Although no definite rule exists for determining whether one is an independent contractor or an employee, certain indicia of the status of an independent contractor are recognized, and the insertion of provisions embodying these indicia in the contract will help to insure that the relationship reflects the intention of the parties. These indicia generally relate to the basic issue of control. The general test of what constitutes an independent contractor relationship involves which party has the right to direct what is to be done, and how and when. Another important test involves the method of payment of the contractor.

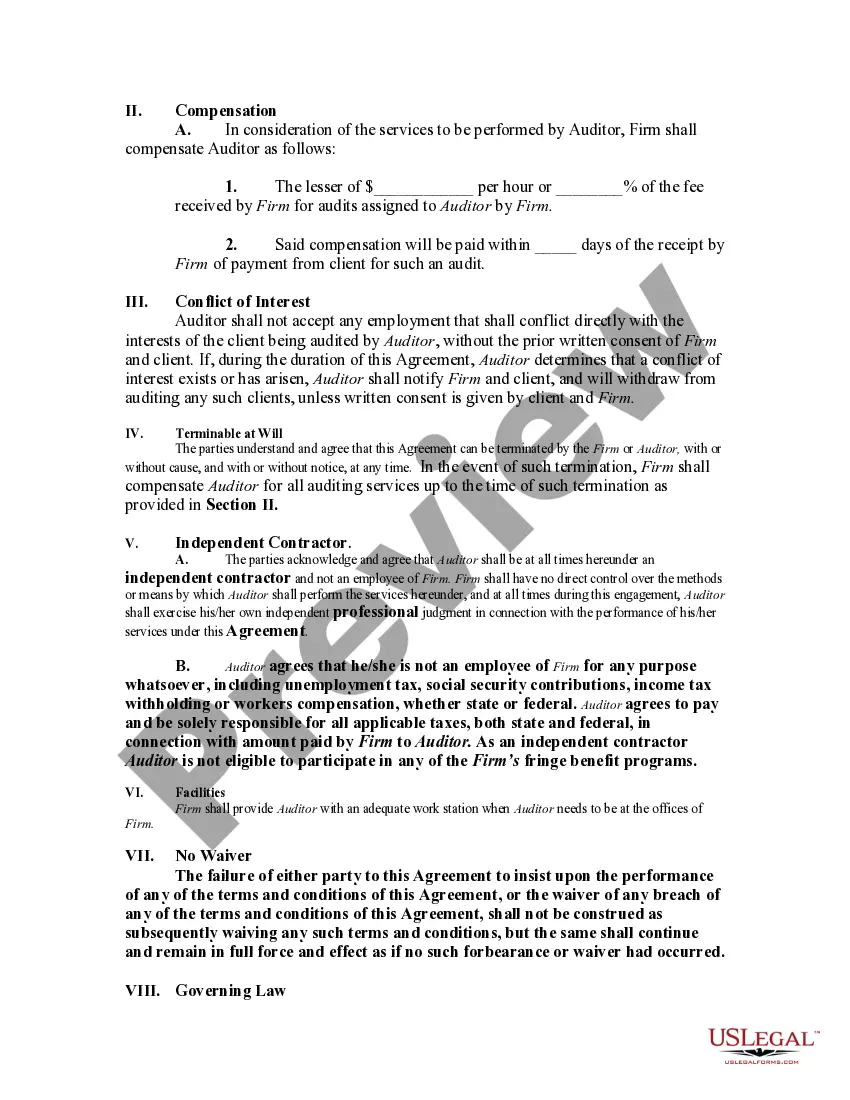

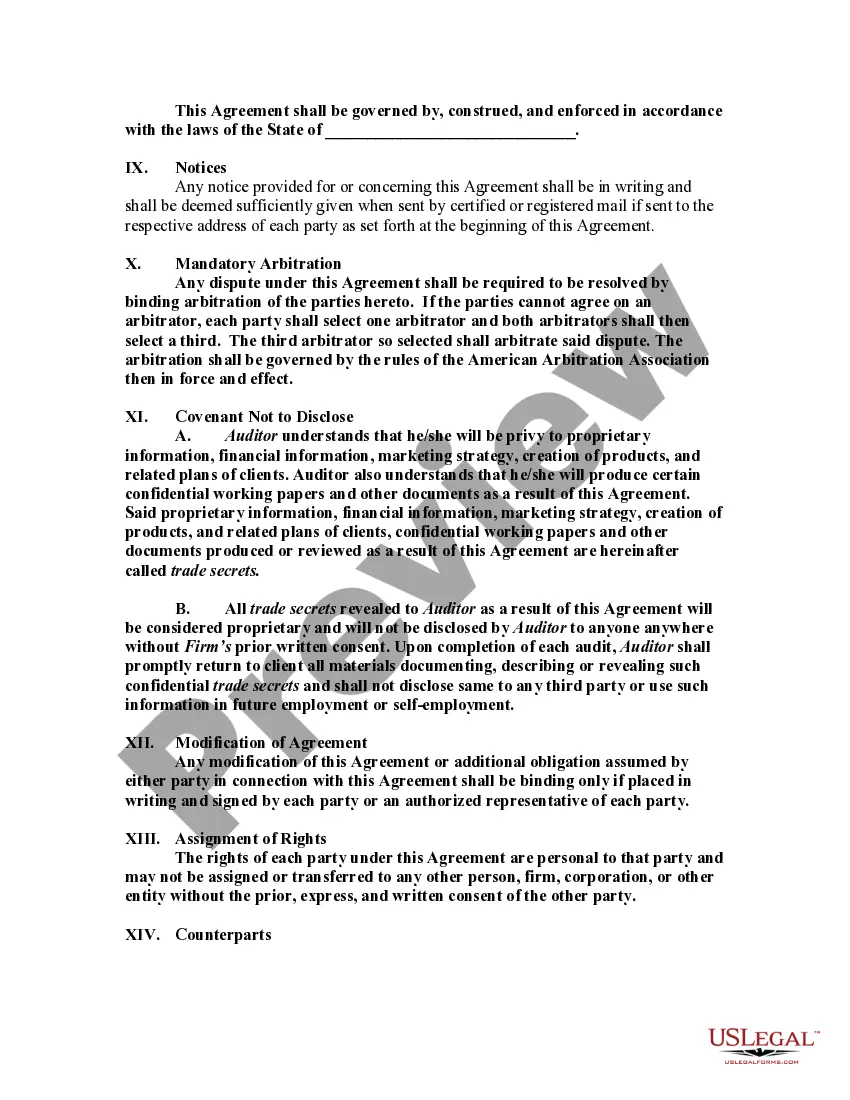

Title: Hawaii Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor Introduction: In Hawaii, accounting firms often enter into agreements with auditors, employing them as self-employed independent contractors. These agreements establish the terms and conditions under which the auditor will provide their services to the accounting firm. This detailed description will provide an overview of the Hawaii Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor, highlighting its key elements and variations. Key Elements of the Hawaii Agreement: 1. Scope of Work: The agreement defines the specific services the auditor will render to the accounting firm, such as conducting audits, financial reviews, or other specialized tasks. It outlines the duration of the engagement or projects to be completed in a given period. 2. Independent Contractor Status: To ensure compliance with tax and employment regulations, the agreement clarifies the independent contractor relationship. It confirms that the auditor is not an employee and operates their own business. The parties affirm that the auditor is responsible for their own taxes, insurance, and withholding. 3. Payment Terms: The agreement stipulates the compensation structure for the auditor's services. It outlines the agreed-upon rate, frequency of payments, and any additional expenses that may be reimbursed. It may also specify any penalties for late payments or early termination of the agreement. 4. Work Schedule and Reporting: The agreement may include details about the auditor's schedule, working hours, and reporting requirements. This ensures that both parties are aware of the expectations and agreed upon the level of availability during the engagement. Additionally, it may define the mode of communication to facilitate efficient collaboration. 