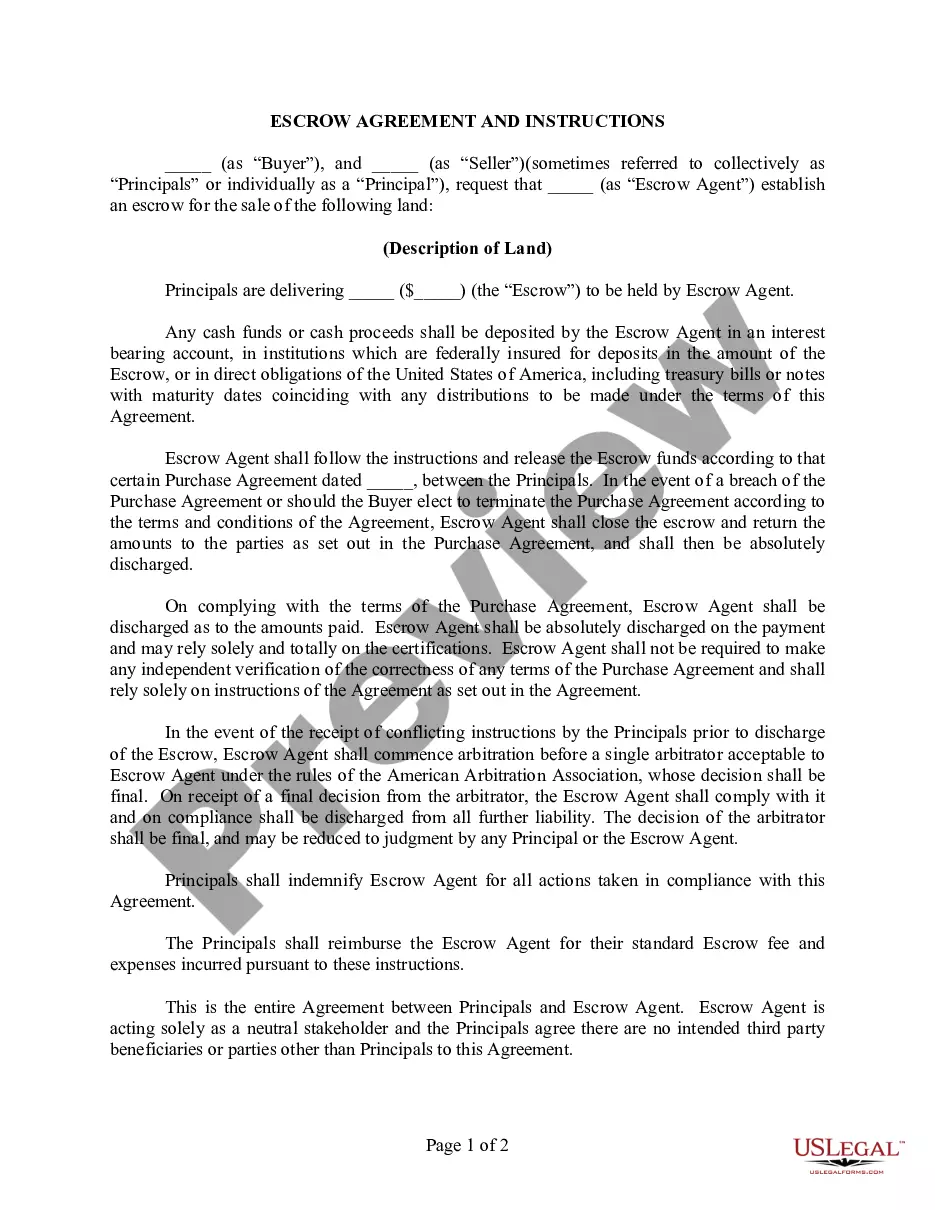

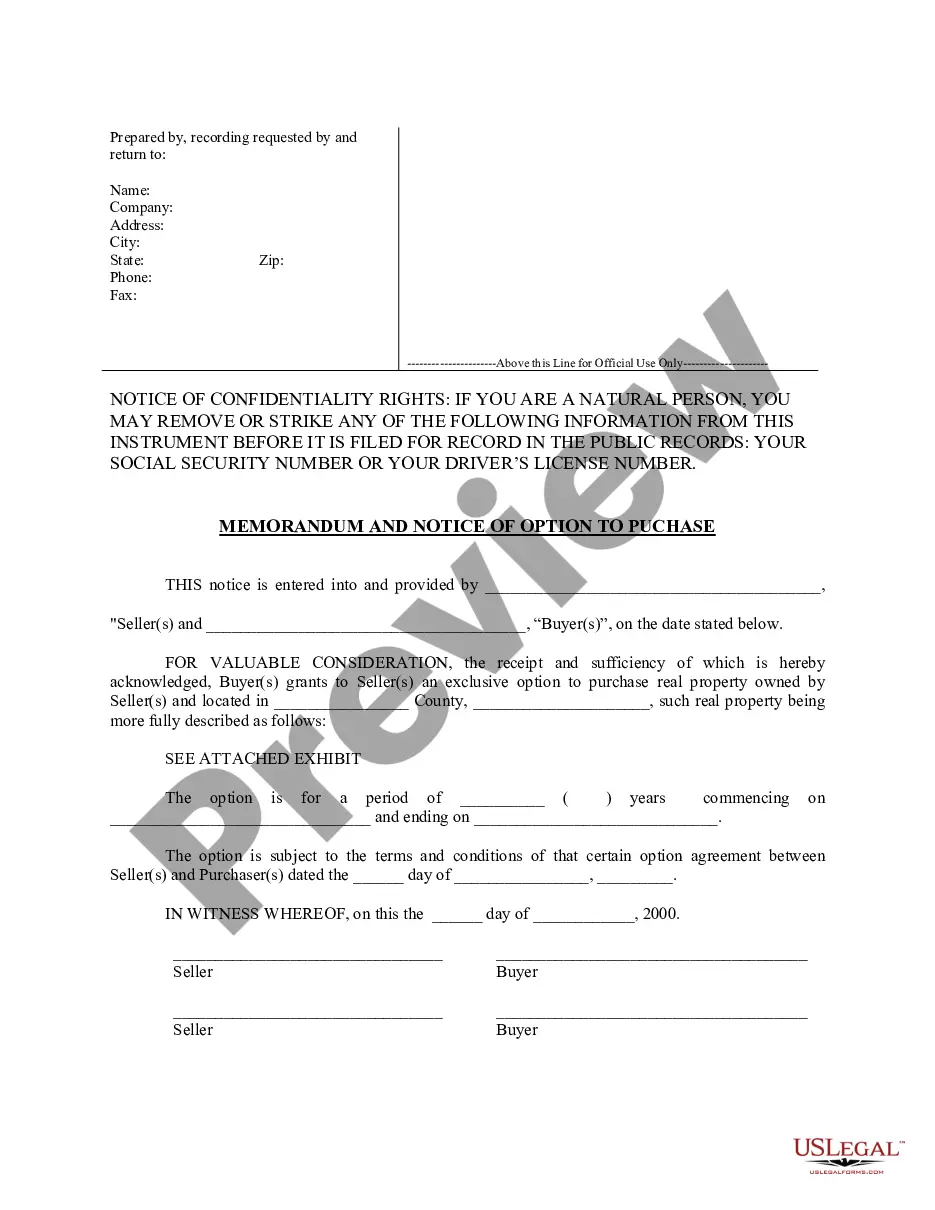

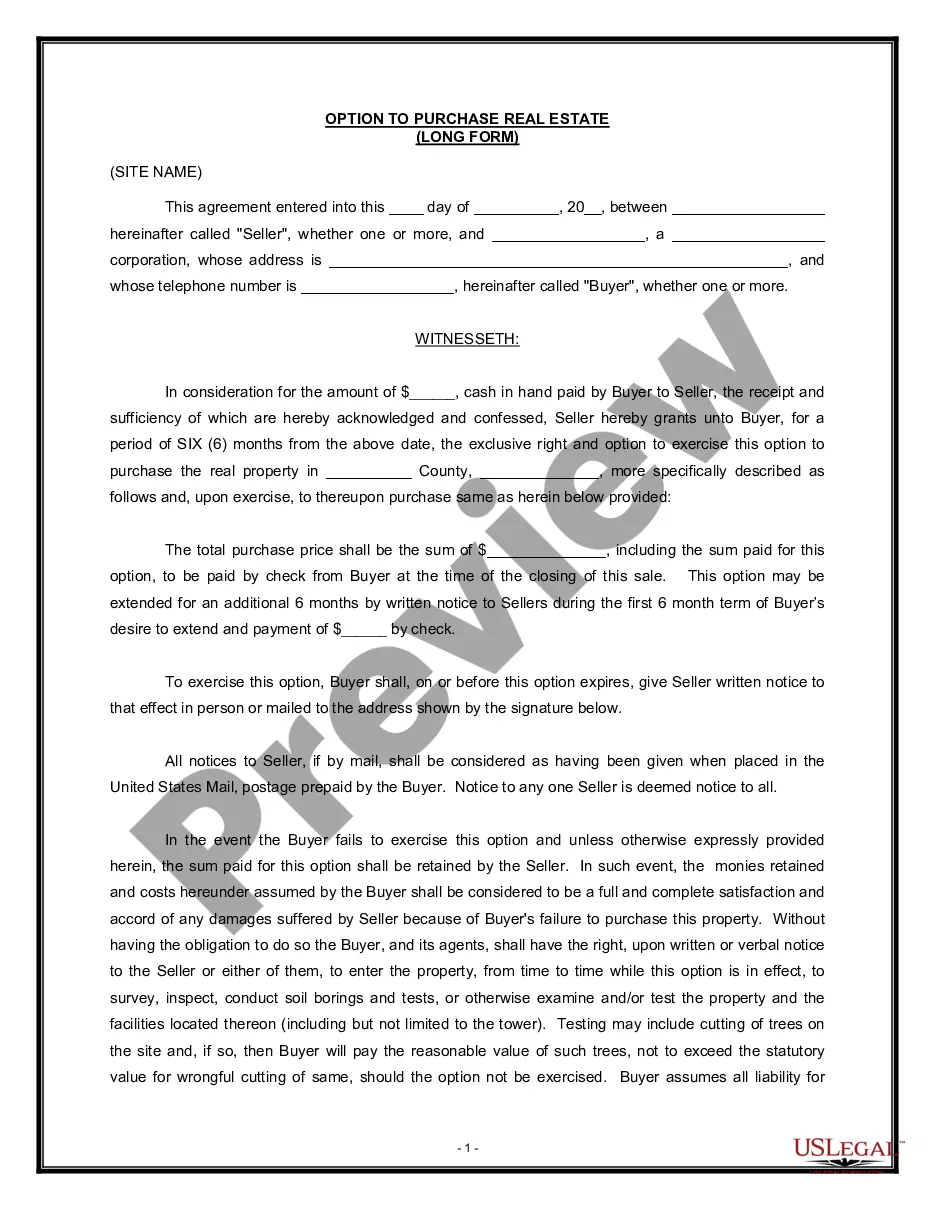

The Truth-in-Lending Act (TILA) is part of the Federal Consumer Credit Protection Act. The purpose of the TILA is to make full disclosure to debtors of what they are being charged for the credit they are receiving. TILA applies only to consumer credit transactions. Consumer credit is credit for personal or household use and not commercial use. This form was designed to cover an situation where the Seller is not a creditor as defined by the TILA.

Hawaii Installment Sale not covered by Federal Consumer Credit Protection Act with Security Agreement

Instant download

Description

Free preview

How to fill out Installment Sale Not Covered By Federal Consumer Credit Protection Act With Security Agreement?

If you want to download, download, or print legal document templates, use US Legal Forms, the foremost variety of legal forms, which are available online.

Utilize the site's user-friendly and convenient search to obtain the documents you need.

Various templates for business and personal purposes are categorized by types and states, or keywords.

Step 5. Complete the payment. You can use your Visa or Mastercard or PayPal account to finish the transaction.

Step 6. Choose the format of your legal form and download it to your system. Step 7. Complete, edit, and print or sign the Hawaii Installment Sale not covered by Federal Consumer Credit Protection Act with Security Agreement.

- Use US Legal Forms to obtain the Hawaii Installment Sale not included in the Federal Consumer Credit Protection Act with Security Agreement in just a few clicks.

