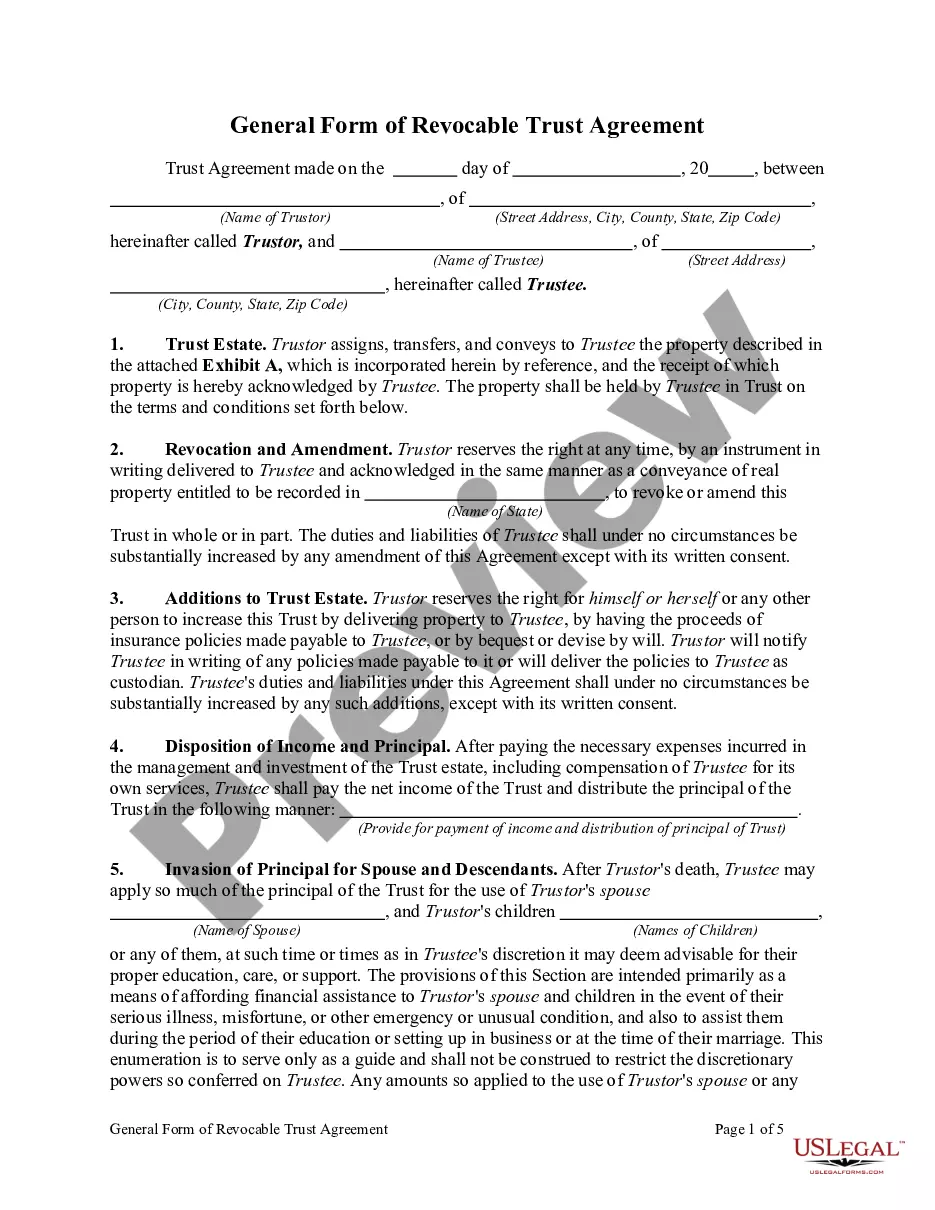

A trust is a fiduciary relationship in which one party holds legal title to another's property for the benefit of a party who holds equitable title to the property. An inter vivos trust is a trust that becomes effective during the lifetime of the person creating the trust (the settler or trustor).

A qualified terminable interest property trust, often referred to as a "QTIP" trust, allows a bequest to a spouse in trust that, after a proper election by the beneficiary spouse, qualifies for the unlimited marital deduction:

" if the beneficiary spouse is entitled to all of the income from the trust property,

" if the income is payable annually or at more frequent intervals, and

" if no person, including the beneficiary spouse, has the power to appoint any part of the qualifying property to any person other than the beneficiary spouse during the beneficiary spouse's lifetime.

