The Fair Credit Reporting Act (FCRA) is designed to help ensure that credit bureaus furnish correct and complete information to businesses to use when evaluating your application. Your rights include:

The right to receive a copy of your credit report. The copy of your report must contain all of the information in your file at the time of your request.

The right to know the name of anyone who received your credit report in the last year for most purposes or in the last two years for employment purposes.

Any company that denies your application must supply the name and address of the credit bureau they contacted, provided the denial was based on information given by the credit bureau.

The right to a free copy of your credit report when your application is denied because of information supplied by the credit bureau. Your request must be made within 60 days of receiving your denial notice.

If you contest the completeness or accuracy of information in your report, you should file a dispute with the credit bureau and with the company that furnished the information to the bureau. Both the credit bureau and the furnisher of information are legally obligated to investigate your dispute.

A right to add a summary explanation to your credit report if your dispute is not resolved to your satisfaction.

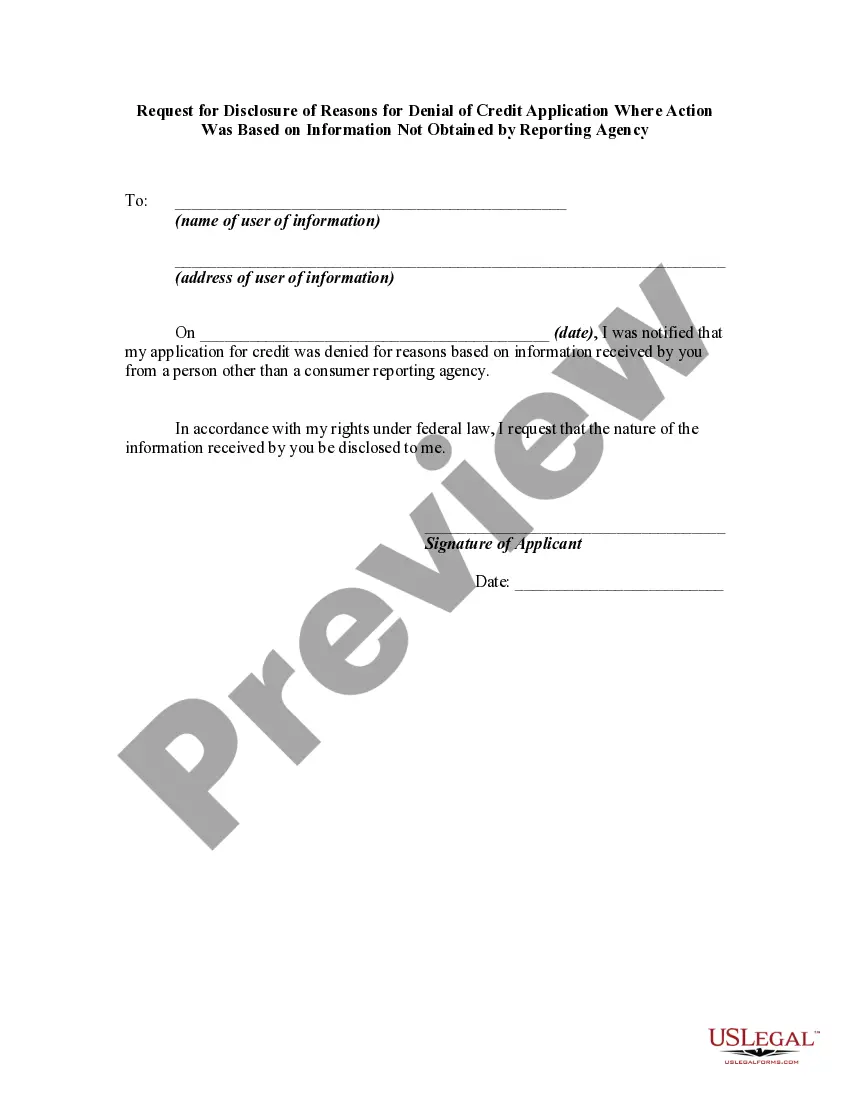

Hawaii Request for Disclosure of Reasons for Denial of Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency If you have been denied credit in Hawaii and believe that the decision was made based on information not obtained by the reporting agency, you have the right to request disclosure of the reasons behind this denial. This request can help you understand why your credit application was denied and allow you to take appropriate action to rectify any errors or inaccuracies. There are several situations in which you might need to submit a Hawaii Request for Disclosure of Reasons for Denial of Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency. Let's explore them: 1. Denial due to missing information: Sometimes, credit applications are denied because of incomplete or missing information. The lender may not have received all the required documentation or details necessary to assess your creditworthiness. In such cases, you can submit this request to understand what specific information was required and how you can provide it. 2. Denial due to outdated information: If information about your credit history, employment status, or personal details has changed, but the reporting agency has not updated it, your credit application might be denied. Requesting disclosure of the reasons will enable you to identify outdated information that needs to be corrected or updated. 3. Denial based on incorrect information: Credit reports may sometimes contain errors or inaccuracies, resulting in a denial of credit. These errors can range from identity theft to incorrect account balances or payment history. By filing a request for disclosure, you can pinpoint the incorrect information and take steps to rectify it with the relevant reporting agency. 4. Denial due to negative credit history: Your credit application might be rejected based on negative information in your credit report, such as late payments, defaults, or bankruptcy. However, if the reporting agency did not obtain this information from valid sources or failed to follow proper procedures, you can submit a request for disclosure to understand the specific sources they relied upon. This will help you determine if any incorrect or unauthorized information influenced their decision. 5. Denial based on lack of consent: Lenders and reporting agencies require your consent to access and evaluate your credit history. If the denial of your credit application occurred because the reporting agency obtained information without your consent, you have the right to request disclosure of the reasons and take appropriate action against the responsible parties. Submitting a Hawaii Request for Disclosure of Reasons for Denial of Credit Application Where Action Was Based on Information Not Obtained by the Reporting Agency can be crucial in understanding the factors that led to the denial of your credit application. By obtaining this information, you can take the necessary steps to correct any errors, update outdated information, or resolve any unauthorized access issues, ultimately improving your chances of obtaining credit in the future.