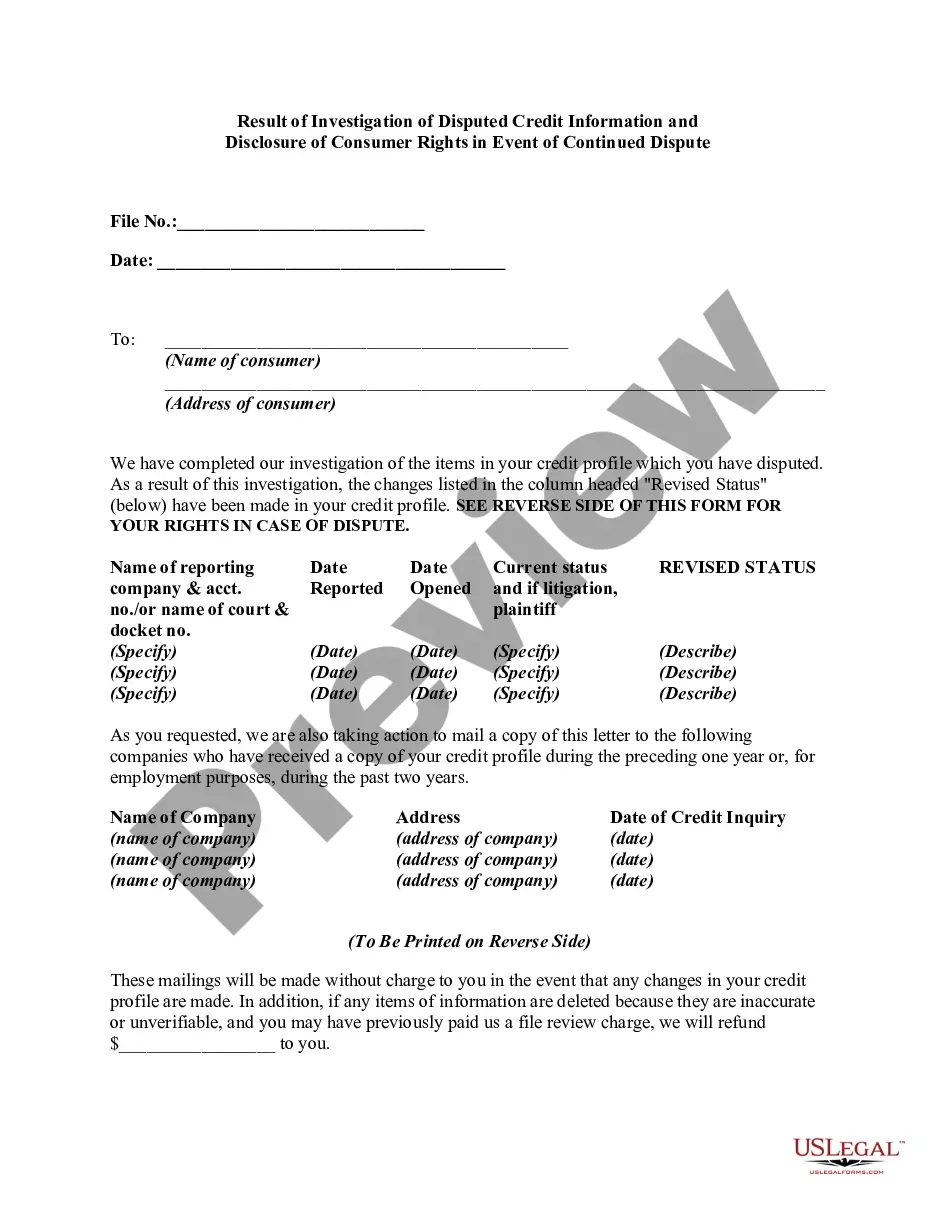

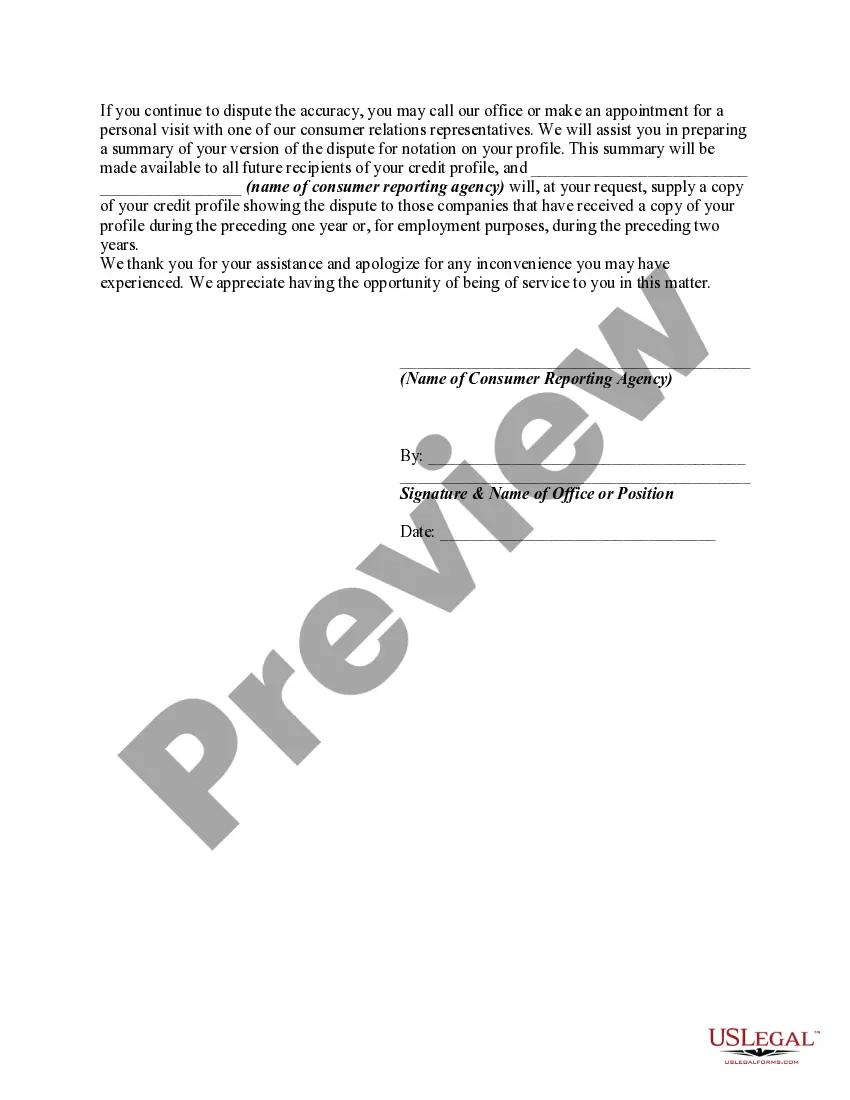

Under the Fair Credit Reporting Act, if a consumer disputes the completeness or accuracy of any item of information in the consumer's file, and the dispute is directly conveyed to the consumer reporting agency by the consumer, the reporting agency must, free of charge, conduct a reasonable reinvestigation to determine whether the disputed information is inaccurate, unless it has reasonable grounds to believe that the dispute is frivolous or irrelevant. If the information is erroneous, inaccurate, or can no longer be verified, the credit reporting agency must promptly correct or delete it and refrain from reporting the information in subsequent consumer reports.

Following any deletion of information or notation as to disputed information, the agency, on request of the consumer, must furnish to certain persons either: (1) notification of the deletion; or (2) the consumer's statement of the dispute or the agency's summary of the statement. The consumer reporting agency must clearly and conspicuously disclose the consumer's rights to make such a request, such disclosure to be made at or prior to the time the information is deleted or the consumer's statement regarding the disputed information is received.

