A secured transaction is created when a buyer or borrower (debtor) grants a seller or lender (creditor or secured party) a security interest in personal property (collateral). A security interest allows a creditor to repossess and sell the collateral if a debtor fails to pay a secured debt.

The Truth-in-Lending Act (TILA) is part of the Federal Consumer Credit Protection Act. The purpose of the TILA is to make full disclosure to debtors of what they are being charged for the credit they are receiving. The Act merely asks lenders to be honest to the debtors and not cover up what they are paying for the credit. Regulation Z is a federal regulation prepared by the Federal Reserve Board to carry out the details of the Act. TILA applies to consumer credit transactions. Consumer credit is credit for personal or household use and not commercial use or business purposes.

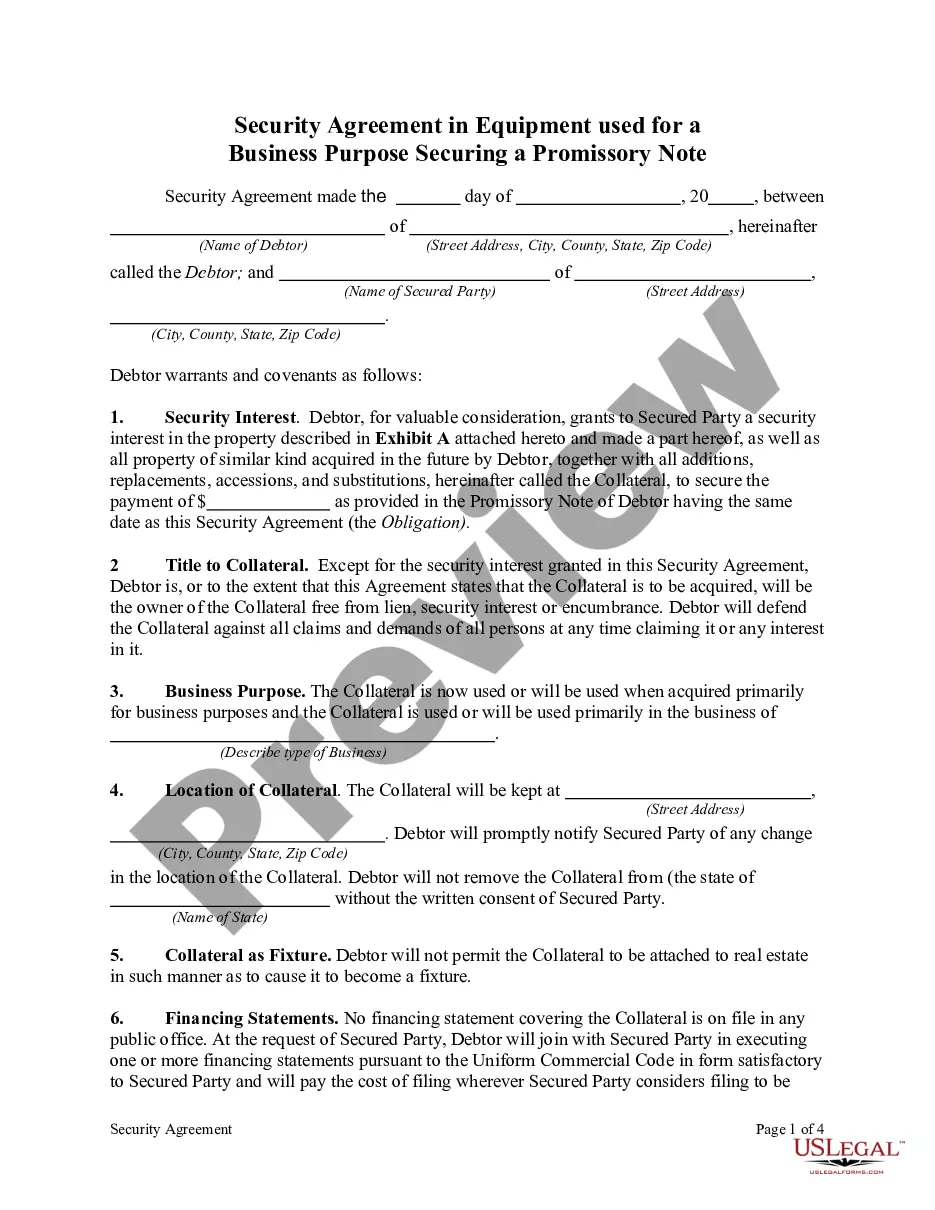

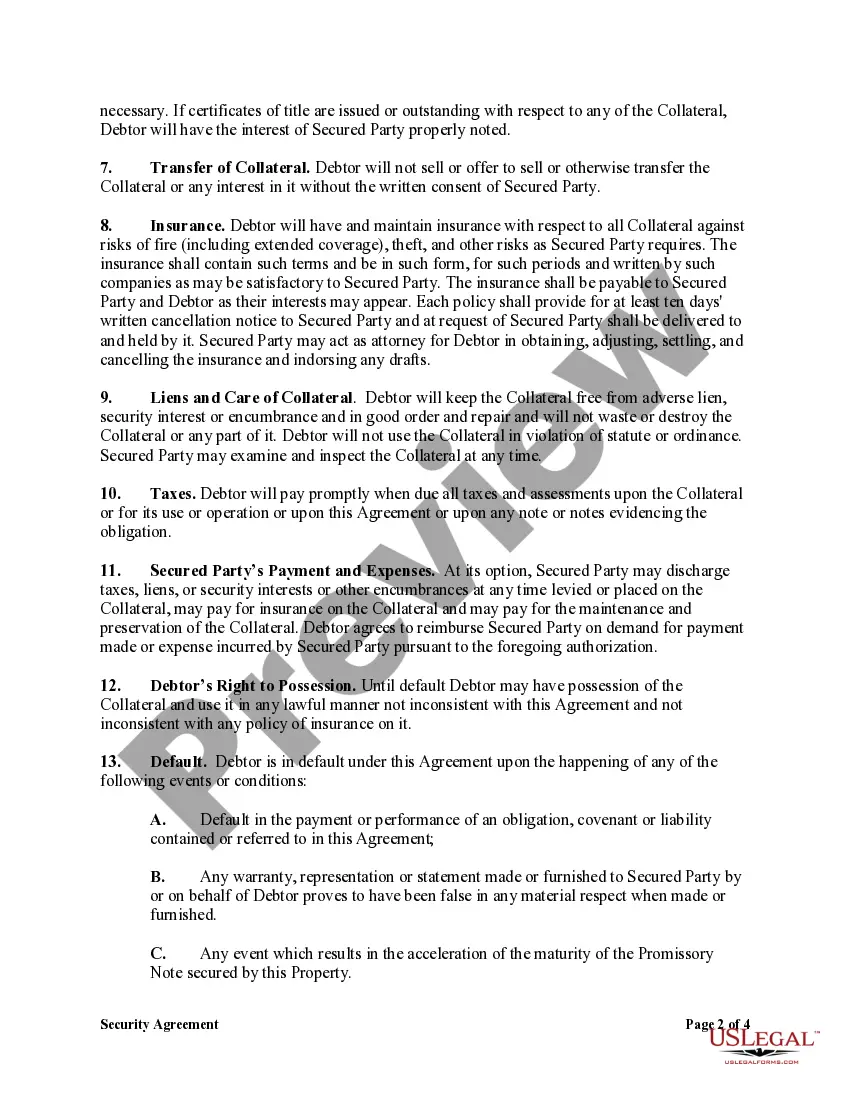

A Hawaii Security Agreement in Equipment for Business Purposes is a legally binding contract that outlines the terms and conditions surrounding the use of equipment as collateral for a business promissory note. This agreement ensures that the lender has a security interest in the equipment, allowing them to repossess or sell it in the event of default by the borrower. The agreement typically includes details such as the borrower's name, address, and contact information, as well as the lender's name and contact information. It also specifies the equipment being used as collateral, describing it in detail, including make, model, serial number, and any other identifying features. Additionally, the agreement will outline the exact dollar amount of the promissory note and the agreed-upon repayment terms, including the interest rate, payment schedule, and due