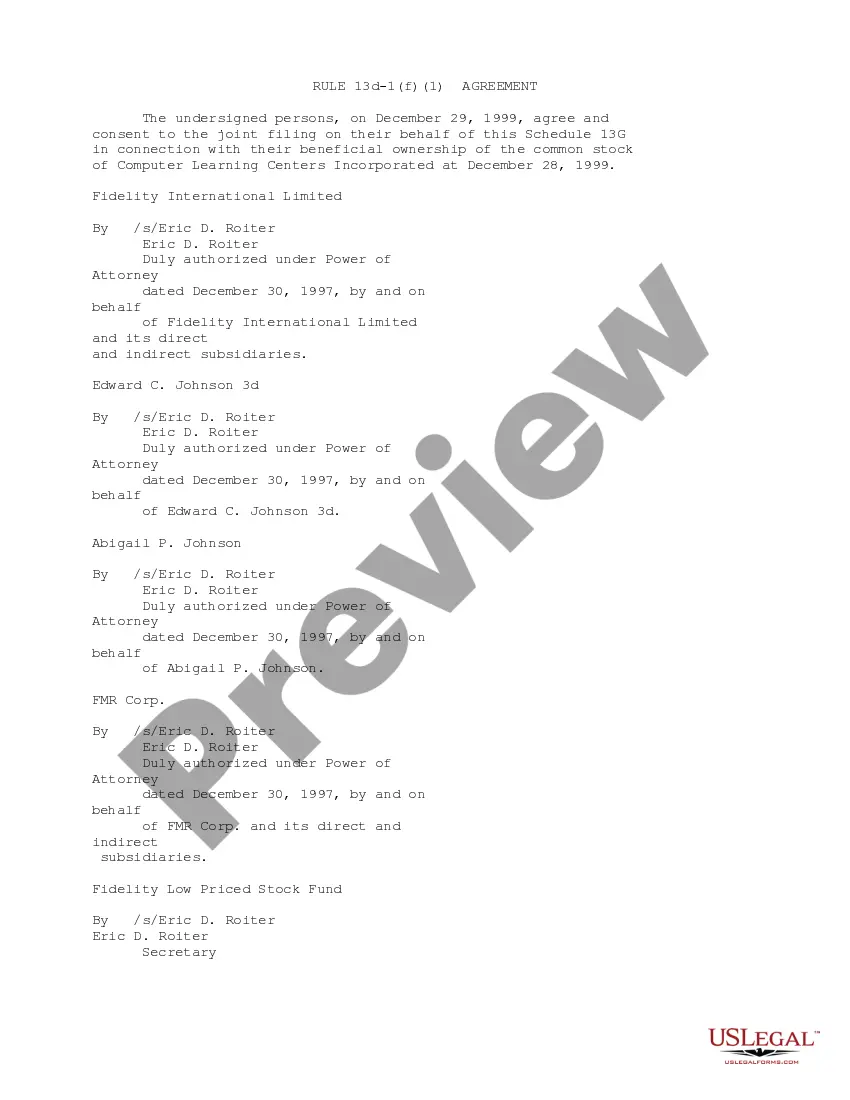

Guam Joint Filing of Rule 13d-1(f)(1) Agreement: A Comprehensive Overview The Guam Joint Filing of Rule 13d-1(f)(1) Agreement refers to a specific filing requirement outlined by the U.S. Securities and Exchange Commission (SEC) for entities in Guam. To understand this agreement thoroughly, let's break it down into its various components. 1. Guam: Guam is an organized and unincorporated territory of the United States, situated in the western part of the Pacific Ocean. It is the largest and southernmost of the Mariana Islands and is subject to U.S. federal laws and regulations. 2. Joint Filing: The concept of joint filing relates to multiple entities or individuals collaborating to submit a filing together. In the case of Rule 13d-1(f)(1), the SEC mandates certain parties to jointly file specific disclosures to ensure transparency and investor protection. 3. Rule 13d-1(f)(1): Rule 13d-1(f)(1) is a provision under the Securities Exchange Act of 1934, established by the SEC. It requires entities, once they cross a specific ownership threshold in a public company (usually 5%), to submit a filing disclosing their ownership and intentions. The joint filing requirement enhances transparency and provides investors with crucial information. 4. Agreement: The Guam Joint Filing of Rule 13d-1(f)(1) Agreement signifies the mutual understanding and consent between parties filing jointly under Rule 13d-1(f)(1). This agreement outlines the obligations, responsibilities, and scope of collaboration involved in the joint filing process. Different Types of Guam Joint Filing of Rule 13d-1(f)(1) Agreements: 1. Corporate Joint Filings: This type of agreement involves two or more affiliated corporations jointly filing their ownership and intentions under Rule 13d-1(f)(1). It commonly occurs when multiple corporations are part of a larger parent company or share a controlling interest. 2. Institutional Joint Filings: Institutional joint filings involve multiple institutional investors, such as mutual funds, pension funds, or hedge funds, collaborating to file disclosures as they cross the ownership threshold specified by Rule 13d-1(f)(1). 3. Individual Joint Filings: Occasionally, individuals may engage in joint filings when they collectively own shares surpassing the reporting threshold. This often occurs in the case of family members or business partners jointly investing in a particular company. 