- passing of title;

- made with the intent to pass title;

- without receiving money or value in consideration for the passing of title.

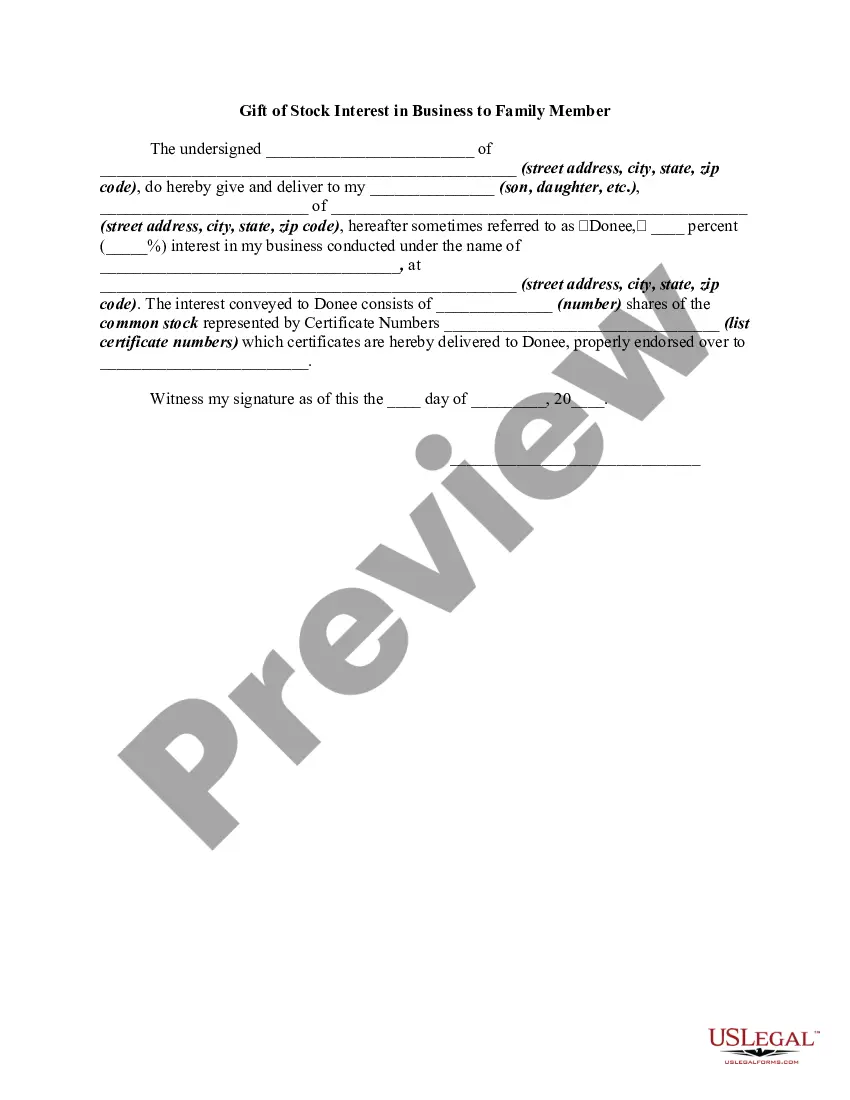

Hawaii Gift of Stock Interest in Business to Family Member refers to the act of transferring stock ownership in a business to a family member as a gift. This type of transaction allows individuals in Hawaii to transfer their ownership interest in a business to a family member while potentially deriving certain tax benefits. The term "Gift of Stock Interest in Business to Family Member" implies that the transfer involves gifting shares or stocks that represent a certain ownership stake in a business. The person gifting the stock may hold various positions within the business, such as majority shareholder, partner, or member of a limited liability company (LLC). By opting for a gift of stock interest, the individual is essentially conveying their ownership rights, voting power, and entitlement to dividends or profits associated with the stocks to a family member. This type of transfer can have several implications, including succession planning, family wealth management, estate planning, and tax planning. Under Hawaii law, there may be specific regulations and procedures that need to be followed when gifting stock interest. It is crucial to consult with an attorney or financial advisor specializing in business law to ensure compliance with state regulations and to navigate the complexities of such a transfer effectively. Different types of Hawaii Gift of Stock Interest in Business to Family Member may include: 1. Inter vivos gift: This refers to a gift made during the lifetime of the giver. By transferring stock interest in a business to a family member through an inter vivos gift, the giver can potentially minimize estate taxes while also providing an opportunity for the recipient to benefit from the business ownership. 2. Testamentary gift: This type of gift involves transferring stock interest through a will or other testamentary document, which will take effect upon the giver's death. Testaments can provide an orderly transfer of ownership and may include further provisions regarding the management or control of the business. 3. Minority interest gift: In some cases, a giver may only transfer a minority interest in the business to a family member. This means that the recipient will hold less than a controlling stake, allowing the giver to retain control while providing a gift that allows the recipient to benefit from the business's future success. Implementing a Hawaii Gift of Stock Interest in Business to Family Member can have various legal and tax implications, depending on the specific circumstances and the structure of the business. It is crucial to seek professional advice to navigate the complexities and ensure compliance with state laws and regulations.