5. Confidentiality and Non-Disclosure: To safeguard sensitive financial information and maintain client trust, the agreement establishes strict confidentiality obligations. It ensures that the auditor will not disclose any proprietary or confidential data obtained during the engagement or use it for personal gain. 6. Intellectual Property: If the auditor produces any reports, analysis, or other intellectual property during the engagement, ownership and usage rights must be clarified within the agreement. Typically, it stipulates that the accounting firm retains all intellectual property rights associated with the work conducted. Variations of the Hawaii Agreement: 1. Multi-Year Engagement: In cases where the accounting firm requires long-term auditing services, the agreement may incorporate a multi-year engagement clause. This outlines the duration of the agreement, the responsibilities of both parties over the duration, and any potential renegotiation terms. 2. Project-Specific Agreement: In some instances, accounting firms may contract auditors for specific projects or assignments rather than an ongoing engagement. The agreement will detail the project's objectives, deliverables, and timeline, allowing for a more targeted approach and flexibility in engagement terms. 3. Non-Competition Clause: To maintain fairness and avoid potential conflicts, the agreement may include a non-competition clause. This prevents the auditor from providing similar services to competitors of the accounting firm for a specified period after the engagement concludes. Conclusion: The Hawaii Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor is a vital legal tool that establishes a mutually beneficial relationship between accounting firms and auditors. With various types of agreements catered to specific needs, this framework enables efficient collaboration while upholding legal compliance and protecting the interests of both parties involved.Title: Hawaii Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor Introduction: In Hawaii, accounting firms often enter into agreements with auditors, employing them as self-employed independent contractors. These agreements establish the terms and conditions under which the auditor will provide their services to the accounting firm. This detailed description will provide an overview of the Hawaii Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor, highlighting its key elements and variations. Key Elements of the Hawaii Agreement: 1. Scope of Work: The agreement defines the specific services the auditor will render to the accounting firm, such as conducting audits, financial reviews, or other specialized tasks. It outlines the duration of the engagement or projects to be completed in a given period. 2. Independent Contractor Status: To ensure compliance with tax and employment regulations, the agreement clarifies the independent contractor relationship. It confirms that the auditor is not an employee and operates their own business. The parties affirm that the auditor is responsible for their own taxes, insurance, and withholding. 