Gift taxes are taxes that supplement the Estate Tax. Gift taxes are placed on gifts given away to any person while you are still living, so that you may not avoid estate taxes by making gifts of your estate. You may give up to $12,000 a year in cash or assets to an unlimited number of people each year without incurring gift tax liability, but the gifts must have no conditions attached. Married couples can give, as a couple, a $24,000 gift per year to as many people as they want. Under federal tax law, gifts totaling more than $12,000 to one person in one year are considered a taxable gift and generate a potential gift tax. It does not matter if you give one $13,000 gift or 13 gifts of $1,000 each, or one gift of $12,000 and a "birthday gift" of $1,000.

Gifts beyond the $12,000 limit (there is an exception for gifts that are directly paid by the gift giver for tuition and medical expenses) are considered "taxable gifts." Taxable gifts create liability for a gift tax. But gift tax is not due to be paid until you give away over $1,000,000 in your lifetime.

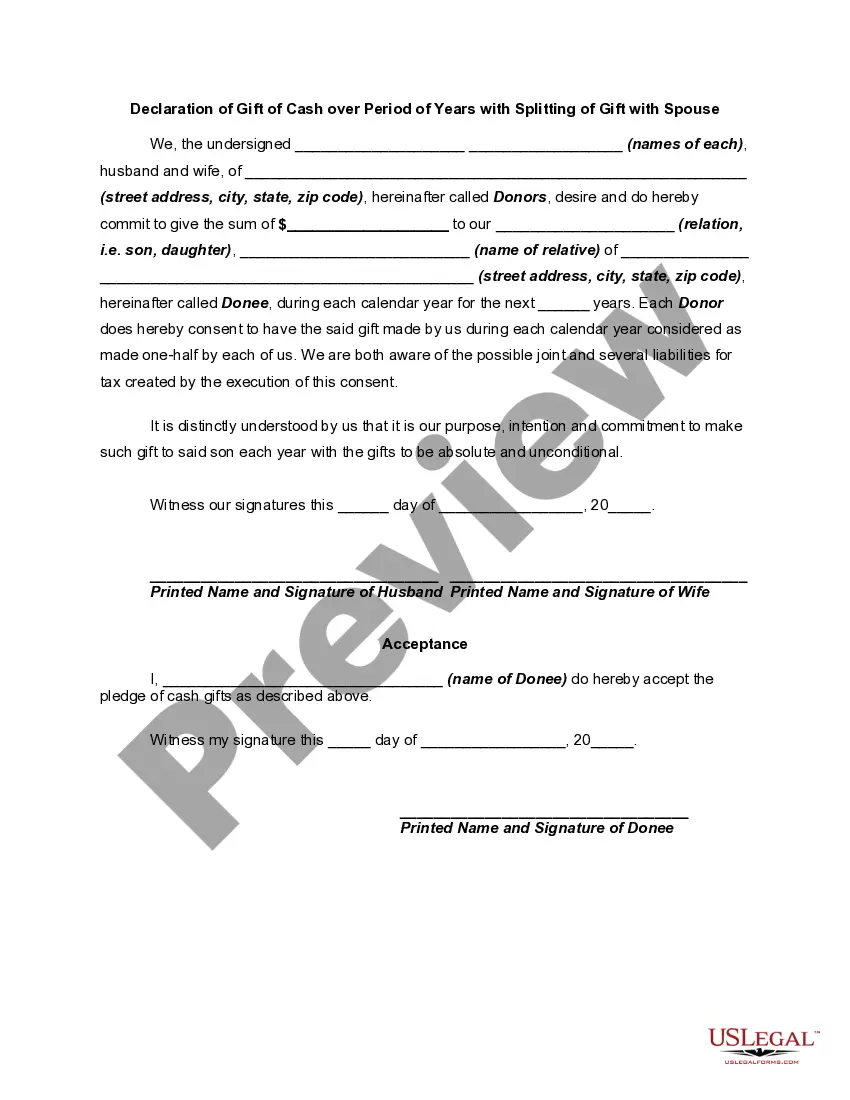

The Hawaii Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse is a legal document that allows individuals to make charitable donations to organizations or individuals over a specific time period while also splitting the gift with their spouse. This unique declaration enables the donor to have control over their charitable giving and involve their spouse in the decision-making process. Keywords: Hawaii, Declaration of Gift, Cash, Period of Years, Splitting of Gift, Spouse, Charitable donations, Legal document, Control, Decision-making. Two types of Hawaii Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse: 1. Individual Hawaii Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse: This type is used when an individual wishes to make a charitable gift over a period of years and involve their spouse in splitting the gift. It allows both partners to contribute to the donation and provides a legally binding framework for the process. 2. Joint Hawaii Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse: This type is used when spouses jointly decide to make charitable donations over a specified time period. Both partners actively participate in the gift splitting, allowing them to combine their resources and strengthen their impact on the chosen charitable cause. In both types, the Hawaii Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse outlines the terms and conditions of the gift, including the duration, monetary amounts, and any restrictions or specifications the donors want to impose. The declaration serves as a formal agreement between the donors, their chosen charitable organization or individual, and any other relevant parties involved such as legal representatives or financial advisors. By utilizing the Hawaii Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse, individuals and couples in Hawaii can ensure that their charitable giving aligns with their values, maximizes their impact, and involves their spouse in the decision-making process. This allows for a more thoughtful and coordinated approach to giving, benefiting both the donors and the chosen cause or recipient.The Hawaii Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse is a legal document that allows individuals to make charitable donations to organizations or individuals over a specific time period while also splitting the gift with their spouse. This unique declaration enables the donor to have control over their charitable giving and involve their spouse in the decision-making process. Keywords: Hawaii, Declaration of Gift, Cash, Period of Years, Splitting of Gift, Spouse, Charitable donations, Legal document, Control, Decision-making. Two types of Hawaii Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse: 1. Individual Hawaii Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse: This type is used when an individual wishes to make a charitable gift over a period of years and involve their spouse in splitting the gift. It allows both partners to contribute to the donation and provides a legally binding framework for the process. 2. Joint Hawaii Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse: This type is used when spouses jointly decide to make charitable donations over a specified time period. Both partners actively participate in the gift splitting, allowing them to combine their resources and strengthen their impact on the chosen charitable cause. In both types, the Hawaii Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse outlines the terms and conditions of the gift, including the duration, monetary amounts, and any restrictions or specifications the donors want to impose. The declaration serves as a formal agreement between the donors, their chosen charitable organization or individual, and any other relevant parties involved such as legal representatives or financial advisors. By utilizing the Hawaii Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse, individuals and couples in Hawaii can ensure that their charitable giving aligns with their values, maximizes their impact, and involves their spouse in the decision-making process. This allows for a more thoughtful and coordinated approach to giving, benefiting both the donors and the chosen cause or recipient.