In order that the property transferred to a surviving spouse by means of an inter vivos marital deduction trust qualify for the marital deduction, the property must be includible in the trustor's gross estate for federal estate tax purpose.

A Hawaii Inter Vivos TIP Trust with Principal to Donor's Children on Spouse's Death is a type of trust created during the lifetime of the donor (also known as a settler or granter) in the state of Hawaii. This trust is specifically structured to provide specific benefits and protections for both the surviving spouse and the donor's children. The key feature of this type of trust is that it allows the donor to transfer assets and property into the trust, while ensuring that the surviving spouse is taken care of during their lifetime. Upon the death of the surviving spouse, the remaining principal of the trust is then distributed to the donor's children as designated in the trust documents. By creating an Inter Vivos TIP Trust, the donor can ensure that their assets are properly managed and distributed according to their wishes, while also providing for the financial wellbeing and security of their surviving spouse. This type of trust can be particularly useful in situations where there may be blended families or concerns about remarriage or potential disputes over inheritance. Different variations of Hawaii Inter Vivos TIP Trust with Principal to Donor's Children on Spouse's Death may include: 1. Marital TIP Trust: This type of trust allows the surviving spouse to receive income generated by the trust assets during their lifetime, while also preserving the principal for the donor's children. Upon the death of the surviving spouse, the principal is distributed to the children. 2. Discretionary TIP Trust: In this type of trust, the trustee has discretion over how much income or principal is distributed to the surviving spouse. This provides flexibility in managing the trust assets and allows the trustee to consider the financial needs and circumstances of the surviving spouse. 3. Testamentary TIP Trust: This trust is created through a provision in the donor's will and goes into effect upon their death. It allows the surviving spouse to receive income from the trust during their lifetime, with the principal going to the donor's children upon the spouse's death. Overall, a Hawaii Inter Vivos TIP Trust with Principal to Donor's Children on Spouse's Death provides a comprehensive estate planning solution for individuals wishing to ensure the financial well-being of their surviving spouse while also protecting their children's inheritance. Consulting with an attorney experienced in estate planning and trust administration is essential to properly establish these trusts and ensure compliance with Hawaii state laws and regulations.

A Hawaii Inter Vivos TIP Trust with Principal to Donor's Children on Spouse's Death is a type of trust created during the lifetime of the donor (also known as a settler or granter) in the state of Hawaii. This trust is specifically structured to provide specific benefits and protections for both the surviving spouse and the donor's children. The key feature of this type of trust is that it allows the donor to transfer assets and property into the trust, while ensuring that the surviving spouse is taken care of during their lifetime. Upon the death of the surviving spouse, the remaining principal of the trust is then distributed to the donor's children as designated in the trust documents. By creating an Inter Vivos TIP Trust, the donor can ensure that their assets are properly managed and distributed according to their wishes, while also providing for the financial wellbeing and security of their surviving spouse. This type of trust can be particularly useful in situations where there may be blended families or concerns about remarriage or potential disputes over inheritance. Different variations of Hawaii Inter Vivos TIP Trust with Principal to Donor's Children on Spouse's Death may include: 1. Marital TIP Trust: This type of trust allows the surviving spouse to receive income generated by the trust assets during their lifetime, while also preserving the principal for the donor's children. Upon the death of the surviving spouse, the principal is distributed to the children. 2. Discretionary TIP Trust: In this type of trust, the trustee has discretion over how much income or principal is distributed to the surviving spouse. This provides flexibility in managing the trust assets and allows the trustee to consider the financial needs and circumstances of the surviving spouse. 3. Testamentary TIP Trust: This trust is created through a provision in the donor's will and goes into effect upon their death. It allows the surviving spouse to receive income from the trust during their lifetime, with the principal going to the donor's children upon the spouse's death. Overall, a Hawaii Inter Vivos TIP Trust with Principal to Donor's Children on Spouse's Death provides a comprehensive estate planning solution for individuals wishing to ensure the financial well-being of their surviving spouse while also protecting their children's inheritance. Consulting with an attorney experienced in estate planning and trust administration is essential to properly establish these trusts and ensure compliance with Hawaii state laws and regulations.