- If you are already a US Legal Forms customer, Log In to your account and then click the Get button to obtain the Hawaii Installment Sale not included in the Federal Consumer Credit Protection Act with Security Agreement.

- You can also access forms you previously downloaded in the My documents tab of your account.

- If this is your first time using US Legal Forms, follow the instructions below.

- Step 1. Ensure you have selected the form for the correct city/state.

- Step 2. Use the Preview option to review the form's content. Don't forget to read the information.

- Step 3. If you are dissatisfied with the form, use the Search box at the top of the screen to find other forms of your legal form type.

- Step 4. Once you have located the form you need, click the Get now button. Choose the pricing plan you prefer and enter your details to create an account.

Form popularity

FAQ

Certain transactions in Hawaii are exempt from the general excise tax, including some types of sales to nonprofit entities and specific agricultural sales. Additionally, exemptions may apply to income derived from certain types of business activities. It's beneficial to explore how a Hawaii Installment Sale not covered by Federal Consumer Credit Protection Act with Security Agreement could potentially impact your general excise tax obligations.

To obtain penalty abatement in Hawaii, you typically need to demonstrate reasonable cause for late payments or filings. Submitting a well-documented request along with your tax return can help, showing evidence of circumstances that led to the issues. Utilizing a Hawaii Installment Sale not covered by Federal Consumer Credit Protection Act with Security Agreement may also assist in addressing financial difficulties, making abatement a more feasible option.

In Hawaii, a non-refundable credit generally refers to a credit against taxes owed, which cannot be refunded if it exceeds your tax obligation. Common examples include credits for income taxes or certain business expenses. Understanding how non-refundable credits may apply in scenarios such as a Hawaii Installment Sale not covered by Federal Consumer Credit Protection Act with Security Agreement is key for effective tax planning.

Certain homeowners may be exempt from capital gains tax on their real estate sales in Hawaii, particularly those who meet the primary residence exclusion criteria. If you have lived in the home for at least two of the last five years, you might qualify to exclude up to $250,000 in capital gains from taxation, or up to $500,000 if filing jointly. It is beneficial to evaluate how a Hawaii Installment Sale not covered by Federal Consumer Credit Protection Act with Security Agreement impacts your tax exemptions.

In Hawaii, the capital gains tax on home sales follows federal guidelines, with rates typically aligned with 0%, 15%, or 20% based on the seller's income. The exact amount can vary, depending on how long the property was owned and whether you qualify for any exclusions. Engaging in a Hawaii Installment Sale not covered by Federal Consumer Credit Protection Act with Security Agreement can also influence your capital gains situation, so considerations should be made with the help of a professional.

In general, the capital gains tax rate can either be 15% or 20%, depending on your income level. For most taxpayers, the rate is 15%. However, if your income exceeds specific thresholds, you may be subjected to the higher 20% rate. It's essential to consult a tax professional to determine your exact rate based on your individual circumstances, especially when considering a Hawaii Installment Sale not covered by Federal Consumer Credit Protection Act with Security Agreement.

In most cases, you will need a General Excise (GE) license to conduct business in Hawaii. This license is essential for any entity earning income from business activities within the state. If you are entering into a Hawaii Installment Sale not covered by Federal Consumer Credit Protection Act with Security Agreement, obtaining a GE license may be required, especially if you manage a business selling goods or services. It's advisable to consult the uslegalforms platform for insights on licensing requirements tailored to your needs.

To become tax exempt in Hawaii, you need to follow specific guidelines established by the state. You typically must submit an exemption application along with the necessary documentation to demonstrate eligibility, such as proof of nonprofit status or use of vehicles for specific exempt purposes. Engaging in a Hawaii Installment Sale not covered by Federal Consumer Credit Protection Act with Security Agreement can help navigate these requirements more effectively. Consider visiting the uslegalforms platform for detailed assistance with the application process.

Certain vehicles in Hawaii are exempt from excise tax under specific conditions. For instance, vehicles used solely for agriculture or nonprofit purposes may qualify for this exemption. Additionally, if you engage in a Hawaii Installment Sale not covered by Federal Consumer Credit Protection Act with Security Agreement, you might find particular benefits related to tax exemptions. It’s essential to review the state laws or consult with a tax professional to determine your specific eligibility.