4. Foreign Joint Filings: This category refers to joint filings involving entities based in Guam but incorporated or doing business outside the United States. It ensures that even foreign-based entities adhering to Rule 13d-1(f)(1) requirements are transparent about their ownership and intentions. In conclusion, the Guam Joint Filing of Rule 13d-1(f)(1) Agreement serves as a vital compliance tool for various entities operating in or linked to Guam. These agreements facilitate transparency and disclosure of ownership and intentions when parties collectively hold a significant stake in a public company, fostering investor confidence and safeguarding the integrity of the securities market.

Guam Joint Filing of Rule 13d-1(f)(1) Agreement

Description

How to fill out Guam Joint Filing Of Rule 13d-1(f)(1) Agreement?

US Legal Forms - one of several greatest libraries of legal varieties in the USA - provides an array of legal document themes you are able to download or print out. Making use of the website, you can find thousands of varieties for enterprise and specific reasons, sorted by classes, says, or keywords and phrases.You can find the most up-to-date versions of varieties much like the Guam Joint Filing of Rule 13d-1(f)(1) Agreement in seconds.

If you currently have a membership, log in and download Guam Joint Filing of Rule 13d-1(f)(1) Agreement through the US Legal Forms library. The Obtain button can look on each develop you look at. You gain access to all in the past downloaded varieties in the My Forms tab of the accounts.

If you wish to use US Legal Forms for the first time, here are basic directions to get you started:

- Be sure you have picked the right develop for your personal area/state. Click on the Preview button to analyze the form`s content. Look at the develop explanation to actually have selected the appropriate develop.

- If the develop doesn`t satisfy your needs, use the Lookup area towards the top of the display screen to obtain the one that does.

- Should you be satisfied with the shape, validate your choice by simply clicking the Get now button. Then, opt for the pricing plan you prefer and provide your credentials to sign up for the accounts.

- Process the financial transaction. Make use of charge card or PayPal accounts to perform the financial transaction.

- Choose the structure and download the shape on your device.

- Make changes. Load, edit and print out and indicator the downloaded Guam Joint Filing of Rule 13d-1(f)(1) Agreement.

Every single template you included in your bank account lacks an expiry date and is also your own eternally. So, if you would like download or print out one more version, just check out the My Forms area and click on about the develop you want.

Obtain access to the Guam Joint Filing of Rule 13d-1(f)(1) Agreement with US Legal Forms, probably the most comprehensive library of legal document themes. Use thousands of expert and status-certain themes that meet your business or specific requirements and needs.