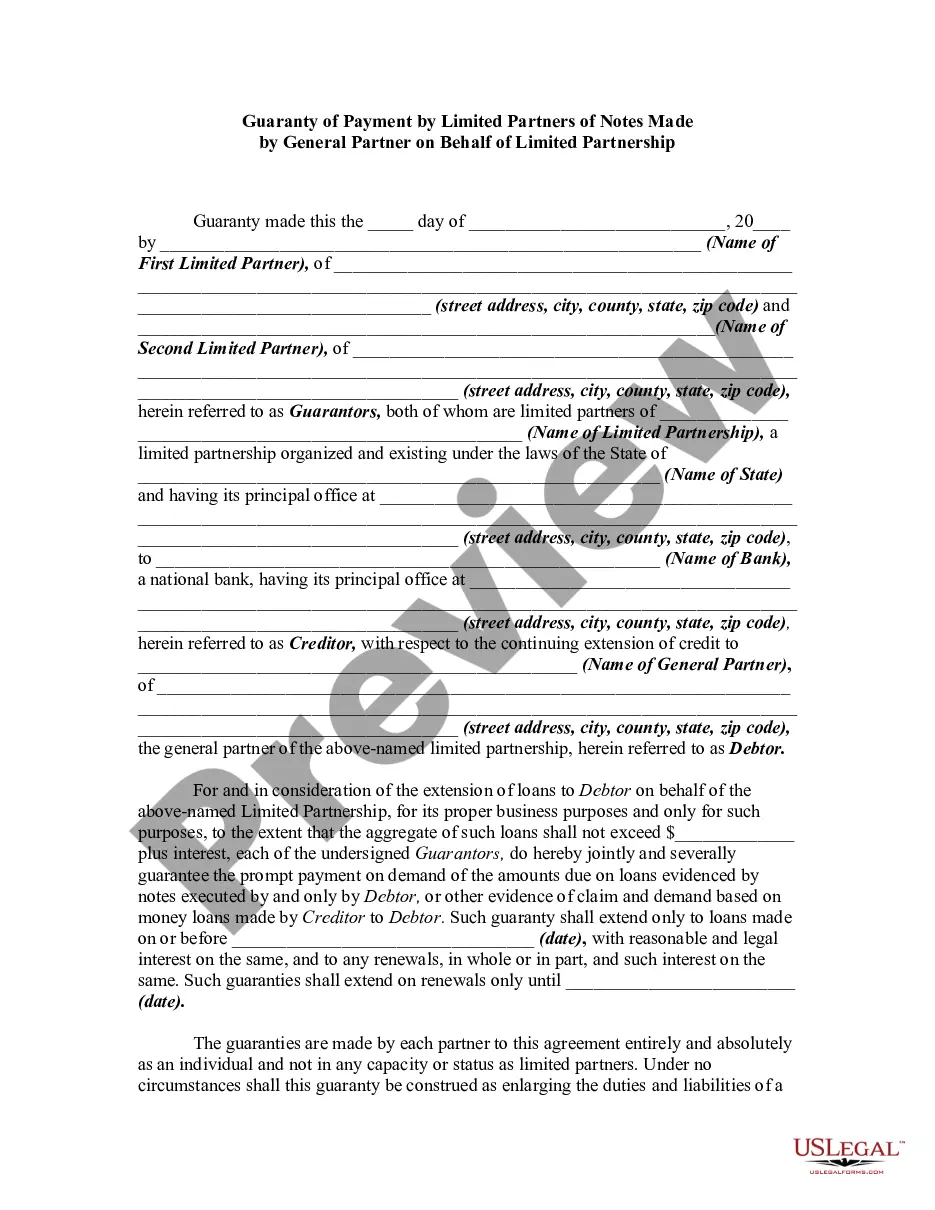

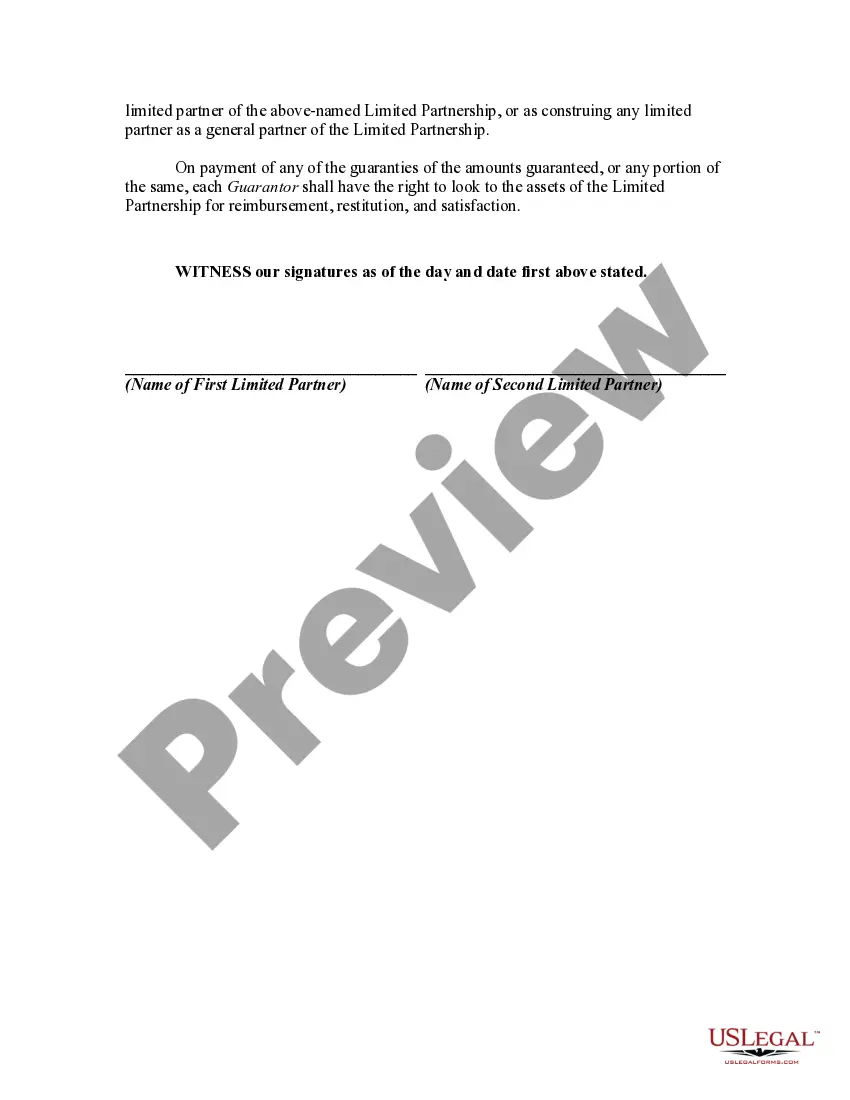

A limited partnership is a modified partnership. It has characteristics of both a corporation and a general partnership. In a limited partnership, certain members contribute capital, but do not have liability for the debts of the partnership beyond the amount of their investment. These members are known as limited partners. The partners who manage the business and who are personally liable for the debts of the business are the general partners. Limited partners have the right to share in the profits of the business and, if the partnership is dissolved, will be entitled to a percentage of the assets of the partnership. A limited partner may lose his limited liability status if he participates in the control of the business.

Hawaii Guaranty of Payment by Limited Partners of Notes Made by General Partner on Behalf of Limited Partnership is a legal document that outlines the responsibilities and obligations of limited partners in regard to financial obligations and payment guarantees within a limited partnership structure. This agreement specifically addresses potential liabilities arising from general partner-issued notes on behalf of the limited partnership. The purpose of the Hawaii Guaranty of Payment is to ensure that limited partners are responsible for guaranteeing timely repayment of any notes issued by the general partner on behalf of the limited partnership. This document serves as a protection mechanism for lenders, as limited partners are personally liable for any default or non-payment of the notes. The Hawaii Guaranty of Payment places an obligation on limited partners to fulfill payment obligations in case the general partner is unable to fulfill its financial commitments. As a result, lenders have added security knowing that their financial interests are protected by limited partners' guarantees. There are different variations of the Hawaii Guaranty of Payment, which may include: 1. Full Guaranty: This type of guaranty ensures that limited partners are fully responsible for the repayment of the notes issued by the general partner on behalf of the limited partnership. In the event of default, the lender can directly demand payment from any of the limited partners. 2. Limited Guaranty: This form of guaranty allows limited partners to limit their liability by specifying the extent to which they are responsible for the repayment of the notes. The limited guaranty may include specific limitations or conditions under which limited partners would be held liable. 3. Conditional Guaranty: In this type of guaranty, limited partners are only obligated to repay the notes if certain predetermined conditions are not met. These conditions may include the general partner's insolvency, bankruptcy, or failure to meet specific financial obligations. It is crucial for all parties involved, including limited partners, general partners, and lenders, to carefully review and fully understand the Hawaii Guaranty of Payment by Limited Partners of Notes Made by General Partner on Behalf of Limited Partnership before entering into any agreement. Seeking legal advice is highly advisable to ensure compliance with relevant laws and protection of all parties' interests.