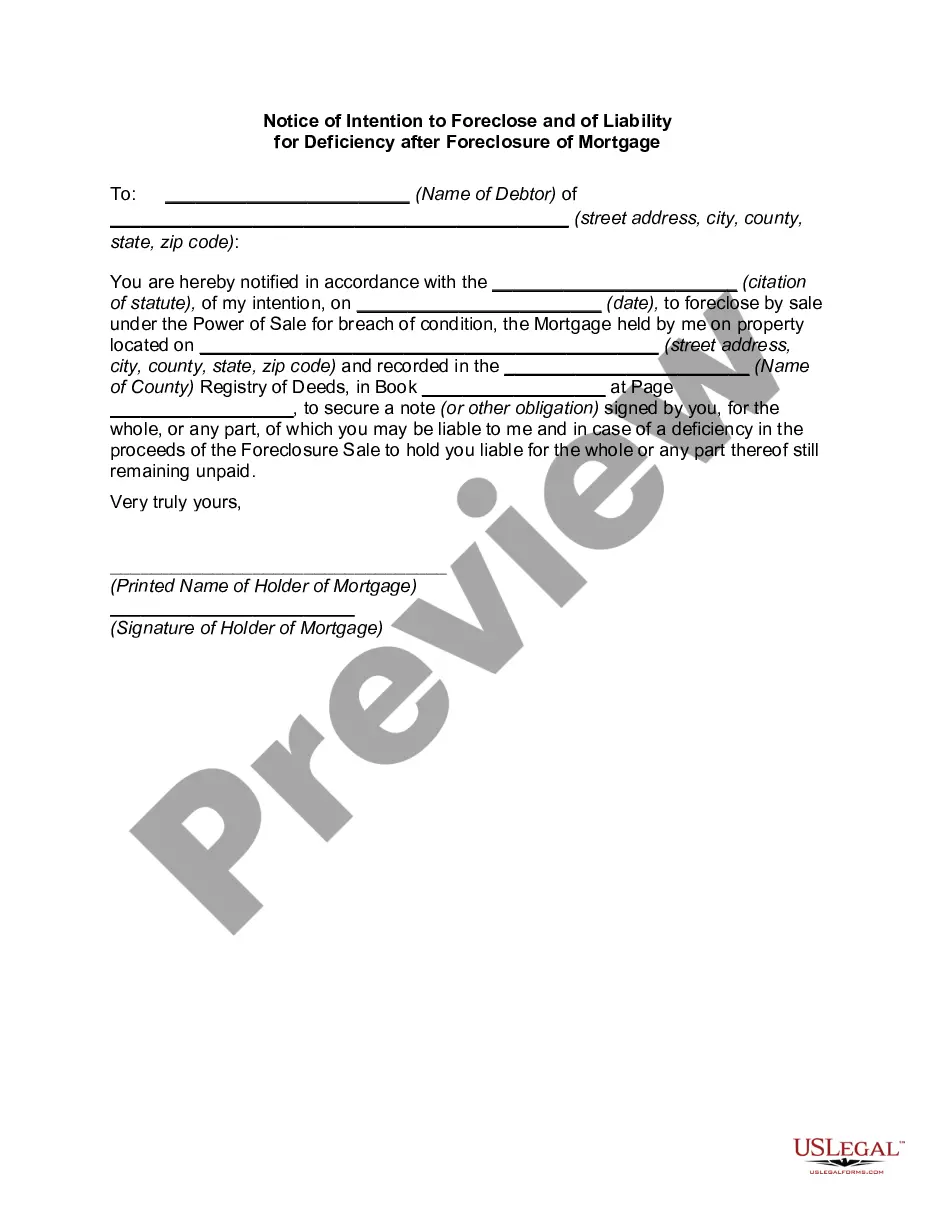

A number of states have enacted measures to facilitate greater communication between borrowers and lenders by requiring mortgage servicers to provide certain notices to defaulted borrowers prior to commencing a foreclosure action. The measures serve a dual purpose, providing more meaningful notice to borrowers of the status of their loans and slowing down the rate of foreclosures within these states. For instance, one state now requires a mortgagee to mail a homeowner a notice of intent to foreclose at least 45 days before initiating a foreclosure action on a loan. The notice must be in writing, and must detail all amounts that are past due and any itemized charges that must be paid to bring the loan current, inform the homeowner that he or she may have options as an alternative to foreclosure, and provide contact information of the servicer, HUD-approved foreclosure counseling agencies, and the state Office of Commissioner of Banks.

Hawaii Notice and Demand to Mortgagor regarding Intent to Foreclose

Description

How to fill out Notice And Demand To Mortgagor Regarding Intent To Foreclose?

Are you currently in a situation where you frequently need documents for both professional or personal purposes.