dates. The purpose of a Hawaii Security Agreement in Equipment for Business Purposes is to protect the lender's investment and ensure that they have a means of recovering their funds if the borrower defaults on the loan. By securing the promissory note with collateral, the lender has an added layer of protection, reducing the risk associated with lending to businesses. There are different types of Hawaii Security Agreement in Equipment for Business Purposes, which may vary depending on the specific industry or circumstances. Some common variations include: 1. Fixed-term Security Agreement: This type of agreement specifies a set term for the loan repayment and the duration of the security interest in the equipment. Once the loan is repaid in full, the security interest is released, and the borrower regains full ownership of the equipment. 2. Floating Security Agreement: In this type of agreement, the security interest "floats" over various equipment, allowing the borrower to replace or add new equipment without needing to update the agreement. The lender's security interest automatically shifts to the newly added equipment, provided it meets certain criteria outlined in the agreement. 3. Purchase Money Security Agreement (PSI): This agreement applies when the lender provides funds specifically for the purchase of equipment. The lender's security interest takes priority over any other claims against the equipment, offering additional protection in case of default. It is crucial for both lenders and borrowers in Hawaii to understand the terms outlined in a Security Agreement in Equipment for Business Purposes — Securing Promissory Note. Seeking legal advice and having a comprehensive understanding of the agreement's implications can ensure a smooth and secure financing transaction for all parties involved.