Title: Understanding Hawaii's Result of Investigation of Disputed Credit Information and Consumer Rights in Ongoing Disputes Introduction: Investigating disputed credit information is crucial for maintaining fair and accurate credit reports. In Hawaii, the law outlines the procedure for investigating disputed credit information and provides consumers with specific rights in the event of a continued dispute. This comprehensive guide delves into the details of Hawaii's result of investigation of disputed credit information and highlights important consumer rights. Key Concepts: Hawaii's Result of Investigation of Disputed Credit Information 1. Investigation Process: When a consumer disputes credit information in Hawaii, the relevant credit reporting agency initiates an investigation to determine the accuracy and legitimacy of the disputed items. The following steps are typically followed: a. Notification: The credit reporting agency must notify the consumer about the investigation within five business days of receiving the dispute. b. Verification: The agency contacts the entity or creditor responsible for reporting the disputed information, requesting verification of its accuracy. c. Reporting Timeframe: Credit reporting agencies generally have 30 days to complete the investigation and inform the consumer about the outcome. 2. Result of the Investigation: After conducting a thorough investigation, the credit reporting agency in Hawaii will provide the consumer with a detailed result. The possible outcomes include: a. Accurate Information: If the investigation confirms the accuracy of the disputed credit information, the agency will notify the consumer about the investigation result, indicating that the reported item(s) will remain on the credit report. b. Inaccurate Information: In case the investigation determines that the disputed information is inaccurate, the credit reporting agency must take necessary steps to rectify the inaccuracies. This may involve updating or deleting the incorrect items from the credit report. Consumer Rights in Event of Continued Dispute: 1. Notice of Dispute Reiteration: If the consumer disagrees with the result of the investigation and continues to dispute the credit information, they have the right to reiterate their claim. The law encourages consumers to provide any additional evidence or documentation to support their dispute. 2. Disclosure of Consumer Rights: Hawaii consumer protection laws ensure that credit reporting agencies provide written notice to consumers about their rights if the dispute remains unresolved. This notice must include the following: a. Consumer Statement: Consumers have the right to include a personal statement in their credit reports, explaining their position and providing context regarding the disputed items. b. File with the Commissioner: Consumers can file a complaint with the Hawaii Commissioner of Financial Institutions if they believe the credit reporting agency acted unlawfully or failed to properly investigate the dispute. c. Legal Remedies: Consumers retain the right to take legal action against credit reporting agencies that fail to comply with state and federal laws while investigating and reporting credit information. Conclusion: Understanding Hawaii's result of investigation of disputed credit information and consumer rights is essential for anyone involved in credit disputes. By knowing the investigation process and their rights in ongoing disputes, consumers can actively participate in ensuring the accuracy and fairness of their credit reports.Title: Understanding Hawaii's Result of Investigation of Disputed Credit Information and Consumer Rights in Ongoing Disputes Introduction: Investigating disputed credit information is crucial for maintaining fair and accurate credit reports. In Hawaii, the law outlines the procedure for investigating disputed credit information and provides consumers with specific rights in the event of a continued dispute. This comprehensive guide delves into the details of Hawaii's result of investigation of disputed credit information and highlights important consumer rights. Key Concepts: Hawaii's Result of Investigation of Disputed Credit Information 1. Investigation Process: When a consumer disputes credit information in Hawaii, the relevant credit reporting agency initiates an investigation to determine the accuracy and legitimacy of the disputed items. The following steps are typically followed: a. Notification: The credit reporting agency must notify the consumer about the investigation within five business days of receiving the dispute. b. Verification: The agency contacts the entity or creditor responsible for reporting the disputed information, requesting verification of its accuracy. c. Reporting Timeframe: Credit reporting agencies generally have 30 days to complete the investigation and inform the consumer about the outcome. 2. Result of the Investigation: After conducting a thorough investigation, the credit reporting agency in Hawaii will provide the consumer with a detailed result. The possible outcomes include: a. Accurate Information: If the investigation confirms the accuracy of the disputed credit information, the agency will notify the consumer about the investigation result, indicating that the reported item(s) will remain on the credit report. b. Inaccurate Information: In case the investigation determines that the disputed information is inaccurate, the credit reporting agency must take necessary steps to rectify the inaccuracies. This may involve updating or deleting the incorrect items from the credit report. Consumer Rights in Event of Continued Dispute: 1. Notice of Dispute Reiteration: If the consumer disagrees with the result of the investigation and continues to dispute the credit information, they have the right to reiterate their claim. The law encourages consumers to provide any additional evidence or documentation to support their dispute. 2. Disclosure of Consumer Rights: Hawaii consumer protection laws ensure that credit reporting agencies provide written notice to consumers about their rights if the dispute remains unresolved. This notice must include the following: a. Consumer Statement: Consumers have the right to include a personal statement in their credit reports, explaining their position and providing context regarding the disputed items. b. File with the Commissioner: Consumers can file a complaint with the Hawaii Commissioner of Financial Institutions if they believe the credit reporting agency acted unlawfully or failed to properly investigate the dispute. c. Legal Remedies: Consumers retain the right to take legal action against credit reporting agencies that fail to comply with state and federal laws while investigating and reporting credit information. Conclusion: Understanding Hawaii's result of investigation of disputed credit information and consumer rights is essential for anyone involved in credit disputes. By knowing the investigation process and their rights in ongoing disputes, consumers can actively participate in ensuring the accuracy and fairness of their credit reports.