There are many reliable document templates available online, but finding ones you can trust is not easy.

US Legal Forms provides thousands of templates, including the Hawaii Notice and Demand to Mortgagor regarding Intent to Foreclose, which can be downloaded to comply with federal and state regulations.

Once you find the correct template, click on Buy now.

Select the pricing plan you want, provide the necessary information to create your account, and pay for your order using PayPal or credit card. Choose a convenient document format and download your copy. Retrieve all templates you have purchased in the My documents section. You can obtain an additional copy of the Hawaii Notice and Demand to Mortgagor regarding Intent to Foreclose anytime, if needed. Just follow the necessary form to download or print the document template. Utilize US Legal Forms, the most comprehensive collection of legitimate forms, to save time and prevent errors. The service provides properly crafted legal document templates that can be used for various purposes. Create your account on US Legal Forms and begin simplifying your life.

- If you are already familiar with the US Legal Forms website and have an account, simply Log In.

- Then, you can download the Hawaii Notice and Demand to Mortgagor regarding Intent to Foreclose template.

- If you don’t have an account and want to start using US Legal Forms, follow these steps.

- Find the template you need and ensure it is for the correct city/region.

- Use the Preview option to view the form.

- Check the description to confirm you have selected the right template.

- If the template is not what you are looking for, use the Search field to find the template that fits your requirements.

Form popularity

FAQ

A letter of intent for foreclosure serves as an official communication indicating a lender's intention to initiate foreclosure proceedings. It typically includes the details outlined in the Hawaii Notice and Demand to Mortgagor regarding Intent to Foreclose. This document gives the mortgagor a chance to address the underlying issues before the foreclosure progresses. Understanding this letter can help mortgagors take necessary actions to prevent further complications.

To stop the intent to foreclose, you must address the notice promptly. First, review the Hawaii Notice and Demand to Mortgagor regarding Intent to Foreclose to understand the specifics of your situation. Then, consider reaching out to your lender to discuss payment options or modifications. Additionally, you may want to explore legal resources to ensure you protect your rights during this process.

Receiving a foreclosure letter can be distressing, but it's important to act quickly. Review the letter carefully and reach out to your lender to discuss options. You may want to explore legal assistance or resources, such as those provided by uslegalforms, which can guide you in understanding your rights. The Hawaii Notice and Demand to Mortgagor regarding Intent to Foreclose outlines your options and next steps clearly.

Generally, lenders begin the foreclosure process after a borrower has missed three monthly payments. However, each lender can have different timelines, making it essential to read your mortgage agreement. The Hawaii Notice and Demand to Mortgagor regarding Intent to Foreclose typically follows this pattern. Staying informed about your payment status can help you avoid reaching the foreclosure stage.

A demand letter is typically used to request payment or action from an individual or entity. In the context of mortgages, it communicates the lender's intent to take further legal action if the borrower does not respond. The Hawaii Notice and Demand to Mortgagor regarding Intent to Foreclose may be issued as a demand letter to start the foreclosure process. Using a structured approach, like the options available at uslegalforms, can simplify this task.

A notice of default and a demand letter are not the same, although they serve related purposes. The notice of default signals that a borrower has missed payments and outlines the consequences, while a demand letter requests immediate payment of the overdue amount. The Hawaii Notice and Demand to Mortgagor regarding Intent to Foreclose can sometimes emphasize these issues. Understanding the difference helps you respond appropriately.

The six phases of foreclosure generally include the notice of default, the waiting period, the auction, the post-auction period, possible redemption, and the transfer of ownership. Each of these steps reflects a crucial stage in the foreclosure process, and understanding them can provide clarity for borrowers. Utilizing resources such as the Hawaii Notice and Demand to Mortgagor regarding Intent to Foreclose can aid in navigating these phases effectively.

The timeline for foreclosure in Hawaii can vary significantly, typically taking anywhere from several months to over a year. Many factors can influence this duration, including court schedules and decisions made by mortgage lenders. Understanding these timelines and seeking assistance, such as the Hawaii Notice and Demand to Mortgagor regarding Intent to Foreclose, can help borrowers navigate this complex process.

The notice of intention to foreclose is a formal declaration from the lender indicating that they plan to take legal action to reclaim the property due to unpaid mortgage obligations. In Hawaii, this notice often includes essential details about the borrower's account and the timeline of actions to follow. It is crucial for borrowers to respond appropriately upon receiving this notice to explore possible resolutions.

A letter of intent to foreclosure is a document that signals a lender's intention to begin the foreclosing process against a borrower. This letter typically includes details about the delinquency, provides a timeline, and may outline potential remedies available to the borrower. Understanding this letter is vital for anyone facing foreclosure, and resources like the Hawaii Notice and Demand to Mortgagor regarding Intent to Foreclose can provide further clarity.