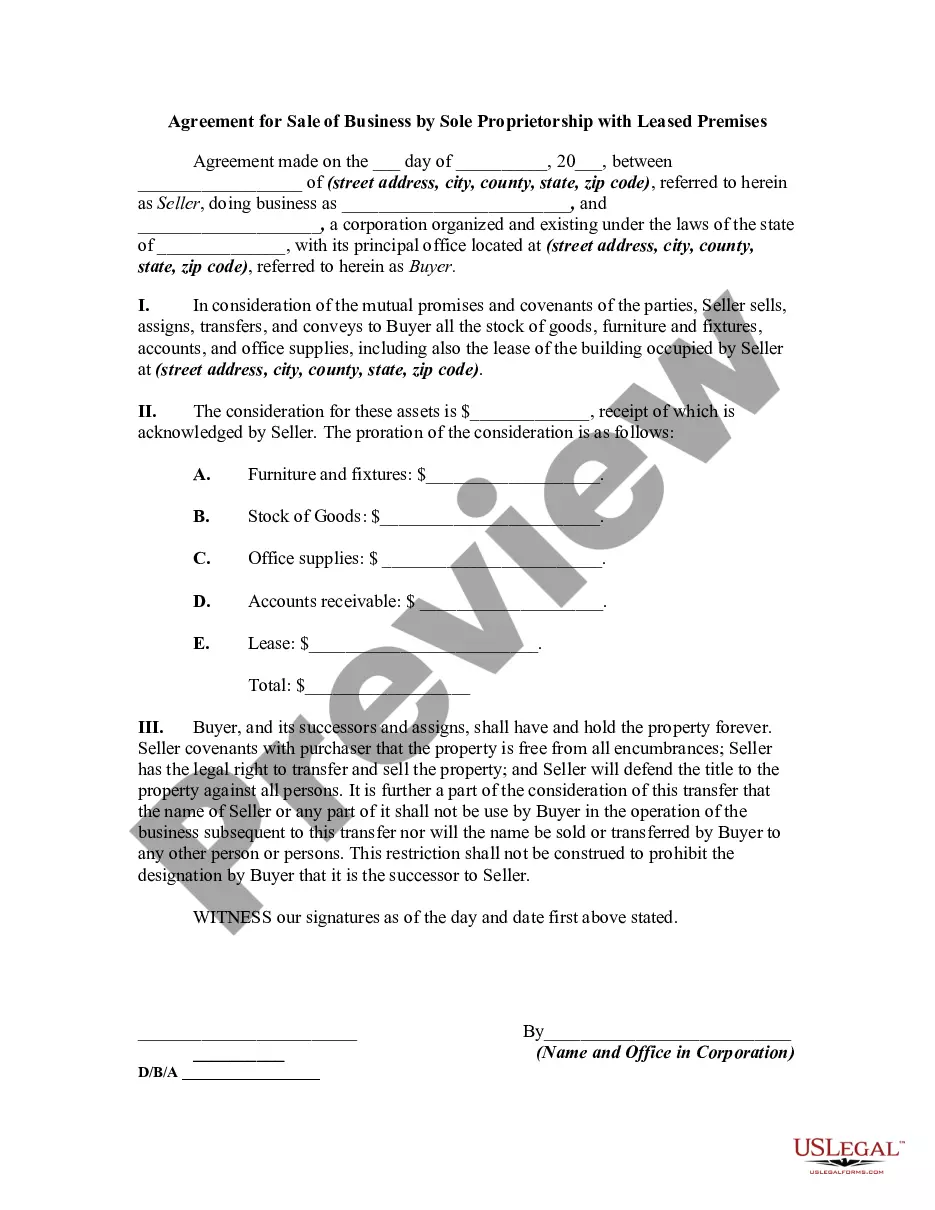

The Hawaii Agreement for Sale of Business by Sole Proprietorship with Leased Premises is a legal document that outlines the terms and conditions for the sale of a business owned by a sole proprietorship in Hawaii, where the business operates out of leased premises. This agreement is crucial to protect the interests of both the buyer and seller involved in the sale transaction. Key elements included in the Hawaii Agreement for Sale of Business by Sole Proprietorship with Leased Premises typically consist of: 1. Parties involved: The agreement begins by identifying the buyer, who intends to purchase the business, and the seller, who is the sole proprietor of the business. Both parties are named along with their contact information. 2. Business details: This section outlines the specific details of the business being sold. It includes the legal business name, physical address of the leased premises, and any relevant permits or licenses necessary for the operation of the business. 3. Purchase price and payment terms: The agreement specifies the purchase price of the business, along with the payment terms agreed upon by both parties. This may include the amount of the initial deposit, any installment payments, and the due date for the final payment. 4. Assets and liabilities: It is essential to identify the assets being transferred as part of the sale. This includes tangible assets such as equipment, inventory, and furnishings, as well as intangible assets like customer lists, intellectual property, and goodwill. Any outstanding liabilities or debts associated with the business should also be clearly stated. 5. Condition of the business: This section describes the current condition of the business and its leased premises. It may outline any warranties, guarantees, or representations made by the seller regarding the business's operational status, financial records, or lease agreements. 6. Closing procedures: The agreement sets out the procedures for the closing of the sale. This may include a specific date for the completion of the transaction, the transfer of ownership, and the handover of necessary documents and keys. Different types of Hawaii Agreement for Sale of Business by Sole Proprietorship with Leased Premises may exist based on the nature of the business being sold. For instance, there could be specific agreements tailored for restaurants, retail stores, service-oriented businesses, or professional practices. The specific type of business should be clearly stated in the agreement to ensure accuracy and adherence to Hawaii's laws and regulations. In conclusion, the Hawaii Agreement for Sale of Business by Sole Proprietorship with Leased Premises is a legally binding document that serves as a comprehensive guide for buyers and sellers operating in the state. By addressing crucial details such as business assets, purchase price, payment terms, and closing procedures, this agreement ensures a smooth, fair, and transparent transaction between parties involved in the sale.