3. Payment Terms: The agreement stipulates the compensation structure for the auditor's services. It outlines the agreed-upon rate, frequency of payments, and any additional expenses that may be reimbursed. It may also specify any penalties for late payments or early termination of the agreement. 4. Work Schedule and Reporting: The agreement may include details about the auditor's schedule, working hours, and reporting requirements. This ensures that both parties are aware of the expectations and agreed upon the level of availability during the engagement. Additionally, it may define the mode of communication to facilitate efficient collaboration. 5. Confidentiality and Non-Disclosure: To safeguard sensitive financial information and maintain client trust, the agreement establishes strict confidentiality obligations. It ensures that the auditor will not disclose any proprietary or confidential data obtained during the engagement or use it for personal gain. 6. Intellectual Property: If the auditor produces any reports, analysis, or other intellectual property during the engagement, ownership and usage rights must be clarified within the agreement. Typically, it stipulates that the accounting firm retains all intellectual property rights associated with the work conducted. Variations of the Hawaii Agreement: 1. Multi-Year Engagement: In cases where the accounting firm requires long-term auditing services, the agreement may incorporate a multi-year engagement clause. This outlines the duration of the agreement, the responsibilities of both parties over the duration, and any potential renegotiation terms. 2. Project-Specific Agreement: In some instances, accounting firms may contract auditors for specific projects or assignments rather than an ongoing engagement. The agreement will detail the project's objectives, deliverables, and timeline, allowing for a more targeted approach and flexibility in engagement terms. 3. Non-Competition Clause: To maintain fairness and avoid potential conflicts, the agreement may include a non-competition clause. This prevents the auditor from providing similar services to competitors of the accounting firm for a specified period after the engagement concludes. Conclusion: The Hawaii Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor is a vital legal tool that establishes a mutually beneficial relationship between accounting firms and auditors. With various types of agreements catered to specific needs, this framework enables efficient collaboration while upholding legal compliance and protecting the interests of both parties involved.