Hawaii Agreement for Sale of Business by Sole Proprietorship with Leased Premises

Description

How to fill out Hawaii Agreement For Sale Of Business By Sole Proprietorship With Leased Premises?

US Legal Forms - one of the most extensive collections of official documents in the USA - provides a broad array of authentic template documents that you can download or print. By utilizing the website, you can access numerous forms for commercial and personal use, categorized by types, states, or keywords.

You can quickly find the latest versions of documents such as the Hawaii Agreement for Sale of Business by Sole Proprietorship with Leased Premises.

If you already have an account, sign in and download the Hawaii Agreement for Sale of Business by Sole Proprietorship with Leased Premises from the US Legal Forms library. The Download option will be visible on each form you view. You can access all previously downloaded forms in the My documents tab of your account.

Process the purchase. Use your credit card or PayPal account to complete the transaction.

Select the format and download the form to your device. Edit. Fill out, modify, print, and sign the downloaded Hawaii Agreement for Sale of Business by Sole Proprietorship with Leased Premises. Every template you add to your account does not expire and is yours indefinitely. Therefore, if you wish to download or print another copy, simply go to the My documents section and click on the form you need. Access the Hawaii Agreement for Sale of Business by Sole Proprietorship with Leased Premises through US Legal Forms, the largest collection of legitimate document templates. Utilize countless professional and state-specific templates that fulfill your business or personal requirements.

- If you are using US Legal Forms for the first time, here are simple steps to get you started.

- Ensure you have selected the correct form for your state/region.

- Choose the Preview option to review the form's details.

- Examine the form description to confirm that you have picked the appropriate form.

- If the form does not meet your needs, use the Search field at the top of the page to find one that does.

- If you are satisfied with the form, validate your choice by clicking the Buy now button.

- Then, select the payment plan you prefer and provide your information to register for the account.

Form popularity

FAQ

The legal binding nature of a verbal agreement varies based on the context and content of the agreement. While they can be enforced, they often face scrutiny in court due to lack of evidence. For significant matters such as a Hawaii Agreement for Sale of Business by Sole Proprietorship with Leased Premises, it is advisable to document the agreement in writing to avoid potential disputes.

In Hawaii, a bill of sale does not typically need to be notarized for it to be considered valid. However, notarization can add an extra layer of security and authenticity to the transaction. When finalizing a Hawaii Agreement for Sale of Business by Sole Proprietorship with Leased Premises, you may want to consider notarizing the bill of sale for peace of mind.

Yes, Hawaii does recognize verbal agreements as legally binding under certain conditions. However, complexities may arise when attempting to enforce them in court. Therefore, when dealing with a Hawaii Agreement for Sale of Business by Sole Proprietorship with Leased Premises, securing a formal written agreement is the best approach.

Verbal contracts can be binding in most states, including Hawaii, but they often face challenges in enforcement. The enforceability hinges on the specific terms and circumstances. Thus, for critical agreements like a Hawaii Agreement for Sale of Business by Sole Proprietorship with Leased Premises, it is wise to opt for a written agreement to ensure clarity and legal protection.

Yes, a verbal agreement can be legally binding, depending on the circumstances surrounding the agreement. Certain elements must exist, such as mutual consent and a clear understanding of the terms. However, for transactions like a Hawaii Agreement for Sale of Business by Sole Proprietorship with Leased Premises, it is always safer to have a written document to solidify the agreement.

An agreement of sale serves to outline the terms and conditions under which a business is sold. It defines the rights and obligations of both parties, ensuring clarity on the transaction. For those involved in a Hawaii Agreement for Sale of Business by Sole Proprietorship with Leased Premises, this document is essential for a smooth and efficient sale process.

In general, a verbal agreement can be difficult to uphold in court. While it may seem easy to back out, doing so can lead to misunderstandings. If your verbal agreement pertains to a Hawaii Agreement for Sale of Business by Sole Proprietorship with Leased Premises, it is advisable to document the terms formally to avoid complications.

Selling a sole proprietor business requires careful planning and documentation. Start by evaluating your business's value, then prepare a comprehensive sales agreement that includes all business assets and liabilities. The Hawaii Agreement for Sale of Business by Sole Proprietorship with Leased Premises is an excellent resource for creating a formal agreement that protects both parties during the transfer.

When closing a business, you must settle debts, notify clients, and cancel permits and licenses. Additionally, prepare final tax returns and manage any last payroll obligations. Before finalizing, ensure all documentation aligns with business regulations, and consider using the Hawaii Agreement for Sale of Business by Sole Proprietorship with Leased Premises to aid in any transactions related to business closure.

You should file the Hawaii general excise tax return based on your designated filing frequency, which could be monthly, quarterly, or annually. Ensure that you file on or before the due date to avoid any unnecessary penalties. When involved in the Hawaii Agreement for Sale of Business by Sole Proprietorship with Leased Premises, keeping a calendar of these deadlines is beneficial. Resources offered by US Legal Forms can help you manage your filing times effectively.